The Federal National Mortgage Association, commonly known as Fannie Mae, is a government-sponsored enterprise that provides liquidity, stability, and affordability to the mortgage market. It does not directly offer loans to homeowners but instead buys and guarantees mortgages through the secondary mortgage market. In doing so, it creates liquidity for lenders, allowing them to underwrite or fund additional mortgages. While Fannie Mae has helped expand homeownership, particularly for low- to moderate-income borrowers, it has also been criticized for its involvement in the subprime mortgage crisis of 2008. This crisis was fueled by relaxed underwriting standards, contributing to an explosion of subprime lending and the spread of toxic mortgages throughout the financial system. As a result, Fannie Mae and its counterpart Freddie Mac faced significant challenges and required a government bailout.

| Characteristics | Values |

|---|---|

| Nature of the Enterprise | Government-sponsored |

| Role | Provides liquidity, stability, and affordability to the mortgage market |

| Target Group | Low- to moderate-income borrowers |

| Type of Loans | Does not originate loans but buys and guarantees mortgages through the secondary mortgage market |

| Tax Exemptions | Exempt from state and local taxes |

| Regulating Bodies | Department of Housing and Urban Development (HUD) and the Federal Housing Finance Agency (FHFA) |

| Role in the 2008 Financial Crisis | Started investing in riskier loans, contributing to a housing bubble |

| Impact of the 2008 Financial Crisis | Nearly collapsed and were bailed out and placed into government conservatorship |

What You'll Learn

![]()

Fannie Mae's role in the 2008 financial crisis

Fannie Mae, along with Freddie Mac, played a significant role in the 2008 financial crisis. Both are government-sponsored enterprises (GSEs) that buy residential mortgages on the secondary market to hold or bundle and sell as mortgage-backed securities (MBS) to investors. This ensures a steady flow of mortgage credit, influencing interest rates and availability.

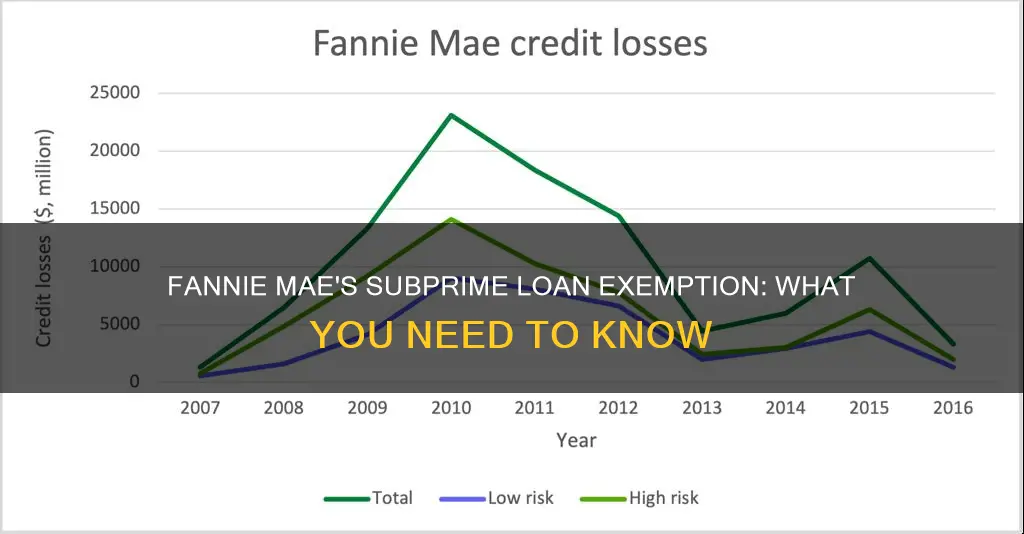

In the lead-up to the crisis, Fannie Mae and Freddie Mac started investing in riskier loans, contributing to a housing bubble. They purchased large volumes of Alt-A mortgages, which had higher LTV and DTI ratios and often lacked full documentation of borrowers' incomes. They also bought private-label MBS collateralized by subprime mortgages, i.e. loans issued to borrowers with poor credit ratings. This was driven by pressure from banks, thrift institutions, and mortgage companies to make more loans to so-called subprime borrowers, and by federal government initiatives to expand lending to low-income and minority borrowers.

As a result of these factors, the GSEs found it increasingly difficult to find creditworthy borrowers. In response, they reduced their underwriting standards and dove into the subprime mortgage market. This involved reducing the accepted credit score, lowering the required down payment, raising the debt-to-income ratio, or accepting low or no documentation. For example, by 2000, they were accepting loans with zero down payment, and by 2006, 45% of first-time homebuyers were putting nothing down.

The actions of Fannie Mae and Freddie Mac fueled the subprime mortgage bubble, and when it burst, they were declared bankrupt by their managers. This caused an instantaneous loss in value for not only the subprime mortgages but also the prime mortgages. As they had provided default insurance on approximately half of all American home mortgages, their bankruptcy threatened to lead to the bankruptcy of any major holder of mortgages or securities based upon mortgages.

In September 2008, the Federal Housing Finance Agency (FHFA) announced that it would take over Fannie Mae and Freddie Mac. Both enterprises had become illiquid as the market for their bonds collapsed in the subprime mortgage crisis. They were placed under the direct supervision of the federal government and remain under conservatorship as of 2024.

Fannie Mae's Stance on PACE Loans

You may want to see also

![]()

The government's response to the financial crisis

The US government's response to the 2008 financial crisis was influenced by the role of government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac in the preceding years. These enterprises are pivotal in the secondary mortgage market, buying and securitizing mortgages, and ensuring a steady flow of mortgage credit.

In the years leading up to the financial crisis, Fannie Mae and Freddie Mac began investing in riskier loans, contributing to a housing bubble. They purchased large volumes of Alt-A mortgages, which often lacked full documentation of borrowers' incomes and had higher loan-to-value (LTV) and debt-to-income (DTI) ratios. Additionally, they bought private-label mortgage-backed securities (MBS) collateralized by subprime mortgages, which were issued to borrowers with poor credit ratings.

The roots of this situation can be traced back to the 1990s, when the Clinton administration, under pressure from various groups, expanded federal government servicing of low-income and minority borrowers through "affordable housing goals." This created a quota system, requiring a certain percentage of the loans acquired by GSEs annually to be made to borrowers in financially vulnerable communities or those with incomes at or below the community median. As these goals were continuously raised, GSEs found it challenging to find creditworthy borrowers, leading them to reduce their underwriting standards and dive into the subprime mortgage market.

The federal government's direct involvement in promoting homeownership and its implicit guarantee to Fannie Mae and Freddie Mac played a significant role in the expansion of the subprime bubble. As a result, when the financial crisis hit, the government had to intervene to prevent a wider economic fallout. In July 2008, Congress passed the Housing and Economic Recovery Act, establishing the Federal Housing Finance Agency (FHFA) to regulate and oversee the GSEs' capital standards and limit their mortgage investment portfolios. The government also provided a bailout to Fannie Mae and Freddie Mac, highlighting the interconnectedness of the government and these enterprises in the lead-up to and response to the financial crisis.

FAFSA Loans: Do They Cover Summer Classes?

You may want to see also

![]()

How Fannie Mae operates

The Federal National Mortgage Association, typically known as Fannie Mae, is a United States government-sponsored entity that was established to expand the secondary mortgage market by making mortgages available to low and middle-income borrowers. It does not provide mortgages to borrowers but purchases and guarantees mortgages through the secondary mortgage market.

Fannie Mae was established in 1938 by the US Congress during the Great Depression as part of the New Deal instituted by President Franklin Roosevelt to manage the effects of the economic downturn. Its role was to grow the mortgage market by securitizing mortgages, thus allowing lenders to reinvest the assets into more lending and reducing reliance on local banks.

Fannie Mae operates a hotline to help people with housing-related financial problems. After purchasing mortgages on the secondary market, Fannie Mae pools them to create packages of mortgage-backed securities (MBS). These securities are purchased as investments by large institutional buyers such as insurance companies, pension funds, and investment banks. Fannie Mae guarantees payments of principal and interest on its MBS.

Fannie Mae also has its own portfolio, commonly referred to as a retained portfolio. This invests in its own mortgage-backed securities and those from other institutions. To fund its retained portfolio, Fannie Mae issues debt called agency debt.

In 1968, Fannie Mae transitioned from a government entity to a quasi-governmental corporation owned by shareholders. This enabled the entity to buy any mortgage, including those listed on the New York Stock Exchange. During the 2008 financial crisis, the subprime mortgage crisis affected Fannie Mae’s ability to purchase new mortgages from the market. Lenders engaged in unethical lending practices by granting loans to borrowers with poor credit history, which led to the housing bubble bursting. Despite government attempts to revive the entity, it plunged into debt. In late 2008, Fannie Mae and Freddie Mac were taken over by the government through a conservatorship of the Federal Housing Finance Committee (FHFC).

Explicit Costs: Are Loans Included?

You may want to see also

![]()

The risks associated with subprime loans

Subprime loans are associated with a variety of risks, both for the borrower and the lender.

For borrowers, subprime loans often come with higher interest rates and fees, making them significantly more expensive than traditional mortgages. This is because subprime borrowers are considered to have a higher risk of defaulting on their loans. The higher interest rates reflect the greater risk to lenders. Subprime loans can also be risky and expensive if they are set up as interest-only mortgages, where the borrower only pays the interest each month for a set period. If the borrower is unable to make their payments, their credit score will be damaged, and they may lose their home to foreclosure.

For lenders, subprime lending involves assuming a higher level of credit, compliance, transaction, and reputation risk, among others. Lenders must be cautious and engage in comprehensive due diligence, as well as have a well-developed business plan that acknowledges the increased risk levels. Examinations of national banks that participate in subprime lending have uncovered serious weaknesses in the business and control processes used to manage the associated risks. Lenders must also be aware that only a few have the ability to measure profitability at the product, portfolio, and customer level, increasing the likelihood of inappropriate strategic decisions.

Additionally, the practice of securitization, where loans are bundled and sold as securities to investors, has contributed to financial crises, such as the one in 2008. Securitization allows lenders to transfer default risk to investors, but it also adds complexity to the lending process and can lead to financial instability and economic crises if not properly managed.

In conclusion, subprime loans pose risks for both borrowers and lenders, including higher interest rates, increased risk of default, and potential financial instability. It is important for both parties to carefully consider the risks and seek alternatives when possible.

Failing a Semester: Can You Still Get Loans?

You may want to see also

![]()

The future of Fannie Mae

The Federal National Mortgage Association, commonly known as Fannie Mae, has played a pivotal role in the secondary mortgage market since its inception in 1938. Over the years, it has faced challenges, including the 2008 subprime mortgage crisis, which led to a government bailout and conservatorship.

Fannie Mae's future appears focused on promoting equitable and sustainable access to homeownership and affordable rental housing. In 2021, they launched initiatives to support low-income homeowners and renters, such as RefiNow™, which helps reduce mortgage costs by lowering barriers associated with refinancing. They also continued their Here to Help campaign, providing COVID-19 relief options and resources to those affected by the pandemic.

Fannie Mae has also been working to address disparities in homeownership, particularly for Black borrowers, by identifying challenges and sharing findings with the industry. They have implemented inclusion policies and initiatives, such as the Future Housing Leaders® program, to promote diversity and create career opportunities for underrepresented groups in the housing industry.

Looking ahead, the Federal Housing Finance Agency (FHFA) has established affordable housing goals for 2025-2027, with annual benchmarks to support equitable housing access for low-income families and those in low-income areas. These goals aim to ensure that Fannie Mae and other enterprises effectively advance their missions and support housing finance markets in a safe and sound manner.

While the structure and role of Fannie Mae in the mortgage finance market remain largely unchanged since the pre-crisis days, there is an ongoing discussion about revisiting their breadth, goals, and structure to shape the future of housing finance.

Who Owns My Mortgage Loan? Fannie, Freddie, and You

You may want to see also

Frequently asked questions

Fannie Mae is a government-sponsored enterprise that provides liquidity, stability, and affordability to the mortgage market. It is exempt from state and local taxes.

No, Fannie Mae does not exempt subprime loans. In fact, it played a significant role in the 2008 subprime mortgage crisis. However, it does provide support to low- to moderate-income borrowers to obtain financing for a home.

A subprime loan is a loan given to borrowers whose incomes, credit ratings, and savings are not good enough to qualify for conventional loans. These borrowers are considered higher-risk and are charged higher interest rates.