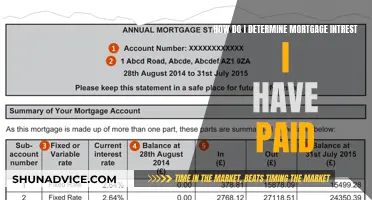

When taking out a mortgage, it's important to understand the annual percentage rate (APR) as it reflects the true cost of borrowing money. This is because, in addition to the interest rate, the APR includes other fees and charges that you'll need to pay to get the loan. These fees can include origination fees, closing costs, and mortgage broker fees. Lenders are required to display APRs, making it easier to compare lending costs between competitors. You can calculate the APR on your own using a formula or an online calculator.

| Characteristics | Values |

|---|---|

| What is APR? | Annual Percentage Rate (APR) is a tool for comparing mortgage offers with different combinations of interest rates, discount points and fees. |

| How is it calculated? | APR = [({Fees + Total Interest} / Loan Principal) / Total Days in Loan Term] x 365 x 100 |

| What does it include? | The APR includes the interest rate, points, mortgage broker fees, origination fees, and other charges that you pay to get the loan. |

| How is it different from the interest rate? | The interest rate is different from the APR. The interest rate is the cost you will pay each year to borrow the money, expressed as a percentage rate. It does not reflect fees or any other charges you may have to pay for the loan. The APR is usually higher than the interest rate. |

| How to find out the APR for your mortgage? | Lenders are required to display APRs. You can use online calculators to determine the APR by entering the interest rate, discount points, loan amount, term, and fees. |

| How to get the best APR? | To get the best APR, apply for a mortgage early on in the home-buying process. Government-backed loans like FHA, USDA, and VA loans often come with more favorable APRs compared to conventional loans. |

What You'll Learn

![]()

Calculating APR

APR, or annual percentage rate, is a useful tool for comparing the costs of different mortgages. It is a measure of the total cost of borrowing, including interest and fees, expressed as a yearly percentage. The APR on a mortgage is different from the interest rate, as the latter does not include any fees.

Lenders will provide the APR information to you, but you can also calculate it on your own. To calculate the APR on a mortgage using a formula, you need to know the loan amount, the interest rate, the number of payments per year, the total number of payments, and any fees and charges added to the loan.

The formula for APR is:

APR = (Total Interest + Fees) / (Loan Amount x Number of Years) x 100

For example, if you borrow $200,000 at a 4% interest rate for 30 years with monthly payments and pay $5,000 in fees and charges, then the total interest you will pay over the life of the loan is $143,739.01. This would result in an APR of:

APR = ($143,739.01 + $5,000) / ($200,000 x 30) x 100 = 2.47%

You can also use an online calculator to find the APR on a mortgage by entering the loan amount, term, interest rate, fees, and discount points.

Understanding Your Mortgage Payoff: Strategies for Homeowners

You may want to see also

![]()

APR vs interest rate

When taking out a mortgage, it is important to understand the difference between the interest rate and the APR (Annual Percentage Rate). The interest rate is the cost you pay to the lender for borrowing money, while the APR includes the interest rate as well as any additional fees and charges. Both are expressed as percentages, but the APR will always be higher than the interest rate as it includes other costs associated with the loan.

The interest rate is the annual cost of a loan to a borrower, expressed as a percentage. It is the cost of borrowing money from a lender and is influenced by the federal funds rate set by the Federal Reserve. For example, during an economic recession, the Federal Reserve may lower interest rates to encourage consumers to spend money. The higher the interest rate, the more you will pay over the life of the loan.

The APR, on the other hand, is a more comprehensive measure of the cost of a loan. It includes the interest rate plus any additional fees and charges, such as origination fees, closing costs, mortgage insurance, and discount points. The APR is intended to give borrowers a more accurate picture of the total cost of the loan. It is a useful tool for comparing different loan offers as it standardises the various fees and charges that may be included. The APR should be provided by the lender in a Loan Estimate document.

It is important to note that your monthly mortgage payments are based on the interest rate, not the APR. However, the APR can help you understand the total cost of the loan over its entire term. It is also worth mentioning that government-backed loans, such as FHA, USDA, and VA loans, often come with more favourable APRs compared to conventional loans.

To calculate the APR for a mortgage, you can use the following formula: APR = [({Fees + Total Interest} / Loan Principal) / Total Days in Loan Term] x 365 x 100. Alternatively, you can use an online APR calculator by entering the loan amount, term, fees, and discount points to determine the APR.

Switching Your Chase Mortgage to Semi-Monthly Payments

You may want to see also

![]()

Fixed vs variable APR

When taking out a loan or mortgage, the lender will determine the annual percentage rate (APR) you'll pay. You may be offered a fixed or variable rate, or you may be able to choose between the two. Understanding the differences between the two can help you save money and meet your financial goals.

A fixed APR is determined at the time of loan approval and typically does not change over the life of the loan. All federal student loans and fixed-rate mortgages have fixed APRs, as do many auto loans and personal loans. A fixed APR is more certain, as you will always know exactly what your monthly payment will be, regardless of market rate changes. However, fixed-rate loans have historically been more expensive over their lifetime than variable-rate loans.

A variable APR, on the other hand, changes with indexed interest rates, such as the prime rate. If interest rates increase, so will your APR. Variable APRs may start out lower than fixed-rate loans, but can end up higher over time depending on market rates. Variable APRs are beneficial in a declining interest rate market because loan payments will decrease as well. However, when interest rates rise, borrowers who hold a variable-rate loan will find that the amount due on their loan payments also increases.

A popular type of variable-rate loan is a 5/1 adjustable-rate mortgage (ARM), which maintains a fixed interest rate for the first five years of the loan and then adjusts the interest rate annually. A split-rate loan allows borrowers to split their loan amount between fixed and variable interest rate components.

To calculate the APR on a mortgage, you can use an online calculator. You will need to enter the loan amount, term, fees, and discount points. APR is a useful tool for comparing mortgage offers with different combinations of interest rates, fees, and discount points.

Becoming a Mortgage Originator in Florida: A Guide

You may want to see also

![]()

How APR impacts monthly payments

When it comes to taking out a mortgage, the APR, or Annual Percentage Rate, is a key factor in understanding how much your loan will cost you each year. It includes not only the interest rate on the loan but also any fees charged by the lender and other providers, giving you a more accurate view of the total cost of borrowing. This is why it is a more effective tool than just the interest rate for comparing mortgage offers.

The APR is calculated by adding up all the fees and interest and dividing this by the loan principal, then dividing this figure by the total days in the loan term, multiplying by 365, and then multiplying by 100.

The APR can be a useful tool for comparing mortgage offers with different combinations of interest rates, fees, and discount points. However, it does have limitations. The APR calculation assumes the borrower will keep the loan for its entire term, which is often not the case. Many people sell their homes or refinance their mortgages before the loan is paid off. Therefore, it is important to also consider the loan's APY (Annual Percentage Yield), which takes into account the compounding of interest over time. This will give you a more accurate picture of the total cost of the loan.

Additionally, the APR may not always reflect the true cost of a loan, as lenders have some flexibility in how they calculate it, including which fees and charges to include or exclude. For example, if you plan to pay off your loan faster or have a shorter repayment period, the costs and fees may be spread too thin with APR calculations, and the actual cost of borrowing may be higher than the APR suggests.

When deciding between minimising interest rates or APR, it is important to consider your long-term plans. If you are not planning on staying in your home long-term, a lower interest rate may be more advantageous due to the breakeven point for fees. However, if you plan to stay in your home for the long term, a lower APR may be preferable as it often translates to a lower total loan cost.

Commercial Mortgage Application: A Step-by-Step Guide

You may want to see also

![]()

Comparing APRs

When comparing mortgage APRs, it's important to understand that the APRs include both the interest rate and any fees charged by your lender and other providers, such as closing costs, mortgage insurance, and loan origination fees. This makes it a valuable tool for comparing the total cost of different mortgage offers.

To effectively compare mortgage APRs, you should consider the following:

- Interest Rate and Fees: Calculate the total interest and fees you would pay over the life of the loan. This will give you an understanding of the overall cost of the mortgage, not just the upfront costs.

- Loan Term: Compare loans with similar terms. The APR assumes that you will keep the loan for its entire term, so comparing loans with the same duration (e.g., 15-year or 30-year fixed-rate mortgages) will provide a more accurate comparison.

- Discount Points and Rebates: Consider the impact of discount points and rebates. Discount points are fees you pay to the lender to lower your interest rate, while rebates are refunds on these fees. These can affect the overall cost of the loan and, therefore, the APR.

- Adjustable-Rate Mortgages (ARMs): Be cautious when comparing APRs for adjustable-rate mortgages. The APR may not accurately capture the true costs of an ARM since future interest rate changes are unpredictable.

- Federal Truth in Lending Act: Ensure that lenders comply with this Act, which requires the disclosure of APR in consumer loan agreements. This ensures that the APRs you are comparing are calculated consistently and accurately.

Additionally, you can use online mortgage APR calculators to input loan amounts, terms, fees, and discount points to determine the APR for each option and facilitate your comparison.

Disputing Mortgage Debt: Know Your Rights and Take Action

You may want to see also

Frequently asked questions

APR stands for Annual Percentage Rate. It is a calculation that reflects the mortgage interest rate plus other charges.

You can calculate your mortgage APR by using an online calculator. You will need to enter your interest rate, discount points, and other fees to determine the APR.

A fixed APR offers a steady rate for the duration of the loan. A variable APR includes rates that may change over time.

APR is a useful tool for comparing mortgage offers with different combinations of interest rates, discount points, and fees. It provides a more accurate view of how much your mortgage will cost than the interest rate alone.

To get the best APR for your mortgage, it is important to apply for a mortgage early on in the home-buying process. Government-backed loans like FHA, USDA, and VA loans often come with more favorable APRs compared to conventional loans.