The COVID-19 pandemic saw the introduction of the Economic Injury Disaster Loan (EIDL) program, which provided financial support to businesses. While the EIDL program is no longer accepting new applications, it is important to understand its implications, such as whether EIDL loans increase shareholder basis. Shareholder basis in an S corporation is influenced by factors like corporate taxable income, capital contributions, corporate losses, and distributions. In the context of EIDL loans, it is stated that they are treated like any other loan, and therefore, they do not increase the shareholder's basis in an S corporation. However, loan forgiveness under the Consolidated Appropriations Act, 2021, can lead to an increase in basis for a shareholder in an S corporation.

What You'll Learn

![]()

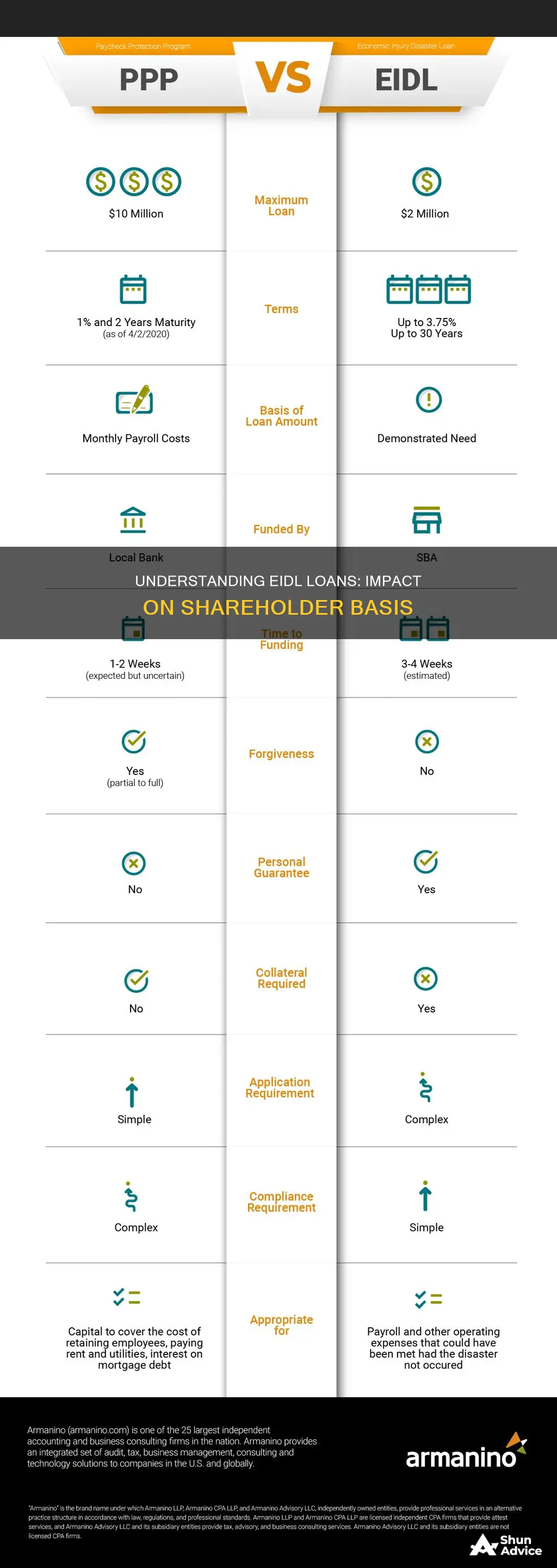

EIDL loans are treated the same as other loans

EIDL loans, or Economic Injury Disaster Loans, are a standard tool used by the Small Business Administration (SBA) to help businesses recover from disasters. They are treated the same as any other loan and do not increase an S corporation shareholder's basis.

EIDL loans are generally secured by a lien on all business assets of the borrower. This means that if a borrower defaults on their EIDL loan, the case will be referred to the Treasury Department, which can garnish income, file liens against the business, and sue to collect any personal guarantees or other promised collateral. As such, it is important to continue making loan payments to the SBA. However, if a borrower is unable to make payments, they can work with a law group to provide an offer in compromise to the federal government to reduce their burden.

In the case of a business closure or liquidation, the borrower must send a message through the MySBA Loan Portal or contact COVID-19 EIDL customer service. If a borrower purchases a portion of a seller's assets or specific equipment that is subject to an EIDL lien, a complete payoff of the EIDL loan may not be necessary. The EIDL Customer Service center can facilitate a seller's request for the SBA's release of the specific collateral via the "Application for Release of Collateral". After receiving the application, the SBA may require the seller to pay down a portion of the EIDL loan as consideration for releasing its lien on the specific assets.

When a lender is financing a borrower's purchase of a seller's business assets, the lender should address any liens on the assets to be acquired in the sale that are subject to a UCC-1 in favor of the SBA which secure an EIDL loan. In a complete asset sale, lenders typically require that the EIDL loan is paid off in full from the seller's sale proceeds. This ensures that the seller can terminate the SBA's UCC lien on their assets after the EIDL loan is fully paid, leaving the lender in first lien position following the closing.

Dire Consolidation Loans: Two-Part Payment Plans?

You may want to see also

![]()

EIDL loans are not eligible for forgiveness

The COVID-19 Economic Injury Disaster Loan (EIDL) program is no longer accepting new applications, increase requests, or reconsiderations. EIDL loans are not eligible for forgiveness and require full repayment, except for the EIDL advance grants. The EIDL loans are structured as traditional loans, and recipients are expected to repay the full loan amount with interest, regardless of how the funds were utilized.

The Small Business Administration (SBA) had provided up to 30 months of deferment, but as of now, most loans have entered the repayment phase, and borrowers are expected to make regular payments. The standard loan terms for EIDL loans are 30-year repayment terms with low interest rates of 3.75% for businesses and 2.75% for non-profits.

If a business is struggling to repay an EIDL loan, it is important to understand the available options. Ignoring repayment obligations can lead to serious consequences, including default, damage to credit, and legal action. There are a few options to consider:

- Dissolving the business: If the original loan amount is under $200,000, it is not tied to any personal guarantees, so owners can dissolve the business without any harm to personal assets.

- Defaulting on the loan: If the loan debt is over $200,000, this decision can be challenging due to the potential for personal guarantees. Defaulting on the loan can result in significant financial repercussions, such as collections and wage garnishment, as well as asset liens.

- Filing for business bankruptcy: In some instances, personal bankruptcy can reduce or eliminate the debt obligations tied to a business's EIDL loan. Chapter 7 bankruptcy can remove personal guarantees, while Chapters 11 and 13 can reduce the debt a business owner is responsible for.

It is important to note that the SBA has introduced flexible hardship accommodations for borrowers facing financial difficulties. The Hardship Accommodation Plan (HAP) offered temporary relief by reducing payments to as low as $25 per month for six months. However, as of March 19, 2025, the HAP for COVID-19 EIDL is no longer open.

Discover Loan: Co-signers Allowed?

You may want to see also

![]()

EIDL loans are secured by a lien on business assets

EIDL loans are generally secured by a lien on all business assets of the borrower. This means that if a borrower defaults on their loan, the Small Business Administration (SBA) may seize their business assets to collect the debt.

In the case of a complete asset sale, lenders typically require that the EIDL loan is paid off in full from the seller's proceeds. This allows the seller to terminate the SBA's lien on their assets after the loan is fully paid. The lender should require the seller to obtain the SBA's payoff letter with wire instructions before proceeding to the closing of the sale.

If a borrower is purchasing a portion of a seller's assets or specific equipment that is subject to an EIDL lien, a complete payoff of the EIDL loan may not be necessary. In this case, the seller can request the SBA's release of the specific collateral through the "Application for Release of Collateral". Upon receiving this application, the SBA may require the seller to pay down a portion of the EIDL loan as consideration for releasing its lien on the specific assets. This collateral release ensures that the borrower receives the purchased assets free of any EIDL lien and allows the lender to obtain its proper lien position.

It is important to note that EIDL loans do not increase an S corporation shareholder's basis. However, EIDL loans are treated the same as any other loan, and there are options for borrowers facing financial distress, such as seeking a subordination agreement or consulting with attorneys experienced in business lending and SBA loan matters.

Earnest Refinance: A Better Option than Sallie Mae Loans?

You may want to see also

![]()

EIDL loans are tax-free

The COVID-19 pandemic has had a devastating impact on businesses, and many have had to seek financial support to stay afloat. The Economic Injury Disaster Loan (EIDL) program, offered by the Small Business Administration (SBA), has been a vital source of funding for small businesses. While these loans have helped businesses stay operational, they have also raised questions about their tax implications.

EIDL loans are generally secured by a lien on all business assets of the borrower. This means that if a borrower defaults on the loan, the SBA has the right to take possession of and sell the business's assets to recoup the loan amount. This can have significant consequences for the borrower, as they may lose their business and face financial ruin. Thus, it is essential for borrowers to understand the terms of the loan, including the potential tax consequences.

The good news is that EIDL loans are indeed tax-free. The Consolidated Appropriations Act of 2021 (CAA, 2021) clarified that gross income does not include forgiveness of EIDL loans, emergency EIDL grants, and certain loan repayment assistance. This means that any amounts received as EIDL advances or restaurant revitalization grants are excluded from the gross income of the recipient. This exclusion applies to both individual business owners and partnerships or S corporations.

In the case of partnerships or S corporations, any amount of EIDL advance or grant excluded from income under the CAA, 2021 or the ARPA (as per the relevant date of enactment) will be treated as tax-exempt income. This tax-exempt income will then be allocated to the partners or shareholders in proportion to their ownership interests in the company. This allocation will increase the partners' or shareholders' bases in their partnership interests.

While EIDL loans are tax-free, it is important to note that there are still financial obligations associated with them. Borrowers are responsible for making regular monthly payments, and interest continues to accrue on the loan balance during any deferment period. Additionally, EIDL loans are subject to repayment and have a 30-year repayment term with low-interest rates (3.75% for businesses and 2.75% for nonprofits).

Understanding Loan and Deed Name Requirements: Do They Match?

You may want to see also

![]()

EIDL loans are low-interest

The low-interest nature of EIDL loans is advantageous for borrowers, particularly when compared to other types of loans or financing solutions. The low interest can result in lower monthly payments, making the loan more affordable for businesses facing economic hardship. This feature of EIDL loans is especially beneficial when a borrower is considering their various loan options and weighing the associated costs.

In addition to the low-interest rates, EIDL loans also offer other benefits. For instance, borrowers can make voluntary payments during the deferment period without incurring prepayment penalties. This flexibility allows businesses to manage their cash flow and make payments when they are able to. Additionally, the SBA provides a Hardship Accommodation Plan (HAP) to offer temporary relief to borrowers facing financial difficulties. Under this plan, payments can be reduced to as low as $25 per month for a period of six months.

However, it is important to note that EIDL loans are not eligible for forgiveness, except for advance grants. Borrowers are responsible for their monthly payment obligations, and interest continues to accrue during the deferment period. If voluntary payments are not made during the deferment, a final balloon payment will be due on the loan at maturity. Therefore, while EIDL loans offer low-interest rates, borrowers should be mindful of their repayment obligations and the potential consequences of non-payment.

Cosigning Loans: Citizen Requirements and Financial Implications

You may want to see also

Frequently asked questions

EIDL stands for Economic Injury Disaster Loan. The Small Business Administration (SBA) provided these loans to small businesses during the COVID-19 pandemic.

No, EIDL loans do not increase an S corporation shareholder's basis. They are treated the same as any other loan.

You can manage your EIDL loan through the MySBA Loan Portal. Here, you can monitor your loan status and make payments. You can also contact COVID-19 EIDL Customer Service by calling 833-853-5638 or emailing [email protected].