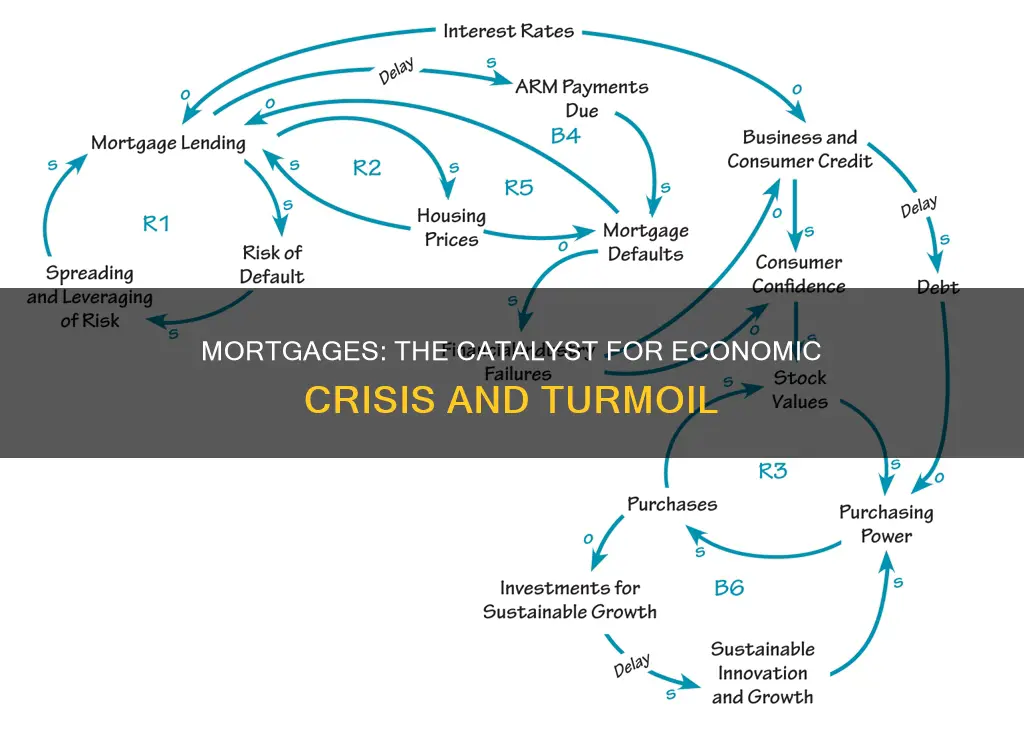

The financial crisis of 2008 was a result of many factors, but one of the key causes was the rise in subprime lending and housing speculation. This was encouraged by governments wanting to help lower-income groups access the housing market, which led to risky financial practices and an increase in loan incentives. As a result, borrowers assumed risky mortgages, and as housing prices declined, investors defaulted on their loans. This triggered a wave of bankruptcies and a loss of investor confidence, which froze credit markets and led to widespread economic distress.

| Characteristics | Values |

|---|---|

| Date | 2008 |

| Immediate cause | Bursting of the US housing bubble |

| Other causes | Subprime lending, increase in housing speculation, risky financial practices, loose monetary policy, increase in loan incentives, rising housing prices |

| Impact | Deep recession, job losses, decline in overall economic activity, increase in unemployment, financial distress, contraction in GDP |

| Response | Interest rate cuts, large-scale asset purchases, bailout measures |

What You'll Learn

![]()

Subprime lending and housing speculation

The economic crisis of the late 2000s had many causes, with commentators assigning varying levels of blame to financial institutions, regulators, credit agencies, government housing policies, and consumers, among others. Two proximate causes were the rise in subprime lending and the increase in housing speculation.

Subprime lending refers to the extension of loans to borrowers with "prime", or low-risk, credit ratings who may default when prices fall. In the years before the crisis, lending standards deteriorated, especially between 2004 and 2007, with lenders offering more and more loans to higher-risk borrowers. This was partly driven by government policies aimed at expanding homeownership, even for those who could not afford it, and the predatory lending practices of mortgage lenders, who offered products such as adjustable-rate mortgages and 2–28 loans. These higher-risk mortgage products contributed to US households becoming increasingly indebted.

The rise in subprime lending was also linked to the growth of mortgage-backed securities (MBS), which derive their value from mortgage payments and housing prices. The increased availability of MBS attracted global investors, who borrowed and invested heavily in the US housing market. As housing prices declined, these investors reported significant losses, which contributed to the broader economic crisis.

Housing speculation further exacerbated the crisis. As housing prices rose, investors with prime-quality mortgages took on high levels of mortgage debt to invest in additional properties. When housing prices fell, many of these investors defaulted and entered foreclosure on their investment properties. This dynamic contributed to a broader trend of rising defaults and losses on various loan types, as the crisis expanded from the housing market to other sectors of the economy.

While the causes of the economic crisis were multifaceted, the interplay between subprime lending and housing speculation played a significant role in driving the severe and long-lasting economic fallout experienced in the US and Europe.

Avoiding Mortgage Crisis: Strategies for Stability and Security

You may want to see also

![]()

Housing policy and the economy

The economic crisis of 2007-2009, also known as the Global Financial Crisis, was triggered by a combination of factors related to housing policies and practices. One significant factor was the expansion of the housing market, particularly in the United States, which experienced a property bubble that eventually burst. This expansion began in the 1990s and continued through the 2001 recession, with home prices more than doubling between 1998 and 2006. The rise in housing prices was fuelled by an increase in mortgage borrowing, with financial institutions offering loans to subprime borrowers and engaging in risky lending practices. These practices included the proliferation of mortgage-backed securities (MBS), where the value of financial instruments was derived from mortgage payments and housing prices. As a result, when housing prices declined, major global financial institutions that had heavily invested in MBS reported significant losses.

The role of governments and their housing policies in encouraging homeownership among low-income households has also been scrutinized. Governments in countries like the United States, Ireland, Spain, and the United Kingdom implemented policies that promoted homeownership among lower-income groups. While these policies had the noble intention of increasing access to the housing market for disadvantaged populations, they also contributed to the fragility of the financial system. The combination of deregulation, loose monetary policies, and pressure on regulators to maintain light oversight created an environment conducive to risky lending practices and excessive exposure to the housing market.

As the crisis unfolded, homeowners began to default on their mortgages at alarming rates. Many found themselves "upside down," owing more on their mortgages than their homes were worth. This led to a wave of foreclosures and bankruptcies, further exacerbating the crisis. The decline in housing prices also affected investors, who were more likely to default on their loans than non-investors. The crisis quickly spread beyond the housing market, impacting other sectors of the economy and leading to a broader economic downturn.

The impact of the crisis was severe and far-reaching. The United States entered a deep recession, with nearly 9 million jobs lost between 2008 and 2009, and the unemployment rate doubling from 5% to 10%. The recession lasted eighteen months, making it the longest since World War II. The effects of the crisis were not limited to the US, as Europe also struggled with elevated unemployment and severe banking impairments, with bailout funds totalling billions of dollars required to stabilize the economy.

Gateway Mortgage: A Giant in the Industry

You may want to see also

![]()

Credit markets and investor confidence

The global financial crisis (GFC) refers to the period of extreme stress in global financial markets and banking systems between mid-2007 and early 2009. The crisis was caused by a combination of factors, including the failure or near failure of financial firms, lax regulation of subprime lending, and falling US house prices, which led to a wave of mortgage losses. This triggered a panic in financial markets, with investors withdrawing their money from banks and investment funds worldwide due to uncertainty about the stability of these institutions.

The crisis had a significant impact on credit markets, with a rapid expansion of credit preceding the financial crash. Frothy credit markets occur when people become less concerned about the potential downsides of lending and borrowing. This was evident in the lead-up to the GFC, as individuals and institutions were willing to lend and borrow large amounts, assuming that asset prices would continue to rise. As a result, many central banks and governments failed to recognize the extent of bad loans and the spread of mortgage losses through the financial system.

The post-crisis period has seen a tightening of credit markets, driven by the Fed's tightening cycle. While this has contributed to financial stability, it is important for policymakers to monitor the credit markets closely. Rapid credit expansion has preceded many financial crises, and sudden collapses in credit can be highly detrimental to the economy. Therefore, keeping a watchful eye on credit markets is essential for preventing future crises.

The GFC also had a significant impact on investor confidence, with investors losing trust in the financial system. As a result, they may have withdrawn their funds, sold their assets, or demanded higher returns to compensate for the increased risk. This dynamic contributed to a vicious cycle of instability and uncertainty, making it challenging for financial institutions to obtain new financing. Central banks responded by lowering interest rates to stimulate economic activity, but the recovery from the crisis was slow.

To restore investor confidence, policymakers, regulators, and financial institutions must prioritize economic recovery and foster stability. This includes implementing measures such as fiscal stimulus packages, monetary easing, and investment in infrastructure. Clear and consistent messaging about the government's commitment to economic stability can help reassure investors. Additionally, demonstrating a commitment to social responsibility and inclusive practices can enhance the reputation of financial institutions and attract investor confidence in the aftermath of a financial crisis.

Mortgage Theft: A Common Crime You Need To Know

You may want to see also

![]()

Financial institutions and lending practices

The economic crisis of 2007–2008 was triggered by a combination of factors, with financial institutions and their lending practices playing a significant role. The crisis was characterised by a "run" on the shadow banking system, which included institutions like investment banks and hedge funds. These entities had become crucial in providing credit to the US economy, yet they operated outside the regulatory framework governing traditional commercial banks.

The shadow banking system's interconnectedness with larger financial institutions, such as Wall Street firms and insurance companies, meant that the crisis spread widely. These larger institutions had also assumed significant debt burdens by providing loans and did not possess adequate financial buffers to withstand substantial loan defaults. As housing prices declined, institutions that had heavily invested in mortgage-backed securities (MBS) reported significant losses, impacting their ability to lend and slowing economic activity.

Mortgage-backed securities, along with collateralised debt obligations (CDOs), were innovative financial instruments that played a pivotal role in the crisis. These instruments derived their value from mortgage payments and housing prices. Initially, they offered higher interest rates and were considered low risk due to their attractive risk ratings from credit rating agencies. However, most of these financial instruments were backed by high-risk subprime mortgages. As delinquencies and defaults increased due to declining housing prices, the risks inherent in these securities were exposed, leading to substantial losses for investors.

The rise in subprime lending and the increase in housing speculation were key factors in the crisis. Financial institutions relaxed lending standards, offering riskier mortgage products that contributed to US households becoming increasingly indebted. Even investors with "prime" credit ratings were more likely to default than non-investors when housing prices fell. This trend of lowered lending standards and higher-risk mortgage products was not adequately recognised or addressed by policymakers and regulators, who placed excessive confidence in the stability of the financial system.

The complex nature of these financial instruments and the interconnectedness of institutions in the shadow banking system made reorganisation through bankruptcy challenging. As a result, government bailouts became necessary to prevent further economic deterioration. The crisis highlighted the cyclical nature of risk-taking in the financial industry and the potential for self-deception and overconfidence in risk management strategies among financial executives and regulators.

What Are the Chances of Assuming a Mortgage?

You may want to see also

![]()

Global economic impact

The global financial crisis of 2007–2009 had far-reaching consequences and impacted the world economy in several significant ways.

One of the most prominent effects was the severe and prolonged economic downturn, often referred to as the Great Recession. The recession officially began in December 2007 and ended in June 2009, but economic weakness and slow growth persisted for years afterward. The United States, in particular, experienced a deep recession, with nearly 9 million jobs lost between 2008 and 2009, and the unemployment rate more than doubled, reaching 10%. The US gross domestic product fell by 4.3%, making it the deepest recession since World War II. The impact was also felt in Europe, with elevated unemployment and severe banking impairments estimated at €940 billion between 2008 and 2012.

The crisis also led to a wave of government bailouts and interventions to stabilize the financial system. In the US, the government invested, loaned, or granted a total of $626 billion through various bailout measures, and ultimately made a profit of $109 billion as of January 2021 due to interest earned on bailout loans. Central banks and governments around the world implemented stimulus measures and cut interest rates to unprecedented levels to support their economies and encourage lending.

The crisis exposed the fragility of the global financial system and the interconnectedness of financial institutions. The collapse of major financial institutions, such as Lehman Brothers, triggered panic and eroded investor confidence worldwide, leading to a freeze in credit markets and widespread economic distress. The crisis highlighted the risks associated with complex financial products, such as mortgage-backed securities (MBS), and the exposure of financial institutions to these products. The total losses from the crisis were estimated in the trillions of US dollars globally.

The global financial crisis also had long-lasting impacts on regulatory policies and approaches to financial sector oversight. There was a recognition of the need to strengthen financial regulations and enhance the independence of central banks and regulators from political interference. Efforts were made to address the "too big to fail" issue and to improve risk management practices within financial institutions. The crisis also prompted a reevaluation of housing policies and the role they played in contributing to the crisis, particularly the encouragement of homeownership among low-income households and the proliferation of risky subprime mortgages.

United Wholesale Mortgage: A Giant in the Industry

You may want to see also

Frequently asked questions

The economic crisis, also known as the Subprime Mortgage Crisis, was caused by the bursting of the United States housing bubble, which peaked in 2006. This was the largest property bubble in human history.

Banks were issuing mortgages to subprime borrowers, leading to a wave of lending practices that contributed to inflating the housing bubble. As housing prices declined, investors defaulted on their mortgages, and financial institutions that had invested heavily in mortgage-backed securities (MBS) reported significant losses.

The crisis had severe and long-lasting consequences, with nearly 9 million jobs lost in the US during 2008 and 2009. The unemployment rate more than doubled, and the US entered a deep recession. The crisis also spread beyond the housing market, with losses in the trillions of US dollars globally.