Falling behind on loan payments can have serious consequences for borrowers, including a negative impact on their credit score and, in some cases, the loss of eligibility for federal student aid. A loan typically becomes delinquent the day after a missed payment, and if payments continue to be missed, the loan will eventually enter default. This can lead to a lawsuit being filed against the borrower by the lender to collect the debt. There are options available to those struggling with loan payments, such as loan modification or refinancing, and in some cases, loan forgiveness may be an option. It is important for borrowers to closely monitor their loans and be aware of the potential consequences of falling behind on payments to avoid these negative outcomes.

What You'll Learn

![]()

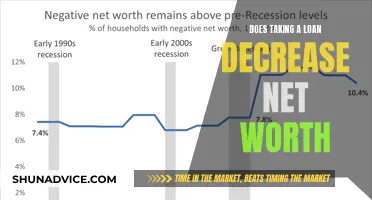

Student loan debt and credit scores

Student loans can impact your credit score in several ways. Firstly, they can increase the length of your credit history, which could raise your score. Secondly, they can add variety to your credit mix, which accounts for 10% of your score calculation. This shows lenders that you can manage different types of debt.

However, student loans can also negatively impact your credit score if you don't manage them properly. Payment history is the most important factor in determining your credit score, accounting for 35% of its calculation. If you miss a payment, you have 90 days before the loan is considered delinquent, after which missed payments will appear on your credit report and may decrease your score. Defaulting on a student loan can result in withheld wages and no further access to federal aid until the debt is settled or a repayment plan is approved. Delinquency or default can remain on your credit report for up to seven years.

Additionally, the large debt load from student loans can increase your debt-to-income (DTI) ratio, which lenders analyse when considering loan applications. It's important to treat student loans as you would any other debt to avoid negatively affecting your credit score. Make payments during your grace period, pay more than the minimum if possible, and consider enrolling in autopay to ensure timely payments.

Teach for America: Loan Forgiveness and You

You may want to see also

![]()

The impact of missing payments

Missing payments on loans can have a range of negative consequences and impact various areas of your life. It is important to understand the potential repercussions to avoid long-term financial difficulties. Here are some key impacts of missing loan payments:

Credit Score Impact

One of the most significant consequences of missing loan payments is the negative effect on your credit score. Payment history is the most important factor in determining your credit score, accounting for 35% of it. Even a single missed payment can lead to a decline in your credit score, and the impact can be more severe if you have a history of good credit. New student loan delinquencies can result in substantial deductions from your credit score, making it challenging to secure favourable terms for future credit needs, such as mortgages or new credit cards.

Increased Costs

Missing loan payments can result in increased costs in the form of late fees and penalty interest rates. Lenders may charge late fees if payments are made after the grace period has ended. Additionally, you may be subject to penalty interest rates on your remaining debt, increasing the overall cost of the loan.

Legal Action and Wage Garnishment

If you continue to miss payments, your lender may take legal action to recover the outstanding amount. This can result in legal fees and potential court judgments. In the case of default, lenders may seek court approval to garnish your wages, directly impacting your take-home pay.

Loss of Grace Period

By missing a payment, you may lose your grace period for future payments. A grace period is the time after your payment is due but before the lender charges a late fee. Typically, a grace period lasts for 15 days, and making a payment within this period can help you avoid late fees.

Impact on Career Trajectory and Living Situation

The negative impact on your creditworthiness due to missed payments can affect your career trajectory and even where you can afford to live. A low credit score may result in increased costs and decreased approvals for loans and services, potentially limiting your options in various aspects of your life.

It is important to note that if you are struggling to make payments, there may be resources and options available to assist you. Proactive financial management and seeking guidance from a loan expert can help you understand your choices and create a plan to avoid the consequences of missed loan payments.

Life Insurance Loan: Impact on Premium Payments?

You may want to see also

![]()

Loan forgiveness

The Biden administration's plans for student loan forgiveness have faced legal challenges. As of March 2025, student loan delinquencies are projected to reach record highs, with over 9 million borrowers at risk of seeing their credit scores drop. The New York Fed estimates that around 15.6% of federal loans were past due at the end of 2024, amounting to over $250 billion in delinquent debt.

In the context of the pandemic, stimulus checks and payment pauses allowed some borrowers to reduce their balances. However, others faced challenges as their loans became politicised. The scale of past-due loans is dynamic, with borrowers potentially curing their delinquency or falling further behind on payments. The impact of these factors will be clarified with the release of updated data.

It is worth noting that loan forgiveness programs have also been subject to scrutiny. For instance, the Justice Department launched an investigation into a Rhode Island school district's "Educator of Color Loan Forgiveness Program." The investigation aims to determine if the program, funded by the Rhode Island Foundation, discriminates against White teachers.

The Fed's Lending Power: Individual Access Explored

You may want to see also

![]()

Interest accrual

Accrued interest is a result of accrual accounting, which requires that accounting transactions be recognised and recorded when they occur, regardless of whether payment has been received or made. This means that even if you're not currently making loan payments, interest continues to accrue and grow. The revenue recognition principle, which states that revenue should be recognised in the period it is earned rather than when payment is received, is relevant here. Additionally, the matching principle, which states that expenses should be recorded in the same accounting period as related revenues, also comes into play.

For example, consider a business that takes out a loan to purchase a company vehicle. The company will owe the bank interest on the vehicle on the first day of the month following the loan. However, the company has had use of the vehicle for the entire previous month, generating revenue. At the end of each month, the business will need to record the interest that it expects to pay out on the following day. This interest is calculated as of the last day of the accounting period and is reported on the income statement as revenue or expense, depending on whether the entity is lending or borrowing.

The impact of accrued interest on the total loan cost is significant. It is added to the principal amount of the loan, increasing the overall cost. This is why it is important for borrowers to understand how interest accrual works and to be aware of their lender's policies. By making informed decisions and staying proactive, borrowers may be able to reduce their total loan cost.

In certain cases, such as with the U.S. Department of Education's Saving on a Valuable Education (SAVE) Plan, interest may not accrue during a period of forbearance. However, it is important to note that this can vary depending on the specific terms of the loan and the applicable laws and regulations.

Tesla's Loan Denial: What's the Real Reason?

You may want to see also

![]()

Loan repayment plans

There are several loan repayment plans available, which can be categorised into two main types: traditional and income-driven repayment (IDR) plans. The best repayment plan for you will depend on your financial situation and goals.

Traditional Repayment Plans

Traditional repayment plans base the borrower’s monthly payment on how much was borrowed and the plan’s repayment term. The four main repayment plans for Federal education loans are:

- Standard Repayment: Under this plan, you will pay a fixed monthly amount for a loan term of up to 10 years. The loan term may be shorter than 10 years, depending on the amount of the loan, and there is a $50 minimum monthly payment.

- Extended Repayment: This plan is similar to the standard repayment plan, but allows for a loan term of 12 to 30 years, depending on the total amount borrowed. While stretching out the payments over a longer term reduces the size of each payment, it increases the total amount repaid over the lifetime of the loan.

- Graduated Repayment: This plan starts with lower payments that gradually increase every two years. The loan term is 12 to 30 years, depending on the total amount borrowed. The monthly payment can be no less than 50% and no more than 150% of the monthly payment under the standard repayment plan, and must be at least $25.

- Income-Sensitive Repayment: This plan pegs the monthly payments to a percentage of gross monthly income. The loan term is 10 years.

Income-Driven Repayment (IDR) Plans

IDR plans tie the amount you pay to a portion of your income and extend the length of time you're in repayment. The four types of IDR plans are:

- Income-Based Repayment (IBR): Similar to income-contingent repayment, IBR caps the monthly payments at a lower percentage of a narrower definition of discretionary income.

- Income-Contingent Repayment (ICR): Payments under the ICR plan are based on the borrower’s income and the total amount of debt. Monthly payments are adjusted each year as the borrower’s income changes. The loan term is up to 25 years, at the end of which any remaining balance on the loan will be discharged. The write-off of the remaining balance is taxable under current law.

- Pay As You Earn (PAYE): This is one of the IDR plans offered by the government.

- Saving on a Valuable Education (SAVE): This plan will no longer be available after 1 July 2024. Monthly payments are capped at 10% of the borrower's income, and the loan term is up to 20 years. At the end of the term, any remaining balance is forgiven, but the amount forgiven is taxable.

Knights of Columbus: Insurance and Loan Services

You may want to see also

Frequently asked questions

If you miss a payment, your loan becomes delinquent. If you continue to miss payments, your loan will eventually enter default. For most federal loans, this occurs after 270 days, or approximately 9 months. Once your loan is in default, the lender can file a lawsuit against you to collect on the debt.

There are several options for dealing with past-due mortgage payments. You may qualify to modify your mortgage, which may include lowering the payments or interest rates. Your lender may extend the term of the loan or reduce the balance of your loan by forgiving the past-due payments. Some homeowners refinance their mortgage when they fall behind in making the mortgage payments. If you want to give up your home, Chapter 7 bankruptcy may be a better option.

FHA loans might fall through due to a low credit score, insufficient funds, too much debt, and/or property-related issues. To avoid having your FHA loan fall through due to insufficient funds, start saving money as early as possible.