As of 2025, the average US mortgage debt is $252,505, with a median monthly payment of $2,127. In the fourth quarter of 2023, total mortgage debt in the US rose to $12.25 trillion, accounting for 70% of household debt. This figure has yet to negatively impact the economy, but it has contributed to a rise in delinquency rates. With the average household debt at $105,056, it's no surprise that first-time homebuyers are struggling to get on the property ladder.

| Characteristics | Values |

|---|---|

| Total Mortgage Debt | $12.61 trillion as of March 2025 |

| Number of Mortgages | 85.10 million |

| Average Mortgage Debt per Person | $252,505 as of 2024 |

| Average Mortgage Debt per Mortgage | $148,120 |

| Percentage of Mortgage Debt as Part of Total Consumer Debt | 69.9% |

| Average Interest Rate for 30-year Fixed-rate Mortgage in 2024 | 6.73% |

| Mortgage Debt Increase since end of 2019 | Over $3 trillion |

| Percentage of Mortgage Debt Delinquent by 90 Days or More as of Q4 2024 | 0.70% |

What You'll Learn

![]()

Average US mortgage debt in 2024: $244,498

The average US mortgage debt in 2024 was $244,498, an increase of roughly $8,000 from the previous year. This figure represents the average mortgage balance per borrower and is separate from the total mortgage debt in the US, which stood at $12.25 trillion in the fourth quarter of 2023.

Mortgage debt is the largest component of household debt in the US, comprising up to 70% of total household debt. The average American debt is over $104,000 to $105,056 per household, with total household debt reaching $17.5 trillion to $18 trillion.

The rise in mortgage debt can be attributed to several factors, including increasing home prices, rising interest rates, and a tight housing inventory. Home prices have increased dramatically in recent years, with median home prices rising by nearly 50% over the past five years. This has been exacerbated by rising interest rates, which have made borrowing more expensive. Additionally, the number of homes available for purchase has decreased by a third, further driving up the cost of housing.

While mortgage debt has increased, it is important to note that delinquency and foreclosure rates have remained relatively low compared to historical standards. This is partly due to the large proportion of super-prime borrowers who locked in low mortgage rates. However, there are concerns that rising interest rates and economic headwinds could increase credit risk for financially vulnerable individuals.

Mortgage Business: A Giant Industry Overview

You may want to see also

![]()

Average US mortgage debt in 2025: $252,505

The average US mortgage debt in 2024 was $252,505, according to Experian. This figure represents an increase of roughly $8,000 from the previous year, when the average mortgage debt was $244,498. The median mortgage payment in January 2025 was $2,127, which remained relatively unchanged from the previous year, despite some volatility in the market.

Mortgage debt is a significant contributor to overall consumer debt in the US. As of the fourth quarter of 2024, total consumer debt stood at $18.036 trillion, with mortgage debt comprising 69.9% to 70% of this amount. This equates to an average household debt of $105,056. The rise in household debt, including mortgages, and higher interest rates, can increase credit risk for financially vulnerable individuals.

The increase in average mortgage debt in 2024 can be attributed to various factors. Firstly, median home prices have increased significantly over the past five years, resulting in higher mortgage values. Additionally, borrowing costs, interest rates, and a shortage of available homes have posed challenges for prospective homebuyers.

While the average US mortgage debt figure for 2025 is not yet available, the trend of increasing debt and high home prices is expected to continue. The Federal Reserve's rate cuts for 2024 and 2025 may provide some relief, but it remains to be seen how effectively these will be passed on to mortgage borrowers.

The Giant Movement Mortgage: How Big Is It?

You may want to see also

![]()

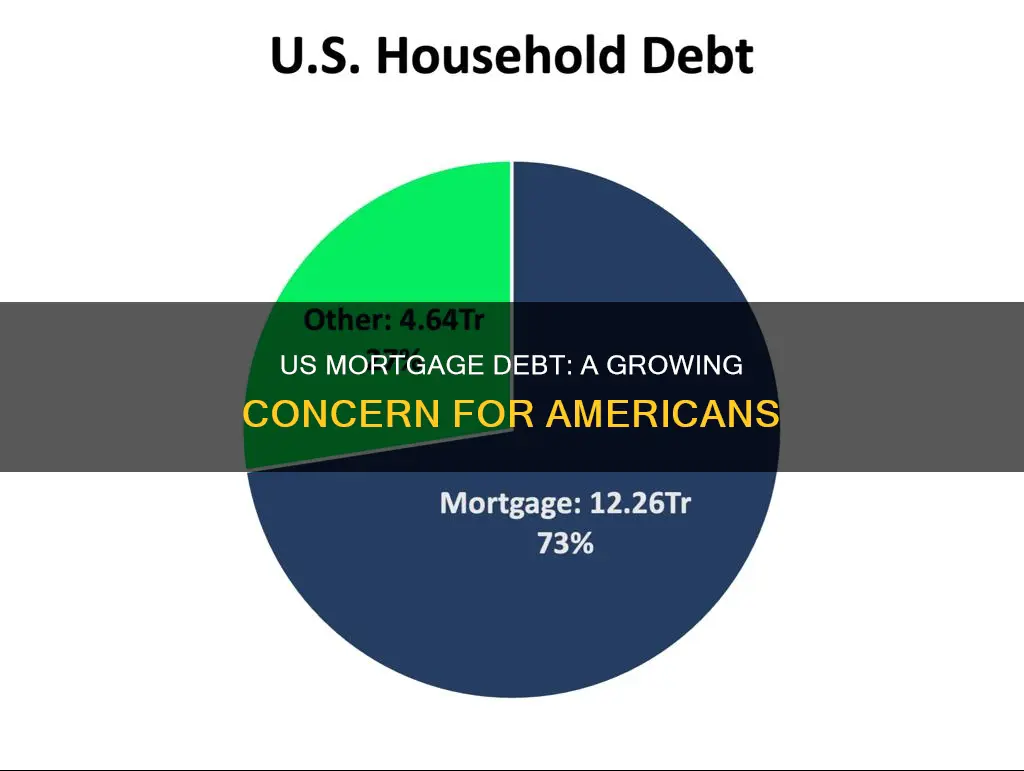

Mortgage debt as a percentage of total US household debt: 70%

Mortgage debt is a significant component of overall household debt in the United States. As of 2025, the average US mortgage debt stands at $252,505, with borrowing costs and interest rates presenting challenges for prospective homebuyers.

In the fourth quarter of 2023, the total mortgage debt in the US reached a staggering $12.25 trillion. This amount represents an increase of $112 billion from the previous quarter. While this massive debt has not yet negatively impacted the economy, it is essential to consider the implications for financially vulnerable individuals. According to the International Monetary Fund (IMF), rising household debt and higher interest rates can increase credit risk for those who are already financially vulnerable. As a result, delinquency rates have been on the rise, indicating that some borrowers are struggling to service their debts.

The high mortgage debt in the US can be attributed to various factors. One significant factor is the increase in median home prices, which have risen by nearly 50% in the past five years. Additionally, 30-year mortgage rates have almost doubled, making it even more challenging for first-time homebuyers to enter the market. The availability of homes for purchase has also decreased by a third, further compounding the issue. These factors have contributed to the substantial mortgage debt that American households are facing today.

It is worth noting that mortgage debt comprises a significant portion of total household debt in the US. As of 2025, American households carry a total debt of approximately $18 trillion, with mortgage debt accounting for 70% of that amount. This means that the average household debt is $105,056, a significant burden for many families. While credit card debt and auto loan debt also contribute to overall household debt, mortgage debt remains the most substantial component.

Ruoff Mortgage Venue: Size, Capacity, and More

You may want to see also

![]()

Mortgage debt as a percentage of total US debt in Q4 2023: 69.9%

Mortgage debt is a significant component of overall US debt, and this was particularly evident in the fourth quarter of 2023. During this period, mortgage debt in the US reached $12.25 trillion, a substantial increase of $112 billion from the previous quarter. This amount represents 69.9% of the total US household debt, which stood at $17.5 trillion at the time.

The rise in mortgage debt in Q4 2023 was influenced by several factors. One key contributor was the increase in median home prices, which had surged by nearly 50% over the previous five years. This trend, coupled with the rise in 30-year mortgage rates, presented challenges for prospective homebuyers. The borrowing costs for mortgage debt remained relatively stable during this period, with rates fluctuating between 6% and slightly above 7%.

While the Federal Reserve's rate cuts for 2024 and 2025 are expected to lead to a decrease in mortgage rates, the impact on the overall economy remains to be seen. The high level of mortgage debt, combined with rising interest rates, could pose financial risks for vulnerable individuals. According to the International Monetary Fund (IMF), these factors may increase credit risk and potentially lead to higher credit defaults.

The distribution of mortgage debt across different age groups is worth noting. Younger homeowners tend to have larger mortgage balances compared to older mortgage borrowers. This trend contributes to the overall mortgage debt landscape and has implications for the financial stability of younger Americans.

In conclusion, the fourth quarter of 2023 witnessed a significant proportion of mortgage debt as part of total US debt, reaching nearly 70%. This situation has implications for both the economy and individual financial wellbeing, especially with the ongoing changes in interest rates and the impact of the COVID-19 pandemic on public debt.

Freedom Mortgage: A Giant in the Industry

You may want to see also

![]()

The impact of rising mortgage debt on the economy

As of Q4 2023, mortgage debt in the US reached $12.25 trillion, with the average mortgage debt per household being $105,056. This figure has yet to show signs of hurting the economy, but it is worth noting that it constitutes approximately 70% of total household debt, which stands at $17.5 trillion.

Rising mortgage debt can have a significant impact on the economy. Firstly, it can increase credit risk for financially vulnerable individuals, as higher interest rates make it more challenging for consumers to service their debt. This can lead to increased credit defaults, particularly for those in precarious financial situations. Secondly, rising mortgage debt is often accompanied by higher home prices, which can result in a market squeeze as fewer people can afford to purchase homes. This can further drive up prices for those who already own homes, potentially leading to a housing market bubble.

On the other hand, rising mortgage debt can also indicate a strong economy, as it may be a result of higher home prices and increased demand for housing. Additionally, the availability of mortgage credit can stimulate the housing market and contribute to economic growth. However, it is essential to consider the impact of interest rates on mortgage borrowers. When the Federal Reserve raises interest rates to combat inflation, mortgage rates tend to increase as well, making borrowing more expensive for consumers. This can lead to increased delinquency rates, especially for those with adjustable-rate mortgages.

Gateway Mortgage: A Giant in the Industry

You may want to see also

Frequently asked questions

US mortgage debt stood at $12.25 trillion in Q4 2023.

The average US mortgage debt was $252,505 in 2024.

The median mortgage payment in the US was $2,127 in January 2025.

Mortgage debt comprises 70% of American household debt.

US mortgage debt is higher than credit card debt and auto loan debt.