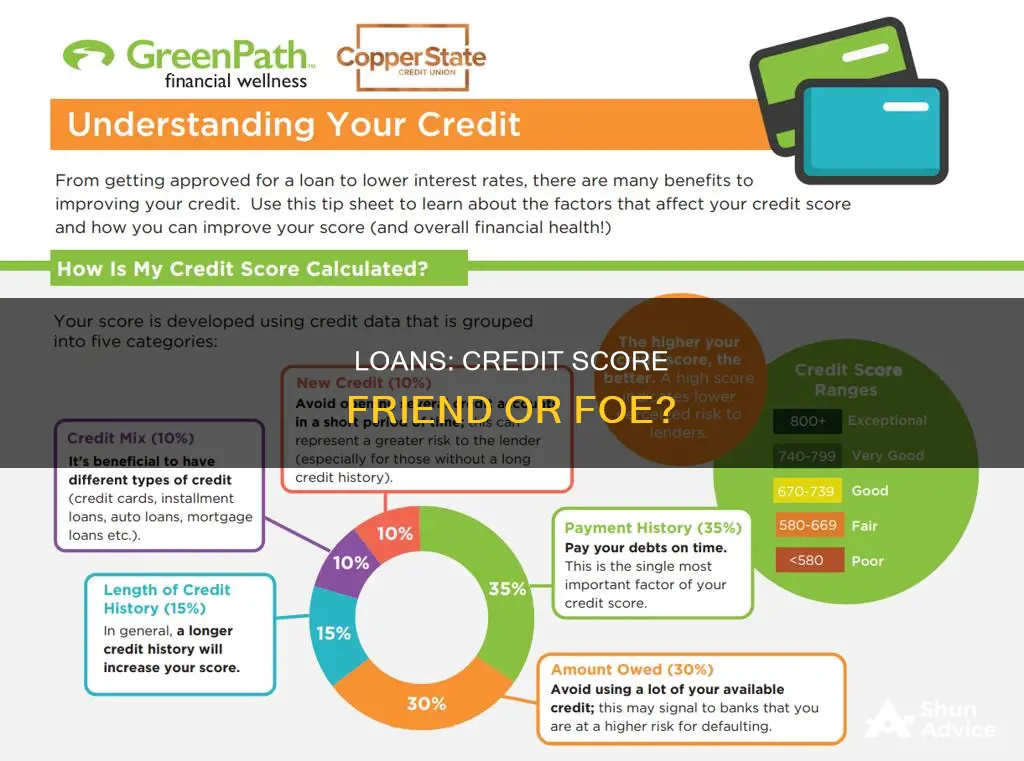

Taking out a loan can affect your credit score in several ways, depending on how you manage your account. When you apply for a loan, your credit score will take a slight hit as the lender performs a hard search on your credit report. However, making consistent, on-time payments can help improve your credit score over time by building a positive payment history. A personal loan can also add diversity to your credit mix, showing lenders that you can handle different types of credit responsibly. On the other hand, missing payments or defaulting on the loan can significantly damage your credit score. Therefore, it is essential to understand the risks and ensure you can afford the repayments before taking out a loan.

| Characteristics | Values |

|---|---|

| Impact on credit score | Can affect credit score positively or negatively |

| Positive impact | Helps build credit history, improves credit mix, reduces credit utilization |

| Negative impact | Increases debt load, slight hit to credit score in the short term, may lower the average age of credit accounts |

| Factors considered by lenders | Credit score, income, money in the bank, employment history |

What You'll Learn

- The impact of taking a loan on your credit score depends on how you manage the loan

- Making consistent, on-time payments can improve your credit score

- Missing payments can cause a significant drop in your credit score

- Applying for a loan can cause a temporary dip in your credit score

- A loan can help diversify your credit mix, improving your credit score

![]()

The impact of taking a loan on your credit score depends on how you manage the loan

Taking out a loan will impact your credit score, but whether this impact is positive or negative depends on how you manage the loan.

When you take out a loan, you increase your total debt load, which can negatively impact your credit score. Additionally, applying for a loan will result in a hard credit check, which can temporarily lower your credit score by a few points.

However, if you manage the loan responsibly, it can have a positive impact on your credit score. This includes making consistent, on-time payments, which can help build a positive payment history and improve your credit score over time. A personal loan can also add diversity to your credit mix, showing lenders that you are financially responsible and able to handle different types of credit.

It's important to understand the risks associated with taking out a loan and to be sure that you can afford the repayments. Missed or late payments will negatively impact your credit score and can stay on your credit report for up to seven years.

In summary, taking out a loan can have both positive and negative impacts on your credit score, but the overall effect depends on how well you manage the loan, including making timely repayments and maintaining a good credit mix.

Loans and Net Worth: A Complex Relationship

You may want to see also

![]()

Making consistent, on-time payments can improve your credit score

Taking out a loan will affect your credit score in several ways, and how you manage the loan is crucial. While applying for a loan can cause a slight dip in your credit score in the short term, making consistent, on-time payments can improve your credit score over time.

When you take out a loan, you increase your total debt load, which can negatively impact your credit score. Additionally, applying for a loan triggers a hard inquiry, which can lower your credit score by a few points. However, making consistent, on-time payments toward your loan can help you build a positive payment history and improve your credit score over time.

Payment history accounts for a significant portion of your credit score, and late or missed payments can stay on your credit report for up to seven years, damaging your creditworthiness. On the other hand, consistent, timely payments demonstrate financial responsibility and can increase your score over time.

It's important to establish a budget that includes all your debt repayments to avoid missing payments. Setting up automatic payments can ensure you pay on time. Additionally, consolidating high-interest credit card debt into a personal loan can improve your credit score by lowering your credit utilization ratio, which is another critical factor in determining your credit score.

In summary, while taking out a loan can impact your credit score in multiple ways, making consistent, on-time payments is a key factor in improving and maintaining a healthy credit score.

Borrowing from Your 401(k): Withdrawal or Loan?

You may want to see also

![]()

Missing payments can cause a significant drop in your credit score

Taking out a loan can impact your credit score in several ways, both positively and negatively. While applying for a loan can cause a slight dip in your credit score in the short term, consistently making timely payments can improve your credit score in the long run.

Missing payments, on the other hand, can cause a significant drop in your credit score. Even a single missed or late payment can negatively impact your credit score. The longer you wait to make the payment, the more severe the impact on your score. If you are more than 30 days past the due date, credit issuers will likely report the delinquency to at least one of the three major credit bureaus, resulting in a drop in your score. Payments that are 60 to 90 days past due will have an even greater effect on your score, and your interest rate may increase. If these payments remain unpaid, the credit issuer may send your debt to a collection agency, and the collection account will be recorded on your credit report. Records of late and missed payments can remain in your credit file for up to seven years.

The impact of missed payments on your credit score also depends on your credit history and payment behavior after missing a payment. If you quickly get back on track, your score will likely start improving, along with your good payment history. A history of on-time payments is crucial for a good credit score, and it is even better if you can pay them in full.

To avoid the negative consequences of missed payments, it is essential to manage your finances effectively and make timely payments according to the loan agreement. If you anticipate difficulties in making payments, communicating with your creditor in advance and exploring available options, such as hardship programs, can help mitigate the potential damage to your credit score.

Life Insurance Loan: Impact on Premium Payments?

You may want to see also

![]()

Applying for a loan can cause a temporary dip in your credit score

The FICO® Score and VantageScore® credit scoring systems treat applications to multiple lenders within a short time period (typically 14 to 45 days) as a single event. By contrast, multiple hard inquiries triggered by several credit card applications within a short timespan can have a cumulative negative effect on credit scores. You can use prequalification to estimate the interest rate and loan amount you can expect, and this will only use soft inquiries which do not affect credit scores.

Your credit score will be hurt if you pay late or default on the loan. However, if you make your payments on time, your credit score should improve. A personal loan can help you build your credit history and show that you can borrow responsibly. It can also help create a credit mix, which makes up 10% of your FICO score.

![]()

A loan can help diversify your credit mix, improving your credit score

Taking out a loan can affect your credit score in several ways, both positively and negatively. A loan can help diversify your credit mix, which can improve your credit score. Credit mix refers to the types of accounts that make up your credit report, including revolving credit and instalment credit. It accounts for 10% of your FICO score and is one of the five factors that influence it.

Having a diverse credit mix demonstrates that you can responsibly manage different types of credit, which can indicate that you are a reliable borrower. For example, if you only have credit cards and take out a personal loan, you can improve your credit mix. As you earn more income, you can typically take on additional forms of credit, such as a mortgage, auto loan, or unsecured credit card, further diversifying your credit mix.

However, it is important to note that opening too many new accounts within a short period can reflect badly on your credit score. Lenders are unlikely to focus on your credit mix when deciding whether to approve or deny a loan application. Instead, they will consider other factors, such as your income, employment status, and existing debts.

Additionally, your credit score may take a slight hit when you apply for a loan due to a hard inquiry, but this should be short-term as long as you pay it back according to the agreement. Properly managing your loan by making timely payments is crucial for improving your credit score in the long run.

Frequently asked questions

Taking a loan can affect your credit score positively or negatively, depending on how you manage the account. A loan can help build your credit history by showing that you can pay back a line of credit on time and in full.

Taking a loan can help create a credit mix, which is a small portion of your credit score. A credit mix shows that you can manage a variety of different accounts.

Yes, the type of loan can matter. For example, a personal loan is usually an unsecured debt, unlike mortgages and auto loans.

Your credit score plays a crucial role in helping you qualify for a loan. Lenders also consider other factors, such as your income, bank balance, and employment history.

To ensure that taking a loan helps improve your credit score, make consistent, on-time payments. Missing a payment can cause a notable drop in your credit score.