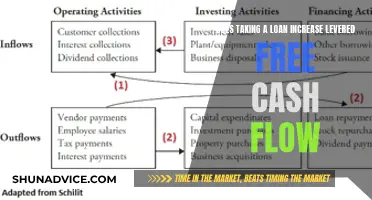

Securitization is a financial practice where various types of debt, such as mortgages, loans, and credit card debt, are pooled together and sold as securities to third-party investors. The originator initially owns the assets, but they are then sold to another entity, typically called the sponsor, who then sells the loan to a depositor. The depositor will assemble the underlying collateral and help structure the securities before selling them to investors. The securities are often split into tranches, or categories of varying risk levels, to cater to different investor risk appetites.

| Characteristics | Values |

|---|---|

| Who owns the loan before it is securitized? | The originator owns the loan before it is securitized. This is typically a company looking to raise capital, restructure debt, or adjust its finances. |

| Who is the depositor? | The depositor is the third entity that purchases the loan from the originator. The depositor typically owns 100% of the beneficial interest in the issuing entity and is usually the parent company or a wholly-owned subsidiary of the parent company. |

| What is the role of the depositor? | The depositor assembles the underlying collateral, helps structure the securities, and works with financial markets to sell the securities to investors. |

What You'll Learn

![]()

Securitization process

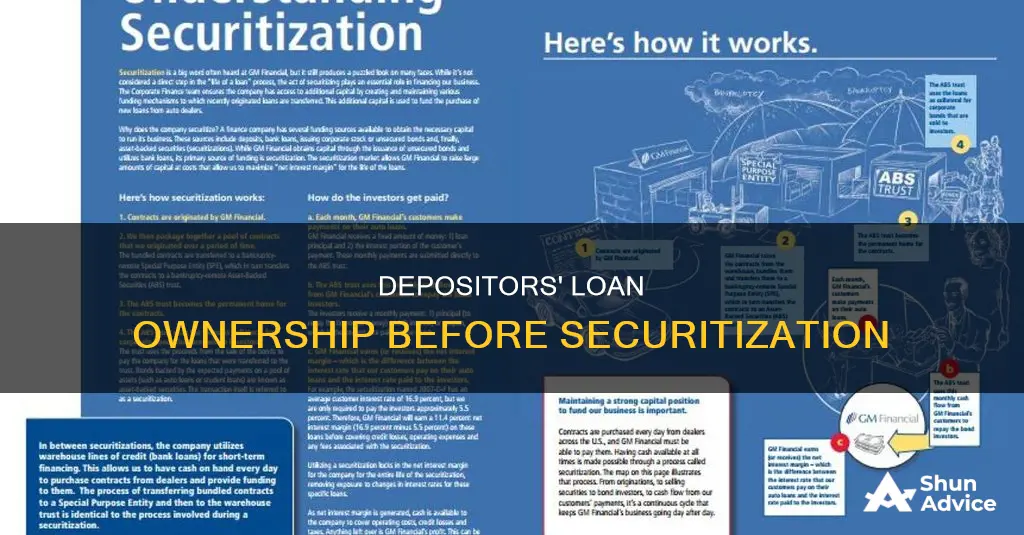

Securitization is a financial practice that involves pooling various types of debt—such as mortgages, auto loans, or credit card debt obligations—and selling them as securities to third-party investors. These securities can be described as bonds, pass-through securities, or collateralized debt obligations (CDOs). The process of securitization typically begins with an originator or a company that owns the assets and is looking to raise capital or restructure its finances. This company sells the loans to an entity called the Sponsor, which then sells the loan to a Depositor.

The Depositor is a critical player in the securitization process. The Depositor assembles the underlying collateral, helps structure the securities, and works with financial markets to sell the securities to investors. The Depositor typically owns 100% of the beneficial interest in the issuing entity and is often the parent company or a wholly-owned subsidiary of the parent initiating the transaction.

To fund the purchase of assets from the originator, the issuer creates tradable securities, which are then purchased by investors. These securities are often split into tranches, with varying degrees of risk exposure. The senior-most tranches, or the "A" class, have the highest level of credit protection, while the more junior "B" and "C" classes function as protective layers, absorbing losses before the senior tranches are affected.

The performance of the securities is directly linked to the performance of the underlying assets. Credit rating agencies rate the securities to provide an external perspective on the liabilities, helping investors make informed decisions. Securitization offers benefits such as improved liquidity, risk diversification, and more efficient capital allocation for both lenders and investors. However, it also carries significant risks, including reduced transparency, misaligned incentives, and potential systemic instability.

Ameritrade Share Loans: What Investors Need to Know

You may want to see also

![]()

Originator of the loan

The originator of a loan is the entity or institution that initiates the loan. This can be a lending company, mortgage broker, loan officer, or loan originator. In securitization terms, the originator is called the "seller". The originator of a loan is typically a company looking to raise capital, restructure debt, or otherwise adjust its finances.

A loan originator can be an individual or entity integral to creating a home loan. They help borrowers move through the mortgage origination process smoothly. This can include collecting credit and financial information, assessing the borrower's needs and loan options, negotiating rates, and submitting the application for underwriting.

Mortgage loan originators (MLOs) are licensed by a state or federal authority and must act in the consumer's best interests. They can work for a bank, credit union, or other lending institutions, large or small. Some are salaried, while many are compensated by commission. MLOs help borrowers through the mortgage application process, from initial inquiry to closing.

The originator initially owns the assets engaged in the deal. To buy the assets from the originator, the issuer SPV issues tradable securities to fund the purchase.

Co-op Bridging Loans: What You Need to Know

You may want to see also

![]()

Issuing securities

There are two main types of securities: equity and debt. Equity securities represent ownership interest held by shareholders in a company, partnership, or trust, and are realized in the form of shares of capital stock. Holders of equity securities are not typically entitled to regular payments, but they can profit from capital gains when they sell the securities. On the other hand, debt securities, such as government and corporate bonds, certificates of deposit (CDs), and collateralized securities, entitle the holder to regular interest payments and repayment of the principal, regardless of the issuer's performance. Debt securities can be secured (backed by collateral) or unsecured, and they are typically issued for a fixed term.

Securitization is a specific financial practice that involves pooling various types of contractual debt, such as mortgages, loans, or credit card debt obligations, and selling their related cash flows to third-party investors as securities. These securities may be described as bonds, pass-through securities, or collateralized debt obligations (CDOs). The cash flows collected from the underlying debt are used to repay the investors, and the performance of the securities is directly linked to the performance of the assets. Securitization can be particularly useful for companies looking to raise capital, restructure debt, or adjust their finances without diluting ownership and control through stock offerings or incurring the high costs of loans or bond financing.

The issued securities in securitization are often split into tranches, with different levels of credit protection or risk exposure. The senior ("A") class of securities has the highest level of protection, while the junior subordinated ("B", "C", etc.) classes function as protective layers, absorbing any losses before the upper-level tranches are affected. This arrangement is known as a cash flow waterfall. In the case of mortgage securitization, the process involves bundling many mortgages into a pool and then selling shares of that pool as bonds. This process also involves multiple parties, including the original lender (Seller), the Sponsor, and the Depositor, who transfers the loan into the trust.

Denver Botanic Gardens: Wheelchair Accessibility and Loaner Options

You may want to see also

![]()

Investor's role

Securitization is a financial practice that involves pooling various types of debt, such as mortgages, loans, or credit card debt obligations, and selling them to third-party investors as securities. These securities may take the form of bonds, pass-through securities, or collateralized debt obligations (CDOs). Investors play a crucial role in this process as they provide the capital required to purchase the assets from the originator.

The investors' role in securitization is multifaceted and involves several steps. Firstly, investors purchase the securities created by the issuer or special-purpose vehicle (SPV). These securities can be acquired through private offerings targeting institutional investors or on the open market. Credit rating agencies provide ratings for the securities to help investors make informed decisions by assessing the associated liabilities. Investors need to understand the level of risk they are undertaking, which can vary depending on the specific securitized product.

Once the investors have purchased the securities, they become the lenders for the underlying debt. They receive regular payments from the principal and interest cash flows generated by the underlying assets. These payments are typically made through a structured process, often referred to as a "waterfall." In this arrangement, senior or "A" class investors are prioritized for repayment, while junior or "B", "C" class investors receive payment only after the senior classes have been fully repaid. This cascading effect helps protect the upper-level investors from losses.

Additionally, investors benefit from credit enhancements that provide additional protection for the promised cash flows. These enhancements can help a security achieve a higher rating, making it more attractive to investors. Securitization also offers investors improved liquidity, risk diversification, and more efficient capital allocation. They can invest in assets that were previously unavailable to them, such as portions of mortgages or other loan-based securities, receiving regular returns from interest and principal payments.

However, it is important to note that securitization has faced criticism and concerns. The complexity and lack of transparency associated with some securitized products, particularly those involving subprime mortgages, have led to significant financial crises. Investors need to carefully assess the risks and understand the true nature of the underlying assets to make informed decisions.

Target Employee Loans: What's the Deal?

You may want to see also

![]()

Credit risk

Securitization is a financial practice that involves pooling various types of debt, such as mortgages, loans, and credit card debt obligations, and selling their related cash flows as securities to third-party investors. The process allows the original lender or creditor to remove these assets from their balance sheets, freeing up capital for additional lending.

In the context of securitization, the depositor is a critical entity in the chain of loan ownership. The original lender, known as the "seller," originates the loan and then sells it to another entity called the "sponsor." The sponsor, in turn, sells the loan to the "depositor," who then transfers the loan into a trust. This chain of ownership transfers is necessary to ensure that the mortgage-backed securities are "bankruptcy remote." In other words, if the original lender goes bankrupt, the subsequent sales of the loan protect it from being repossessed by a bankruptcy trustee.

Before the loan is securitized, the depositor owns the loan. The depositor assembles the underlying collateral, helps structure the securities, and works with financial markets to sell the securities to investors. The depositor typically owns 100% of the beneficial interest in the issuing entity and is often a parent company or a wholly-owned subsidiary of the parent initiating the transaction.

Teamsters Union: Unsecured Loans Available?

You may want to see also

Frequently asked questions

The originator, which could be a company or a bank, initially owns the loan before it is securitized.

The depositor purchases the loan from the originator and transfers it into a trust. The depositor typically owns 100% of the beneficial interest in the issuing entity.

Securitization allows companies to raise capital, restructure debt, or adjust their finances without diluting ownership or control through stock offerings or incurring high expenses through loans or bond financing.