Mortgage-backed securities (MBS) are investments similar to bonds that consist of a bundle of home loans bought from the banks that issued them. MBS are priced according to the cost of buying $100 of a particular bond. For example, if the price of an MBS bond is 101.00, an investor pays $101.00 and owns $100.00 worth of the bond. MBS prices are influenced by economic growth and inflation, with economic reports released daily affecting prices. MBS prices are also inversely related to interest rates, meaning that existing MBS become less valuable when interest rates rise.

| Characteristics | Values |

|---|---|

| Type of investment | Mortgage-backed securities (MBS) are an investment like a bond |

| Composition | MBS are comprised of groups of similar mortgages, also known as "pools" |

| Function | MBS function similarly to other bonds in that they have a purchase price and pay the investor back in installments based on the yield |

| Price | The price refers to the cost of buying $100 of a particular bond. For instance, if the price of a bond is 101.00, the investor pays $101.00 and owns $100.00 worth of that bond |

| Yield | Yield is the rate of return paid on a bond over time. The coupon yield of a particular MBS determines the rate of return of the principal amount remaining in the MBS pool purchased by the investor |

| Coupon | The coupon doesn't change, but the price does. The higher the coupon of MBS, the higher the price will generally be |

| Interest rate | MBS pay a fixed interest rate that is usually higher than US government bonds. MBS prices are inversely related to interest rates |

| Payouts | MBS typically offer monthly payouts, while bonds offer a single lump-sum payout at maturity |

| Risk | MBS are considered relatively low-risk, given the government backing for most of them |

| Market growth | The growth of the MBS market can be attributed to increasing demand for these securities, global economic expansion, and efforts to stimulate economic growth through monetary policy |

| Market challenges | The market faces challenges such as interest rate risk, refinancing, and economic downturns leading to mortgage defaults |

| Impact of economic growth | Economic growth and inflation impact MBS prices. Good economic news often sinks MBS prices |

| Impact of economic reports | Economic reports with measurements of economic strength and inflation influence MBS prices |

| Impact of inflation | Higher inflation leads to a higher cost of borrowing money, which can sink MBS prices |

What You'll Learn

![]()

The relationship between MBS and interest rates

Mortgage-backed securities (MBS), as investment-grade bonds, provide investors with an opportunity to enter the mortgage market amidst interest rate uncertainty. MBS are essentially bonds backed by a collection of home loans, creating a unique investment product. The performance of MBS is closely tied to interest rates, and any changes in interest rates can significantly impact the value of MBS.

When interest rates rise, it can lead to a decline in the market value of MBS. This is due to the inverse relationship between bond prices and interest rates. Higher interest rates make newer bonds more attractive because they offer higher yields, reducing the appeal of existing bonds with lower yields. This dynamic is particularly relevant for long-term MBS exchange-traded funds (ETFs), as they are more sensitive to rate changes. As a result, fund managers employ various strategies to mitigate the negative impact of rising interest rates, such as shortening the duration of their holdings to focus on securities less sensitive to rate hikes.

On the other hand, when interest rates are low, MBS can become more attractive to investors. In this scenario, investors are willing to pay a premium for MBS, driving up their prices. This increased demand for MBS can lead to a corresponding decrease in mortgage interest rates, as lenders adjust their rates to remain competitive.

It's important to note that MBS prices also incorporate the level of risk associated with the underlying loans. For example, MBS backed by mortgages that allow lower credit scores may be priced lower and have higher yields due to the increased default risk. Additionally, economic factors such as inflation and economic growth play a crucial role in influencing MBS prices and interest rates. Positive economic news and higher inflation rates can drive up the cost of borrowing, affecting the demand for MBS and interest rates.

In summary, the relationship between MBS and interest rates is intricate and constantly evolving. Investors and fund managers must carefully navigate this landscape, considering various factors such as interest rate movements, economic indicators, and the level of risk associated with MBS, to make informed investment decisions.

Factors That Determine Mortgage Amounts

You may want to see also

![]()

How economic growth and inflation influence MBS pricing

The two factors with the most impact on MBS interest rates are economic growth and inflation. Economic growth and inflation are closely linked, and both have a significant influence on MBS pricing.

Economic Growth

A growing economy increases the demand for capital, which leads to a higher cost for borrowing money. This is why positive economic news often coincides with a drop in MBS prices. As the economy grows, there is also a higher demand for resources, which can lead to inflation.

Inflation

Inflation refers to a broad rise in the prices of goods and services across the economy over time, which erodes purchasing power. Central banks play a key role in managing inflation by setting interest rates and influencing inflation expectations. When inflation is high, the purchasing power of money decreases, and the value of debt is reduced. Conversely, during deflation (when prices fall), debt becomes more expensive, and investments such as stocks, corporate bonds, and real estate become riskier.

Demand-Pull Inflation

Demand-pull inflation occurs when demand for goods and services exceeds the economy's ability to produce them sustainably. This excess demand puts upward pressure on prices, leading to an increase in inflation. For example, when demand for new cars recovered quickly after the COVID-19 pandemic, a shortage of semiconductors caused a spike in new and used car prices.

Cost-Push Inflation

Cost-push inflation is caused by rising input costs, which increase the price of final goods and services. For instance, an increase in the price of oil can lead to higher petrol prices, which then affect the transportation of goods and, consequently, the prices of groceries and other items.

Imported Inflation

Imported inflation refers to how the exchange rate influences inflation through exported and imported goods and services. The exchange rate can affect the prices of tradable goods and services, while non-tradable goods and services are influenced more by domestic developments.

Inflation Expectations

Inflation expectations refer to the beliefs that households and firms have about future price increases. These expectations can influence current economic decisions and impact actual inflation outcomes. For example, if firms expect higher inflation, they may raise their prices, and workers may demand higher wages to compensate for the expected loss in purchasing power.

In summary, economic growth and inflation are key factors that influence MBS pricing. Economic growth drives demand for capital and resources, impacting borrowing costs and inflation. Inflation, in turn, affects purchasing power, debt values, and investment risk. Demand-pull, cost-push, and imported inflation dynamics, as well as inflation expectations, further shape the inflationary environment, ultimately influencing MBS pricing.

Markets: Money, Bonds, Stocks, and Mortgages, What's the Commonality?

You may want to see also

![]()

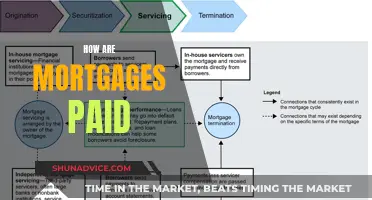

How MBS function like other bonds

Mortgage-backed securities (MBS) are investments that function similarly to bonds. They are created out of a pool of residential mortgages, providing income to investors. MBSs are formed by pooling together mortgages, which are then sold to investors on the secondary market. The investor who buys an MBS is essentially lending money to homebuyers. MBSs are similar to other bonds in that they have a purchase price and pay the investor back in instalments based on the yield. The price of an MBS is influenced by prepayment speed, usually measured in units of CPR or PSA. MBSs are considered to have a higher yield than other fixed-income securities.

MBSs pay a fixed interest rate that is usually higher than US government bonds. They typically offer monthly payouts, while bonds offer a single lump-sum payout at maturity. MBSs are also considered relatively low-risk, given the government backing for most of them. If an MBS is guaranteed by the federal government, investors do not have to bear the costs of a borrower's default. MBSs offer diversification from the markets of corporate and government securities.

The total face value of an MBS decreases over time. Unlike bonds and most other fixed-income securities, the principal in an MBS is not paid back as a single payment to the bondholder at maturity. Instead, it is paid along with the interest in each periodic payment (monthly, quarterly, etc.). This decrease in face value is measured by the MBS's "factor", the percentage of the original "face" that remains to be repaid.

MBSs have a prepayment function (or prepayment risk), independent of the interest rate. This includes economic growth, regulatory risk, demographic trends, and a shifting risk aversion profile. Prepayment can be either voluntary, such as when borrowers refinance or relocate, or involuntary, such as defaults. MBSs also have a credit risk that depends on the likelihood of the borrower paying the promised cash flows (principal and interest) on time. MBSs issued by government-sponsored enterprises (GSEs) like Fannie Mae, Freddie Mac, and Ginnie Mae are considered to have the highest credit, given their government backing.

Incorporate Closing Costs: Folding Them into Your Mortgage

You may want to see also

![]()

The effect of refinancing on MBS pricing

The pricing of mortgage-backed securities (MBS) is influenced by several factors, including economic growth, inflation, and interest rates. MBS prices are also impacted by refinancing activities, which can affect the duration of MBS and the level of prepayments.

When interest rates fall, refinancing typically increases as homeowners seek to take advantage of lower-rate mortgages. This results in what is known as negative convexity, where the duration of MBS falls, and MBS may not fully benefit from the price appreciation associated with declining interest rates. To compensate investors for this risk, MBS may offer a higher yield or spread compared to US Treasury securities.

The impact of refinancing on MBS pricing can be influenced by various factors, including the level of interest rates, the cost and hassle associated with refinancing, and the availability of alternative investment options. For example, if the potential savings from refinancing are relatively low, such as $20-50 per month, some homeowners may decide that it is not worth the effort and expense. This could lead to lower prepayment rates and potentially stabilize MBS durations.

Additionally, the Federal Housing Finance Agency's (FHFA) Uniform Mortgage-Backed Security (UMBS) program and similar initiatives have been introduced to constrain excessive refinancing and its potential impact on MBS. These programs aim to standardize and regulate the mortgage market, reducing the risk of significant deviations in prepayment performances by mortgage originators.

It's worth noting that the current environment, as of August 30, 2024, does not provide a financial incentive for homeowners to refinance. On the contrary, it disincentivizes refinancing, as homeowners would be giving up their "cheap" mortgages for more expensive ones. As a result, prepayments are expected to remain low, contributing to the stability of MBS durations and allowing the MBS sector to benefit from declining interest rates.

Mortgage Advising: After the Loss of a Spouse

You may want to see also

![]()

The role of MBS in the 2007 financial crisis

The global financial crisis of 2007–2009 was a period of extreme stress in global financial markets and banking systems. The crisis was caused by a combination of factors, including the securitization of bad loans, falling US house prices, and a rising number of borrowers unable to repay their loans.

Mortgage-backed securities (MBS) played a significant role in the crisis. MBS are financial products created by packaging together loans and leases, in this case, mortgages. Banks and lenders issued mortgages to homebuyers, who then sold these mortgages to larger banks to be packaged into MBS. This process, known as securitization, allowed the banks and lenders to pass on the risk of default to the larger banks.

The number of loans originated between 2000 and 2006 was unusually large due to the real estate bubble in the United States. As a result, MBS became increasingly popular among investors, as they were believed to be low risk and offered higher returns due to the higher interest rates paid by subprime borrowers. However, when US housing prices began to fall, the value of MBS declined, and investors incurred significant losses.

The decline in MBS prices further exacerbated the financial crisis. Investors who had purchased MBS with short-term loans found it difficult to roll over these loans, leading to further selling of MBS and declines in MBS prices. This created a panic in financial markets, with investors pulling their money out of banks and investment funds as they lost confidence in the stability of the financial system.

Understanding APR: The Mortgage Interest Rate Factor

You may want to see also

Frequently asked questions

MBS stands for Mortgage-Backed Securities. They are investments similar to bonds that consist of a bundle of home loans bought from the banks that issued them.

MBS prices are inversely related to interest rates. When interest rates increase, the price of MBS may drop. The two factors with the most impact on interest rates are economic growth and inflation.

MBS pay a fixed interest rate that is usually higher than US government bonds. They also offer monthly payouts, while bonds offer a single lump-sum payout at maturity. MBS are also considered low-risk investments as they are often backed by the federal government.