The demand for loans is influenced by a variety of factors, including interest rates, economic conditions, consumer confidence, and government policies. When interest rates are high, borrowing becomes more expensive, leading to a decrease in loan demand as individuals and businesses opt to borrow less. This relationship between interest rates and loan demand is inverse, with higher interest rates deterring borrowers and lower interest rates encouraging them. Additionally, economic factors such as expectations of an economic slowdown can make consumers more inclined to save and borrow less, impacting the demand for loans. Government policies that affect disposable income, such as changes in marginal tax rates, can also influence borrowing behaviour and loan demand. Understanding these factors is crucial for financial institutions, investors, and policymakers to make informed decisions and predict shifts in the market for loanable funds.

| Characteristics | Values |

|---|---|

| Relationship between money supply and demand for loans | Inverse relationship |

| Impact of money supply on interest rates | More money = lower interest rates; Less money = higher interest rates |

| Impact of interest rates on borrowing | Higher interest rates = more expensive to borrow; Lower interest rates = cheaper to borrow |

| Factors influencing interest rates | Overall strength of the economy, inflation, unemployment, supply and demand, risk premium |

| Impact of borrowing cost on demand for loans | Higher borrowing cost = lower demand for loans; Lower borrowing cost = higher demand for loans |

| Role of financial institutions | Financial institutions adjust interest rates to balance supply and demand |

What You'll Learn

![]()

The inverse relationship between money supply and interest rates

The Inverse Relationship

The money supply and interest rates are inversely related. When there is a larger money supply in a country's economy, market interest rates tend to be lower, making it cheaper for consumers to borrow. Conversely, a smaller money supply leads to higher interest rates, making loans more expensive for consumers. This relationship is not isolated but influences and is influenced by various economic factors.

Impact on Borrowing and Spending

The Role of Central Banks

Central banks, such as the Federal Reserve in the United States, play a crucial role in managing the money supply and influencing interest rates. They employ various tools of monetary policy, including open-market operations, the discount rate, and reserve requirements, to control the money supply and, by extension, interest rates. This management is essential for guiding the economy through different stages of the business cycle. For example, during the expansionary stage, a contractionary monetary policy may be implemented to decrease the money supply, leading to higher interest rates and discouraging borrowing to prevent the economy from "overheating."

Interest Rates and Risk

While the money supply significantly influences interest rates, it is important to note that interest rates also reflect the level of risk that investors and lenders are willing to accept. This is known as the risk premium. Investors consider the likelihood of repayment when deciding between investment options with different interest rates. The perceived risk associated with a particular investment will influence the interest rate demanded by the investor.

Bellco's RV Loan Options: What You Need to Know

You may want to see also

![]()

How interest rates reflect the cost of borrowing

Interest rates are influenced by the demand for, and supply of, credit in an economy. An increase in demand for credit will lead to a rise in interest rates, or the price of borrowing. On the other hand, a rise in the supply of credit leads to a decline in interest rates. The supply of credit increases when the total amount of money that is borrowed goes up. For example, when money is deposited in banks, they can lend more money, increasing the credit available and thus increasing borrowing. When this occurs, the cost of borrowing decreases.

The money supply in a country is influenced by the actions of its central bank, such as the Federal Reserve in the United States, and commercial banks. A larger money supply lowers market interest rates, making it less expensive for consumers to borrow. Smaller money supplies tend to raise market interest rates, making it pricier for consumers to take out a loan. The central bank must consider the overall strength of the economy, including inflation, unemployment, and supply and demand, to set interest rates.

Interest rates can also be influenced by the level of risk that investors and lenders are willing to accept. This is referred to as the risk premium. For example, an investor with excess money to lend may have two possible investments: one offering a 5% interest rate and the other offering a 6% interest rate. The investor must consider the likelihood of being repaid and may choose the lower rate or ask the 6% buyer to raise the rate to a premium in proportion to the assumed risk.

Interest rates can be fixed, where the rate remains constant throughout the term of the loan, or floating, where the rate is variable and can fluctuate based on a reference rate. The interest expense, or cost of borrowing money, is calculated on the original or principal amount of the loan. The interest rate is usually expressed as a percentage of the principal per period of time, typically a year. This measure includes interest and may include other costs such as fees and charges. The longer the borrower has to repay the loan, the more interest the lender should receive as long-term loans have a greater chance of not being repaid.

Best Egg Refinance Loans: What You Need to Know

You may want to see also

![]()

How the demand for loans is measured

The demand for loans is measured by the willingness of firms to borrow to engage in large-scale construction projects. This could include the construction of a new manufacturing facility, research into a new product line, or upgrading existing capital. The supply of loanable funds is determined by the willingness of households to save, in addition to the savings or dis-savings of the government. When households save more today, they are also reducing their current levels of consumption. Essentially, they are deferring present consumption to the future.

Financial markets are made up of markets for different types of securities: equities, bonds, credit cards, etc. In the market for each asset, supply and demand interact to determine the price and rate of return. Since each financial market is both a source of borrowed funds and a destination for saving, each financial asset is a substitute for every other financial asset, and thus, all financial markets are linked, directly or indirectly. For example, if the interest rate on US Treasury Bills goes up, you should expect the interest rates on US Treasury notes and bonds to go up to a certain extent as well.

The interest rate measures the price in the financial market. If the interest rate is above the equilibrium level, an excess supply or surplus of financial capital will arise in this market. For instance, at an interest rate of 21%, the quantity of funds supplied increases to $750 billion, while the quantity demanded decreases to $480 billion. At this above-equilibrium interest rate, firms are keen to supply loans to credit card borrowers, but relatively few people or businesses wish to borrow. As a result, some credit card firms will lower the interest rates or other fees they charge to attract more business. This strategy will push the interest rate down toward the equilibrium level.

If the interest rate is below the equilibrium, then excess demand or a shortage of funds occurs in this market. At an interest rate of 13%, the quantity of funds credit card borrowers demand increases to $700 billion, but the quantity the credit card firms are willing to supply is only $510 billion.

Does Lending Money Make You a Business?

You may want to see also

![]()

The impact of government borrowing on private investment

During periods of high unemployment, government borrowing can help absorb idle funds, ensuring that private investment is not affected. In this scenario, the government's ability to borrow without impacting private investment is enhanced by the availability of excess savings. On the other hand, during periods of full employment, government borrowing can restrict private spending. This is because, with banks already loaned up to their limit and investments absorbing all available savings, additional government borrowing will compete with private investment, making it more costly.

The concept of the "crowding-out effect" in economic theory suggests that increased government spending, achieved through higher taxes or borrowing, ultimately decreases private sector spending. This occurs because higher taxes can reduce income and spending by individuals and businesses, while increased borrowing by the government can lead to higher interest rates and borrowing costs, reducing borrowing demand from the private sector. As a result, businesses may become discouraged from making capital investments due to the increased cost of borrowing.

The relationship between government debt and corporate policies is significant. Government debt issuance can influence investors' portfolio allocations and the relative pricing of different assets. It has been observed that government debt is negatively correlated with corporate debt and investment but positively correlated with corporate liquidity. This implies that when government debt increases, corporate debt and investment decrease, while corporate liquidity improves. This relationship is more evident in larger, less risky firms whose debt is a closer substitute for government securities.

The money supply also plays a crucial role in the impact of government borrowing on private investment. A larger money supply generally leads to lower interest rates, making borrowing less expensive for consumers. Conversely, a smaller money supply tends to raise interest rates, making borrowing more costly. The central bank must consider the overall strength of the economy, including factors such as inflation, unemployment, and supply and demand, when determining interest rates.

Best Buy Loaner Phones: What's the Deal?

You may want to see also

![]()

The role of the Federal Reserve in setting interest rates

The Federal Reserve (Fed) is the central bank of the United States and is perhaps the most influential financial institution in the world. The Fed's management of monetary policy can have a significant impact on the shape of the nation's economy.

The Federal Open Market Committee (FOMC) sets a target interest rate policy for the federal funds rate. This is the rate at which commercial banks borrow and lend excess reserves to other banks on an overnight basis. The federal funds rate is a cornerstone of US monetary policy and a key driver of economic activity. The FOMC's decisions about the federal funds rate have far-reaching economic consequences and are widely followed by the non-financial press. The FOMC sets the target federal funds rate eight times a year, based on prevailing economic conditions.

The Federal Reserve uses its monetary policy tools to implement, or carry out, the new stance of policy. The key tools of monetary policy are "administered rates" that the Federal Reserve sets: Interest on reserve balances; the Overnight Reverse Repurchase Agreement Facility; and the discount rate. The Fed adjusts two administered rates, interest on reserve balances and ON RRP, to keep the federal funds rate within the target range determined by the FOMC. The Fed adjusts the discount rate to serve as a ceiling. The Fed usually adjusts the three administered rates by the same amount and at the same time so they move up and down together.

The Federal Reserve also influences interest rates through its balance sheet of financial assets. During challenging economic periods, the Fed has tried to boost economic activity by purchasing fixed-income assets, such as US government bonds and mortgage-backed securities. The Fed's market participation helps moderate interest rates.

Beto's College Loans: What Does He Owe?

You may want to see also

Frequently asked questions

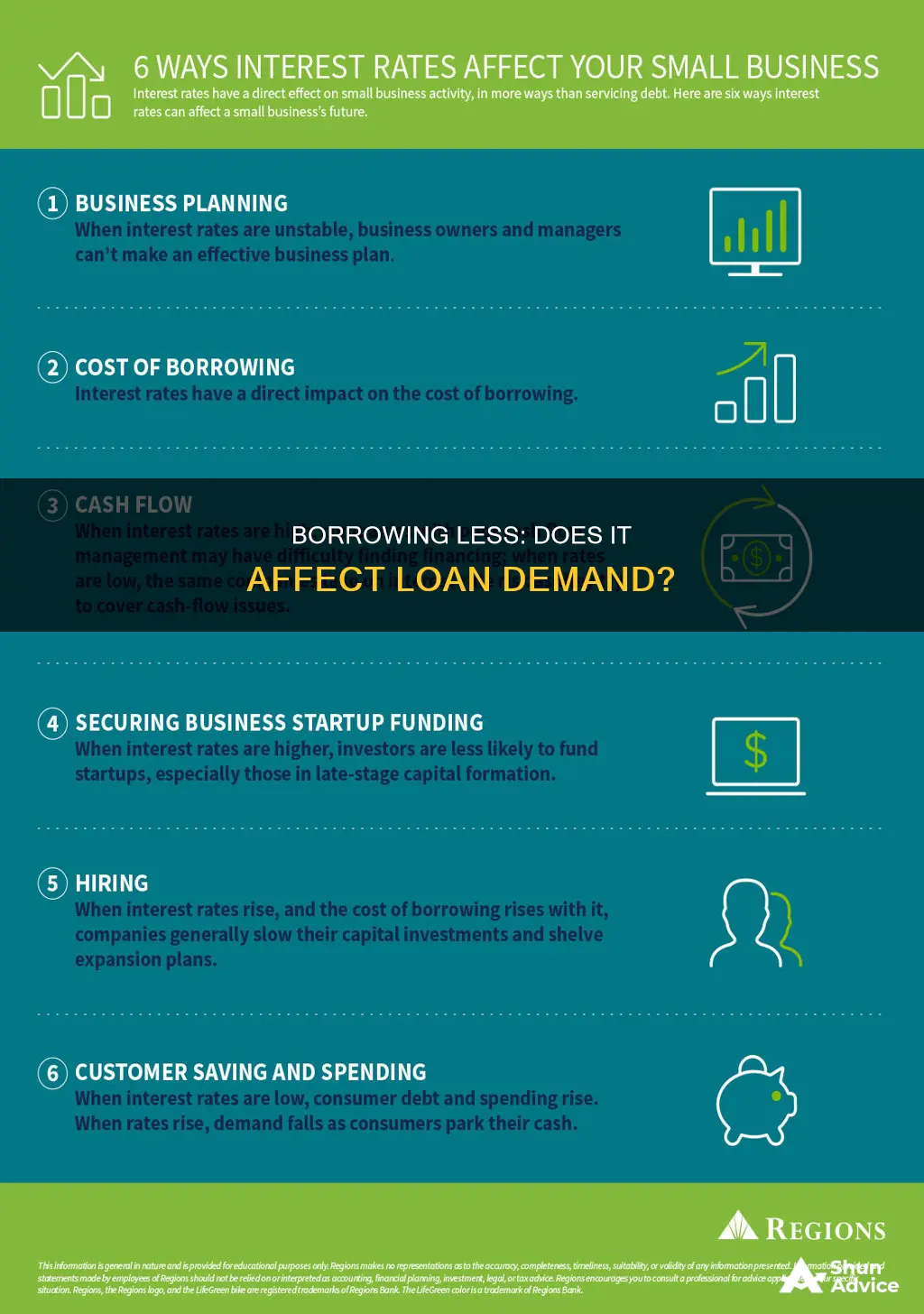

Yes, borrowing less does decrease the demand for loans. This is because, as the interest rate increases, the cost of borrowing also increases, which slows down the number of new loans being issued.

Interest rates and the demand for loans are inversely proportional. As interest rates increase, the demand for loans decreases, and vice versa.

Higher interest rates make it more expensive for households and firms to borrow money for purchasing housing and durable goods or investing in projects. As a result, they will borrow less, leading to a decrease in the demand for loans.

Interest rates are influenced by the supply and demand for money, the level of risk that investors and lenders are willing to accept, and the overall strength of the economy, including factors like inflation, unemployment, and government policies.

Financial institutions monitor the market equilibrium between the supply and demand for loanable funds. If there is an excess demand for loans, they may lower interest rates to attract more borrowers and increase the supply of loanable funds. Conversely, if there is an excess supply, they may raise interest rates to make borrowing more attractive, stimulating demand for loans.