Mortgages are loans used to buy homes or other types of real estate. The property itself serves as collateral for the loan, and the borrower agrees to repay the lender over a set period, usually in regular monthly payments. The cost of a mortgage depends on several factors, including the type of loan, the term length, and the interest rate charged by the lender. Mortgage rates are influenced by various economic factors and the borrower's financial situation, and they can fluctuate daily or even multiple times a day. Lenders consider factors such as economic conditions, credit score, loan amount, and loan-to-value (LTV) ratio when setting interest rates. Additionally, the down payment, financial situation, and home price can impact the length of the mortgage term.

| Characteristics | Values |

|---|---|

| Type | Fixed-rate, adjustable-rate, conventional, non-conventional, government-backed, conforming, non-conforming, Federal Housing Administration (FHA), Veterans Affairs (VA), U.S. Department of Agriculture (USDA) |

| Term | 10, 15, 20, 30, 40 years |

| Interest Rate | Determined by current market rates, the level of risk a lender assumes with the loan, the borrower's credit score, debt-to-income ratio, loan amount, loan-to-value ratio, economic factors, competition in the local market, and more |

| Down Payment | Minimum 3% for conventional loans, 3.5% for FHA loans, 10% for VA loans, 0% for USDA loans, 20% to avoid private mortgage insurance (PMI) |

| Monthly Payments | Principal, interest, taxes, insurance, homeowners association (HOA) fees, and other expenses |

What You'll Learn

- Mortgage rates are influenced by economic factors and the borrower's financial situation

- A good credit score is key to a lower interest rate

- Lenders set rates based on the return they need to make a profit

- The type of mortgage, its term, and interest rate determine the cost

- The property itself serves as collateral for the loan

![]()

Mortgage rates are influenced by economic factors and the borrower's financial situation

Mortgage rates are influenced by a combination of economic factors and the borrower's financial situation.

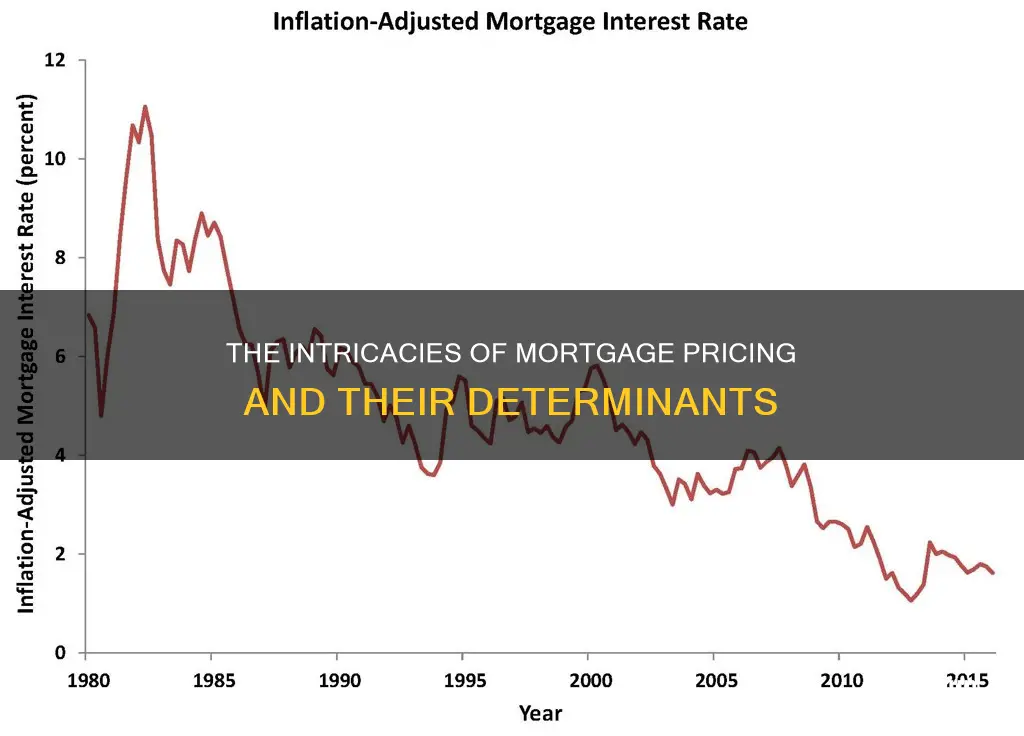

Economic factors that influence mortgage rates include inflation, economic growth, and the Federal Reserve Bank's monetary policy. Inflation, influenced by factors such as global trade tensions, consumer debt levels, and geopolitical events, causes investors to demand higher bond yields, which impacts the rates quoted to mortgage borrowers. The Federal Reserve Bank's monetary policy decisions, such as establishing the Fed Funds rate and adjusting the money supply, also have a significant impact on mortgage rates.

The borrower's financial situation plays a crucial role in determining the mortgage rate they receive. Lenders review the borrower's finances and credit history, including their credit score, income, and assets, and debt-to-income ratio (DTI). A higher credit score indicates a lower risk of default for the lender, potentially resulting in a lower interest rate for the borrower. A lower DTI ratio suggests the borrower has more financial flexibility to make their mortgage payments, which can also lead to a lower interest rate.

Other factors that influence mortgage rates include the type of property, occupancy status, and the availability of homes and consumer demand in the housing market. The type of property, such as a single-family home versus a condo or multi-unit dwelling, can impact the mortgage rate. Additionally, if the home will be the borrower's primary residence, the rate may be lower. The supply and demand dynamics in the housing market also play a role, as a decline in the availability of homes or a shift in consumer preferences can lead to a decrease in mortgage demand and, consequently, a decline in interest rates.

Closing Costs: Who Pays What in a Mortgage?

You may want to see also

![]()

A good credit score is key to a lower interest rate

The credit score range that is considered "good" varies depending on the creditor, but a score of 700 or above is generally considered good or excellent, and will likely result in a lower interest rate. A score below 680 may still qualify you for certain loans, but you are more likely to pay the lowest rates with a score in the 700s. A higher credit score can also qualify you for a larger loan and a lower down payment.

Your credit score is not the only factor that affects your mortgage rate. The type of loan and repayment term, the current market rates, and the home's location can also impact the interest rate you receive. However, your credit score is something that you have control over, and improving your score can help you get a lower interest rate on your mortgage.

Bonds and Mortgage-Backed Securities: What's the Common Link?

You may want to see also

![]()

Lenders set rates based on the return they need to make a profit

Lenders do not set mortgage rates in a vacuum; they are determined by a combination of factors, including economic influences and the borrower's financial situation. When setting rates, lenders consider the return they need to make a profit after accounting for risks and costs.

Lenders review a borrower's finances and credit history, including their credit score, income, assets, and debt, to confirm that they can afford the loan payments and meet the lender's requirements. A higher credit score indicates overall financial health and qualifies the borrower for a lower interest rate. Lenders also consider the loan amount, the loan-to-value (LTV) ratio (the property's value compared to the loan amount), and competition in the local market.

Economic factors, such as current market rates and the level of risk assumed by the lender, play a significant role in determining mortgage rates. For example, fixed-rate mortgages often charge a higher interest rate than adjustable-rate mortgages during the ARM's fixed-rate period because lenders of fixed-rate loans bear the risk of interest rate changes during the loan term. Additionally, government-backed loans like FHA, VA, and USDA loans sometimes have lower rates due to the government guarantee or insurance that reduces the lender's risk.

The cost of origination and the desired margins above these costs also influence the rates set by lenders. Efficient mortgage manufacturers can be more competitive in their pricing. Competition in the local market can drive down margins and interest rates, benefiting borrowers.

Ultimately, lenders consider various factors to determine mortgage rates, and by understanding these factors, borrowers can make informed decisions and aim for the best rates available in the market.

Understanding Mortgage Approval: A Step-by-Step Guide

You may want to see also

![]()

The type of mortgage, its term, and interest rate determine the cost

The type of mortgage, its term, and the interest rate are key factors in determining the overall cost. Mortgages are loans used to buy homes or other types of real estate. The property itself serves as collateral for the loan. There are various types of mortgages, including fixed-rate and adjustable-rate. The type of mortgage chosen will impact the cost. For example, fixed-rate mortgages typically have a higher interest rate than adjustable-rate mortgages during the initial fixed-rate period.

The term of a mortgage refers to the duration over which the loan must be repaid. Common mortgage terms include 10, 15, 30, or even 40 years. Opting for a shorter-term mortgage will result in paying less interest over time but will lead to higher monthly payments. On the other hand, a longer-term mortgage will reduce the amount of each monthly payment but will result in paying more interest overall.

Interest rates on mortgages can vary from lender to lender and can fluctuate daily or even multiple times a day. These interest rates are influenced by various economic factors, such as the 10-year Treasury notes (T-notes) issued by the US government. Lenders also consider the borrower's financial situation, including their credit score, income, assets, debt, and loan amount when setting interest rates. A higher credit score and a lower debt-to-income ratio can lead to a lower interest rate and, consequently, lower monthly payments.

Additionally, the type of mortgage chosen can impact the interest rate. For example, government-backed mortgages like FHA, VA, and USDA loans sometimes offer lower interest rates due to the government guarantee or insurance that reduces the lender's risk. Discount points also play a role, as borrowers can choose to pay a fee upfront to secure a lower interest rate over the life of the loan.

Understanding Mortgage Amortization: What, Why, and How?

You may want to see also

![]()

The property itself serves as collateral for the loan

When taking out a mortgage, the property itself serves as collateral for the loan. This means that the borrower agrees to repay the lender over a set period, typically in regular monthly payments. If the borrower defaults on the loan, the lender can take ownership of the property. Mortgages are often the most significant financial commitment an individual or family will ever make.

The property acts as a guarantee to the lender that the loan will be repaid. This is because, in the event of a default, the lender can seize the property and sell it to recoup their losses. This is known as foreclosure. The lender may become the new owner of the home if the borrower defaults on their mortgage and it is foreclosed.

The value of the property compared to the amount of the loan is known as the loan-to-value (LTV) ratio. This is one of the factors that lenders consider when setting interest rates, along with economic factors, the credit score of the borrower, the loan amount, and competition in the local market. A higher credit score will typically result in a lower interest rate and, therefore, lower monthly mortgage payments.

Lenders must also consider the costs of origination and decide on margins to remain competitive in the market. Fixed-rate mortgages often charge a higher interest rate than adjustable-rate mortgages during the ARM's fixed-rate period because lenders of fixed-rate loans bear the risk of interest rate changes during the loan term.

Factors That Determine Mortgage Amounts

You may want to see also

Frequently asked questions

A mortgage is a loan used to buy or refinance a home or other types of real estate.

Mortgage rates are determined by a combination of factors, including economic influences and the borrower's personal financial situation. The two primary factors that determine mortgage interest rates are current market rates and the level of risk a lender assumes with the loan.

There are several types of mortgages, including fixed-rate and adjustable-rate mortgages, conventional mortgages, conforming loans, non-conforming loans, and government-backed loans.

To get a mortgage, you need to apply to a lender, who will review your finances and credit history to confirm that you can afford the loan payments and meet the lender and loan requirements. You can apply as the only borrower or with a co-borrower.