LendingTree is an advertising-supported comparison service that helps users find the best deal on their loans. It provides multiple offers from several lenders, allowing users to compare and choose the best option for them. LendingTree does not include all lenders, savings products, or loan options available in the marketplace, and the company is compensated by the companies on its site, which may impact how and where offers appear. Debt consolidation loans are the most popular product on the LendingTree marketplace, with 50.7% of LendingTree users taking out a personal loan to consolidate debt or refinance their credit cards in the third quarter of 2024.

| Characteristics | Values |

|---|---|

| Type of loan | Debt consolidation loan |

| Loan amount | $1,000 - $100,000 |

| Interest rate | Varies, but lower than credit cards |

| Credit score requirement | 620 or higher |

| Lender compensation | LendingTree is compensated by companies on its site, which may impact how and where offers appear |

| Lender network | LendingTree works with a network of 300+ lenders |

| Loan options | LendingTree does not include all lenders, savings products, or loan options available in the marketplace |

| Additional services | Credit monitoring, budgeting insights, personalized financial recommendations |

What You'll Learn

![]()

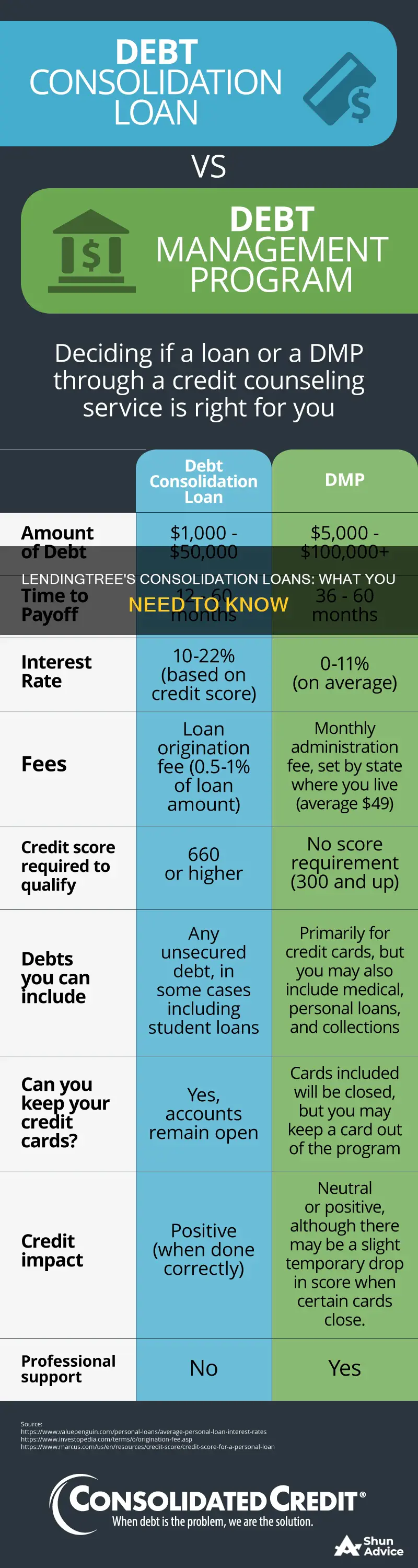

Debt consolidation loans vs bankruptcy

Debt consolidation loans and bankruptcy are two ways to help manage your debt. However, they have very different implications for your financial situation and credit score.

Debt consolidation loans are a type of personal loan that you can use to pay off multiple existing debts, such as credit cards, medical bills, or personal loans. Consolidation loans typically have lower interest rates than credit cards, so they are a cheaper way to repay high-interest credit card balances. For example, if you have $10,000 in credit card debt, you could save up to $3,000 in interest by using a debt consolidation loan. Consolidation loans can also improve your credit score by streamlining your monthly budget and making it easier to make on-time payments. However, you will still have to pay the full amount you owe, and there may be fees associated with the loan that can add up.

Bankruptcy, on the other hand, is a legal process that can reduce, restructure, or eliminate your debt. It can be a complicated and expensive process, and it will have a significant negative impact on your credit score, making it difficult to obtain loans or credit cards in the future. Bankruptcy may be a good option if you are unable to make payments on your debt and need a fresh start financially. It can also delay repossession or foreclosure on a secured loan, such as a mortgage or auto loan. However, it is important to note that bankruptcy may result in losing many of your assets, and it will remain on your credit report for seven to ten years.

In summary, debt consolidation loans can help you manage your debt by providing a single loan with a lower interest rate, which can improve your credit score if you make on-time payments. Bankruptcy, on the other hand, is a more extreme measure that can reduce or eliminate your debt but will have a significant negative impact on your credit score and may result in losing assets. Consolidation loans are generally a better option if you can afford to make payments and are committed to improving your financial situation, while bankruptcy may be a last resort if you are unable to manage your debt through other means.

Lending Club: Can You Refinance Existing Loans?

You may want to see also

![]()

How does LendingTree get paid?

LendingTree is an online lending marketplace that connects consumers to multiple banks and loan companies. It does not charge consumers for its services. Instead, LendingTree is compensated by the companies on its site, such as banks and specialty mortgage lenders, who pay to join its network. This compensation may impact how and where offers appear on the site. LendingTree does not include all lenders, savings products, or loan options available in the marketplace.

LendingTree is not a mortgage provider or broker, and it does not make any approval decisions itself. Instead, it passes users' information to its network of lenders, who decide whether or not to extend an offer based on their loan criteria. LendingTree allows users to connect with multiple loan operators to find optimal terms for loans, credit cards, deposit accounts, and insurance.

While LendingTree does not charge consumers a fee for its services, there may be costs associated with the loan application process, such as processing fees, appraisal fees, and title fees. These fees are typically paid to the lender and are standard when obtaining a mortgage. It is important for consumers to carefully review and compare quotes from multiple lenders before proceeding with a loan application to ensure they are getting the best deal.

By using LendingTree, consumers can benefit from having multiple lenders compete for their business, which can result in better deals and lower rates. LendingTree provides a convenient "one-stop-shop" for loan needs, offering choice, convenience, and value while helping users find the lender that best suits their needs.

Lending Club Loan App: What You Need to Know

You may want to see also

![]()

Debt relief options

Debt consolidation loans are the most popular product on the LendingTree marketplace. In the third quarter of 2024, 50.7% of LendingTree users took out a personal loan to consolidate debt or refinance their credit cards. A debt consolidation loan is a type of personal loan that you use to pay off multiple existing debts, such as credit cards or medical bills. It doesn't get rid of your debt but consolidates many smaller debt bills into one big debt bill. Consolidating your debt can help streamline your monthly budget and save you money on interest if your consolidation loan has a lower APR than what you're currently paying.

LendingTree's monthly credit card study shows that the average credit card APR is 24.84%, while debt consolidation loans have an average APR of 18.66% for credit scores of 720 and above. This means that if you have excellent credit, you could pay less overall interest on a debt consolidation loan. For example, you could save up to $3,000 in interest by paying off $10,000 in credit card debt with a debt consolidation loan.

It's important to note that debt relief options come with risks. For example, if you don't change your spending habits after consolidating, you may end up in more debt. Additionally, secured loans like auto loans and mortgages are usually not eligible for debt relief. Debt relief focuses on unsecured debts like credit cards, personal loans, personal lines of credit, and private student loans.

When considering debt relief options, it's essential to do your research and compare different lenders to find the best option for your financial situation.

Understanding Land Loans: The NOI Factor

You may want to see also

![]()

Credit score impact

Debt consolidation loans are the most popular product on the LendingTree marketplace. In the third quarter of 2024, 50.7% of LendingTree users took out a personal loan to consolidate debt or refinance their credit cards.

A debt consolidation loan can help improve your credit score. A LendingTree study found that using a personal loan to pay off debt could boost your credit score by 80-plus points after only one month. As long as your lender reports your on-time payments to credit bureaus, your score will continue to increase.

However, it is important to note that a debt consolidation loan is not a solution to get rid of your debt. Instead, it is a way to trade in multiple smaller debt bills for one big debt bill. It can help streamline your monthly budget and save you money on interest if your consolidation loan has a lower APR than what you are currently paying on your debt.

When it comes to obtaining credit, including personal loans, a higher credit score generally leads to better interest rates from lenders. Your credit score indicates to lenders how likely you are to repay a loan on time and in full. Therefore, the higher the credit score, the lower the perceived risk for the lender.

Even borrowers with bad credit can find lenders willing to work with them. However, it is important to pay attention to maximum APRs, as these are the ones most likely to apply to borrowers with bad credit.

Additionally, while debt consolidation can help improve your credit score, there are risks involved. For example, if you do not change your spending habits after consolidating, you may end up accumulating more debt. Furthermore, late credit card payments or debt settlement can hurt your credit score. Any settled accounts will appear as "settled" on your credit report for up to seven years, indicating to future lenders that you may have trouble with your next loan.

LendingTree also offers debt relief options for those with multiple credit cards who can afford their current debt and have solid credit. Debt relief can help reduce your interest rates or the total amount you owe by reorganizing or settling your debt. However, it is important to carefully review the options and understand the risks involved, as missteps could cost you money and your credit score.

Lazada's Loan Services: What You Need to Know

You may want to see also

![]()

Best debt consolidation loan options

Debt consolidation loans are a good option for those looking to streamline their monthly payments. They are particularly useful for consolidating high-interest debt, like credit card debt.

- LightStream: LightStream is a highly regarded lender for many loan types, including debt consolidation. It offers consistently low-interest rates and a rate beat program to ensure you get the lowest rate on your consolidation loan. However, LightStream only works with borrowers with good or better credit and does not offer prequalification.

- Avant: Avant is a good option for borrowers with lower credit scores who need to receive their loan money quickly. Avant offers loans ranging from $2,000 to $35,000 with interest rates starting higher than other lenders.

- Upgrade: Upgrade is one of the best companies to consolidate debt because it offers fast cash and affordable loans ranging from $10,000 to $50,000 with low fixed rates and no prepayment penalties.

- SoFi: SoFi is the best option for anyone with a high balance, as it offers debt consolidation loans of $5,000 to $100,000. SoFi does not have any application or prepayment fees.

- Upstart: Upstart is a good option for borrowers with poor credit but strong work histories and education. It offers loans up to $50,000 and potential qualification without a credit history.

- Achieve: Formerly known as Freedom Plus, Achieve offers a debt consolidation discount and a co-borrower option, as well as an impressive array of additional perks not offered by competitors. It is a good match for borrowers with strong work histories and education but poor credit.

Factors to Consider

When choosing a debt consolidation loan, consider the following factors:

- Approval Requirements: Some lenders specialize in excellent credit borrowers, while others focus on helping bad credit borrowers. Check the lender's eligibility criteria to ensure they are a good fit for your credit score and financial situation.

- Interest Rates and Fees: Personal loan APRs vary widely based on your credit score and the lender. Compare interest rates and fees, including origination fees, to find the best option for you.

- Repayment Options: Most debt consolidation loan terms range from one to seven years. Consider the length of the repayment period and how it will impact your monthly payments and total interest charges.

- Credit Score Impact: Taking out a debt consolidation loan can impact your credit score. On-time payments can help improve your score, while late payments can hurt your credit.

It is important to research and compare different lenders and loan options to find the best debt consolidation loan that fits your needs and financial situation.

Lending Tree's Construction Loan Options: What You Need to Know

You may want to see also

Frequently asked questions

A debt consolidation loan is a type of personal loan that you use to pay off multiple existing debts, such as credit cards or medical bills. Instead of having multiple smaller debt bills, you will have one big debt bill.

LendingTree is an advertising-supported comparison service. It brings multiple lenders to you so you can compare personal loan offers in minutes. LendingTree is compensated by companies on the site and this may impact how and where offers appear.

To qualify for a debt consolidation loan, you will need a credit score of at least 620. You will also need to provide various documents and information.

A debt consolidation loan can save you money on interest if you can secure a lower APR. It can also improve your credit score by making you appear less risky to lenders.