Many investors are curious about the strategy of buying term insurance and investing the difference, but it's important to understand the pros and cons before making a decision. This approach involves using the savings from term insurance premiums to invest in assets, potentially growing the money over time. While it can provide financial security and potential returns, it also comes with risks and considerations. This paragraph will explore the concept in detail, examining the benefits of combining insurance and investment, as well as the potential drawbacks and factors to consider before implementing this strategy.

What You'll Learn

- Risk and Reward: Understanding the trade-off between risk and potential returns when investing

- Term Length: Exploring the impact of different term lengths on investment strategies

- Market Conditions: Analyzing how market trends affect the effectiveness of this strategy

- Tax Implications: Examining the tax benefits and drawbacks of buying term and investing

- Diversification: Discussing how this approach can contribute to a diversified investment portfolio

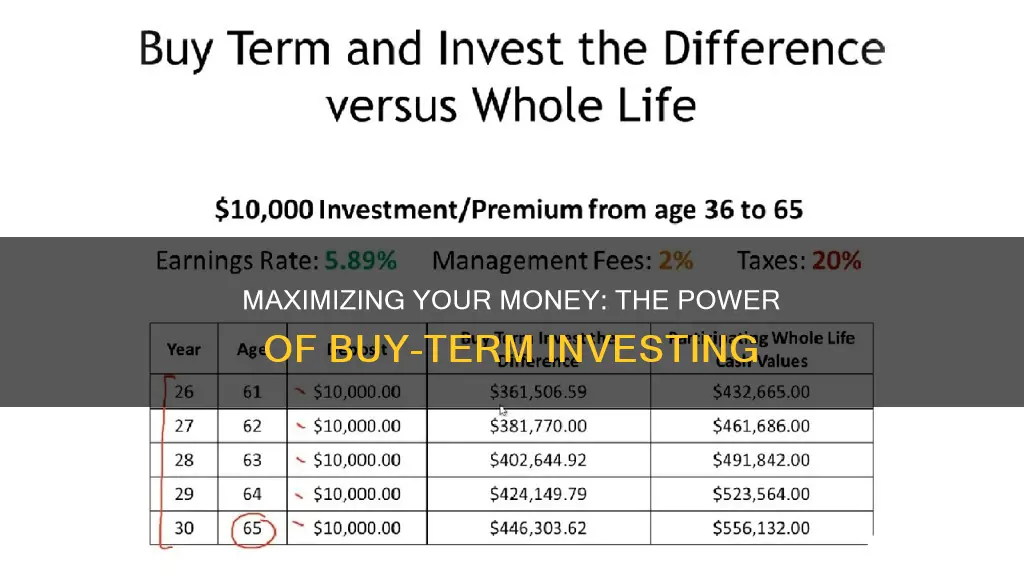

![]()

Risk and Reward: Understanding the trade-off between risk and potential returns when investing

When it comes to investing, understanding the relationship between risk and reward is crucial. This concept is often referred to as the risk-reward trade-off, and it's a fundamental principle that investors should grasp to make informed decisions. The idea is simple: the higher the potential return, the greater the risk involved. This trade-off is a key consideration for investors, especially those who are just starting their investment journey.

In the context of your question, "Does buying term and investing the difference work?" this concept becomes even more relevant. Buying term insurance, such as life insurance, provides a guaranteed return in the form of a death benefit. However, the trade-off is that you are taking on a certain level of risk. The risk here is the potential for a decrease in the value of your investment if the market performs poorly or if you need to access the funds before the term ends. By investing the difference, you are essentially seeking higher returns, which come with their own set of risks.

The key to success in this strategy is to carefully assess your risk tolerance and investment goals. Here are some points to consider:

- Risk Assessment: Evaluate your financial situation and determine how much risk you are willing to take. This involves understanding your investment horizon, the potential impact of market volatility, and your ability to withstand short-term fluctuations. For example, if you have a long-term investment goal, you might be more comfortable with higher-risk investments.

- Diversification: Diversifying your portfolio is a powerful way to manage risk. By spreading your investments across different asset classes, sectors, and regions, you reduce the impact of any single investment's performance on your overall portfolio. This strategy ensures that even if one investment underperforms, others may compensate for it.

- Long-Term Perspective: Investing often requires a long-term commitment. Short-term market fluctuations should not deter you from your investment strategy. By maintaining a long-term perspective, you can weather short-term market volatility and benefit from the power of compounding returns.

- Regular Review: Regularly reviewing your investment portfolio is essential. Market conditions and your personal circumstances may change over time, and adjustments may be necessary. Reviewing your investments periodically allows you to rebalance your portfolio, ensuring it aligns with your risk tolerance and goals.

In summary, buying term insurance and investing the difference can be a viable strategy, but it requires a thoughtful approach. By understanding the risk-reward trade-off, assessing your risk tolerance, and adopting a long-term investment mindset, you can make informed decisions that align with your financial objectives. Remember, investing is a journey, and managing risk is an ongoing process that requires careful consideration and adaptation to changing market conditions.

Wall Street's Annual Investors

You may want to see also

![]()

Term Length: Exploring the impact of different term lengths on investment strategies

The concept of "buy term and invest the difference" is an investment strategy that involves purchasing an annuity or a term insurance policy and then investing the difference between the policy's value and the premium paid. This approach is particularly appealing to those seeking to optimize their investment returns while also having a guaranteed income stream. The term length of the policy plays a crucial role in this strategy, as it directly impacts the investment period and the potential returns.

When considering different term lengths, investors should evaluate the trade-off between immediate income and long-term growth. Longer term policies offer the advantage of a more extended investment horizon, allowing for potential compound growth. For example, a 30-year term policy provides a more extended period for the investment to mature, potentially resulting in higher returns. However, this comes with the risk that the investor may outlive the policy, and the guaranteed income stream may not be needed for an extended period.

Shorter term lengths, such as 10 or 20 years, provide a more immediate income stream, which can be beneficial for those seeking regular cash flow. These policies offer a more conservative approach, ensuring a steady income for a defined period. While the investment growth may be more limited, the guaranteed payments provide a sense of security, especially for retirees or those approaching retirement age.

The impact of term length on investment strategies is significant. Longer terms may attract investors seeking substantial growth, while shorter terms cater to those prioritizing a consistent income. A comprehensive analysis of an individual's financial goals, risk tolerance, and life expectancy is essential to determine the most suitable term length. For instance, a young investor with a long-term financial plan might opt for a longer term policy, while an older individual may prefer a shorter term to secure immediate income.

In summary, the "buy term and invest the difference" strategy offers a flexible approach to investing, allowing individuals to tailor their financial plans according to their needs. By understanding the implications of different term lengths, investors can make informed decisions, balancing the desire for growth with the need for a reliable income stream. This strategy provides a unique opportunity to optimize investments while also considering the individual's unique circumstances and goals.

The Secret to Unlocking Investment: The Top500 Strategy

You may want to see also

![]()

Market Conditions: Analyzing how market trends affect the effectiveness of this strategy

When considering the strategy of buying term insurance and investing the difference, it's crucial to understand the market conditions that can significantly impact its effectiveness. This approach involves purchasing a term life insurance policy, which provides coverage for a specific period, and then investing the savings from the premiums in various financial instruments. The success of this strategy relies heavily on the prevailing market trends and economic conditions.

One critical factor is the interest rates set by central banks. Lower interest rates often make borrowing cheaper, which can encourage people to take out loans or mortgages. This environment might not be ideal for the buy-term strategy, as it may lead to reduced savings or investment opportunities. Conversely, in a high-interest-rate environment, borrowing becomes more expensive, potentially limiting the appeal of taking out loans for this strategy.

Market volatility is another essential consideration. If the financial markets experience significant fluctuations, the value of investments can vary dramatically. During periods of high volatility, the strategy's effectiveness may be diminished as the investment returns could be less predictable. For instance, if the stock market takes a downturn, the value of the invested funds might decrease, impacting the overall success of the strategy.

Additionally, market trends in the insurance industry play a vital role. The availability and cost of term life insurance policies can vary based on market conditions. In a competitive market, insurance providers might offer more attractive rates or additional benefits, making the buy-term strategy more appealing. However, during periods of economic uncertainty, insurance companies may adjust their pricing or terms, potentially affecting the strategy's long-term viability.

Lastly, economic growth and inflation rates are essential indicators. A robust economy with low inflation can provide a favorable environment for investment growth. In such conditions, the strategy's focus on investing the difference can potentially yield positive returns. Conversely, high inflation may erode the purchasing power of the invested funds, making it less effective over time. Understanding these market conditions is key to making informed decisions and optimizing the buy-term investment strategy.

Buy-to-Let UK: Where to Invest for Long-Term Returns

You may want to see also

![]()

Tax Implications: Examining the tax benefits and drawbacks of buying term and investing

The strategy of buying term insurance and investing the difference can be a powerful financial tool, but it's important to understand the tax implications that come with it. This approach involves purchasing a term life insurance policy, which provides coverage for a specific period, and then investing the surplus funds in various financial instruments. While this strategy can offer significant benefits, it's crucial to consider the tax consequences to ensure you're making an informed decision.

One of the primary tax advantages of this approach is the potential for tax-deferred growth. When you invest the difference between the cost of the term insurance and your actual investment, you can benefit from tax-free growth. This is particularly beneficial for long-term investments, as the compound interest can accumulate over time without being taxed annually. For example, if you invest $10,000 annually in a tax-advantaged account, and the investment grows at a rate of 7% annually, you could accumulate a substantial amount over 20 years, all while avoiding capital gains taxes.

However, there are also potential drawbacks and tax considerations. Firstly, the initial investment in term insurance may be a significant expense, and the premiums can be substantial, especially for higher coverage amounts. These premiums are typically tax-deductible, but the timing and method of deduction can vary. In some cases, you may be able to deduct the premiums in the year they are paid, providing an immediate tax benefit. Alternatively, if you choose to itemize deductions, you can claim the premiums as a medical expense deduction, which may offer more flexibility in certain tax years.

Additionally, when investing the difference, you should be mindful of the tax treatment of your investments. If you invest in tax-efficient vehicles like a 401(k) or an individual retirement account (IRA), the growth and earnings within these accounts are often tax-deferred or tax-free until withdrawal. This allows your investments to grow exponentially over time. However, if you invest in other vehicles, such as a taxable brokerage account, you may be subject to capital gains taxes when you sell the investments, depending on the holding period and your tax bracket.

In summary, buying term insurance and investing the difference can be a strategic financial move, but it requires careful consideration of tax implications. Understanding the tax benefits, such as tax-deferred growth and potential deductions, is essential. At the same time, being aware of the potential drawbacks, including the tax treatment of your investments and the initial insurance premiums, will help you make an informed decision. Consulting with a financial advisor or tax professional can provide personalized guidance, ensuring that your strategy aligns with your financial goals and tax situation.

Investing in People: Definition and Impact

You may want to see also

![]()

Diversification: Discussing how this approach can contribute to a diversified investment portfolio

Diversification is a fundamental strategy in investing, and it involves spreading your investments across various assets, sectors, and geographic regions to reduce risk and maximize returns. This approach is particularly relevant when considering the concept of "buy term and invest the difference," which is a strategy where you purchase a term policy, invest the difference between the premium and the policy's value, and potentially benefit from the investment's growth over time. Here's how diversification can contribute to a well-rounded investment portfolio:

Asset Allocation: Diversification allows investors to allocate their capital across different asset classes such as stocks, bonds, real estate, commodities, and cash equivalents. By buying term insurance and investing the difference, you can direct the funds towards various investment vehicles. For instance, you might invest in a mix of stocks from different industries, government bonds, and alternative investments like real estate investment trusts (REITs) or mutual funds. This allocation ensures that your portfolio is not overly exposed to any single asset class, reducing the impact of market volatility.

Risk Management: One of the primary benefits of diversification is risk reduction. By investing in a variety of assets, you can mitigate the risks associated with individual investments. If one investment underperforms, the gains from other diversified holdings can offset potential losses. For example, if the stock market experiences a downturn, but your bond investments and real estate holdings perform well, your overall portfolio value may remain stable or even increase. This strategy is especially crucial when using the "buy term and invest the difference" method, as it provides a safety net through insurance while allowing for strategic investments.

Long-Term Growth Potential: Diversification aims to capture the long-term growth potential of various markets and sectors. By investing in a range of assets, you increase the chances of benefiting from different economic cycles and market trends. For instance, investing in a mix of large-cap and small-cap stocks can provide exposure to both established and emerging companies, potentially offering higher returns over time. Similarly, investing in international markets through diversified funds can provide access to global growth opportunities. This approach ensures that your portfolio is not limited by the performance of a single market or industry.

Flexibility and Adaptability: A diversified portfolio offers flexibility, allowing investors to adapt to changing market conditions. If certain sectors or asset classes outperform, the investor can rebalance the portfolio to maintain the desired asset allocation. This rebalancing process ensures that the portfolio remains aligned with the investor's risk tolerance and financial goals. Additionally, diversification enables investors to take advantage of new investment opportunities as they arise, providing a dynamic and responsive investment strategy.

In summary, diversification is a powerful tool for investors, especially when combined with the "buy term and invest the difference" strategy. It enables investors to manage risk, capture growth potential, and maintain a balanced portfolio. By allocating investments across various asset classes and sectors, investors can navigate market fluctuations and potentially achieve their long-term financial objectives. This approach encourages a thoughtful and strategic investment mindset, ensuring that the portfolio is well-prepared for various economic scenarios.

College Savings: Invest Wisely for Your Child's Future

You may want to see also

Frequently asked questions

This strategy involves purchasing term life insurance, which provides coverage for a specific period, and then investing the difference between the insurance premium and the death benefit in a separate investment vehicle.

By buying term life insurance, you secure financial protection for your loved ones during the specified term. Simultaneously, investing the difference can potentially grow your money over time, providing a financial cushion or additional savings.

This method combines insurance and investment, offering both immediate financial security and long-term growth potential. It allows you to protect your loved ones while also building wealth, providing a comprehensive financial plan.

While this strategy can be beneficial, it's important to note that term life insurance may not be the most cost-effective long-term investment. Additionally, the investment portion carries market risks, and the performance of the investment vehicle can vary.

Absolutely! You can adjust the term length of the insurance policy to align with your specific needs and the duration of your financial goals. The investment portion can also be tailored to your risk tolerance and investment preferences, allowing for a personalized approach to financial planning.