If you're looking to buy a home, it's important to understand how mortgages work. Amortization is the process of paying off a loan over time in predetermined installments. With mortgage amortization, your monthly payments gradually pay off the loan's principal and interest. When you first start paying off your mortgage, most of your payment is allocated toward interest. However, over time, more of your payment each month goes toward the principal, which continues until the loan is completely paid off. You can use an amortization calculator to determine how much interest you will pay over the loan's entire term and to create an amortization schedule, which is a monthly breakdown of how much of each payment goes toward principal and interest. Understanding amortization will help you make better financial decisions and be a more conscious shopper when considering mortgages.

Re-amortizing your mortgage

| Characteristics | Values |

|---|---|

| Definition | Amortization is the process of paying off a debt or loan over time in predetermined installments. |

| Purpose | To gradually pay off the loan's principal and interest. |

| Benefits | Allows borrowers to have a fixed payment over a given time period. |

| Factors | Interest rate, type of loan, loan amount, loan term, and loan start date. |

| Calculation | Utilize an amortization calculator to determine total interest, remaining loan balance, and monthly payment distribution. |

| Schedule | An amortization schedule outlines the monthly breakdown of payments toward principal and interest. |

| Early repayment | Reducing the loan balance with early payments can lower total interest costs and shorten the loan term. |

| Tax implications | Certain types of interest, such as home mortgage interest, may be tax-deductible, making it essential to differentiate principal from interest contributions. |

| Fixed-rate vs. adjustable-rate | Fixed-rate mortgages maintain consistent monthly payments, while adjustable-rate mortgages (ARMs) fluctuate based on rate adjustments. |

What You'll Learn

![]()

Understanding amortization schedules

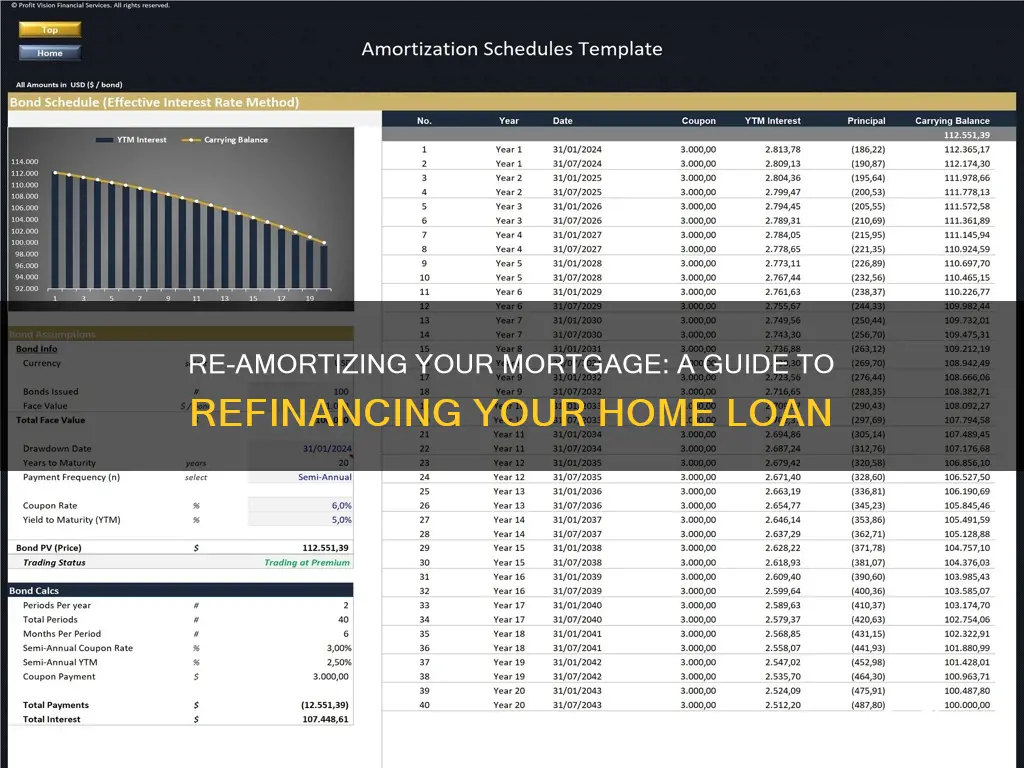

Amortization is the process of paying off a debt or loan over time in predetermined, regular installments. An amortization schedule is a table that shows how much of each payment is dedicated to paying off the interest and the principal balance of the loan. The principal balance is the amount you borrowed, while the interest is the cost of taking out the loan.

An amortization schedule is often referred to as an amortization table. It shows a breakdown of your monthly mortgage payments over time. It outlines how much of each payment is allocated to interest and how much is allocated to paying off the loan's principal balance. When you first start paying off your mortgage, most of your payment is dedicated to interest. However, as you make payments over several years, the allocation shifts, and a larger portion of each payment is applied to the principal balance.

The amortization schedule for a fixed-rate mortgage will show that you are repaying the loan in equal installments. Initially, a larger portion of each payment is dedicated to interest, but over time, you will pay less interest and more towards the principal balance with each payment until the loan is paid off.

It is important to review your mortgage amortization schedule to understand how much you will be paying each month. By analyzing how much money from each of your payments goes towards interest, you may be motivated to pay extra each month to reduce the principal balance. An amortization schedule can also help you understand how reducing the loan balance with early payments can lower your total interest costs and shorten the loan term.

Putting Your Mortgage on Hold: What You Need to Know

You may want to see also

![]()

Fixed-rate vs. adjustable-rate mortgages

Fixed-rate and adjustable-rate mortgages (ARMs) are the two types of mortgages that differ in their interest rate structures. With a fixed-rate mortgage, the interest rate is set at the beginning of the loan and remains the same throughout its term. This means that your monthly payments will also stay the same, making budgeting easier. Fixed-rate mortgages are simpler and offer more predictability for the borrower, protecting them from sudden increases in monthly payments if interest rates rise. However, if interest rates drop a few years into your mortgage, you may not benefit from this change.

On the other hand, with an adjustable-rate mortgage (ARM), the interest rate may fluctuate. ARMs typically start with a lower interest rate and monthly payments than fixed-rate loans, but these can increase or decrease over time based on broader market trends and broader interest rate indices. The initial rate period for an ARM can vary, lasting for months or a few years, after which the rate is adjusted at regular intervals until the end of the loan term. It is important to understand the adjustment frequency and indexes before choosing an ARM.

The decision between a fixed-rate and an adjustable-rate mortgage depends on various factors. Consider your financial situation, the length of time you plan to own the home, and the current interest rate environment. If you prefer stability and predictability in your monthly payments, a fixed-rate mortgage may be more suitable. However, if you are comfortable with potential fluctuations in interest rates and payments, an ARM could offer you the benefit of initially lower interest rates.

Additionally, it is worth noting that mortgage amortization refers to the process of paying off your mortgage debt over time through regular monthly payments. These payments are allocated towards both the loan's principal balance and the interest. In the early stages of your loan, most of your payment goes towards interest, but over time, a larger portion is applied to the principal. An amortization schedule outlines how your payments are distributed and can help you understand how to reduce your loan balance and total interest costs.

Mortgage and Deed: Adding EIN, What You Need to Know

You may want to see also

![]()

How to calculate amortization

Amortization is the process of paying off a debt or loan over time in predetermined, fixed, and equal installments. For mortgages, this means that a portion of your monthly payment goes towards the principal (the amount you borrowed), and another portion goes to interest. Over time, you pay less towards interest and more towards the principal with each payment until the loan is paid off.

To calculate amortization, you will need to know the principal loan amount, the monthly payment amount, the loan term, and the interest rate on the loan. You can then use the following formula to calculate the monthly interest payment, principal payment, and outstanding loan balance:

- Convert the annual interest rate to a monthly rate by dividing it by 12.

- Multiply the loan amount by the monthly rate to get the interest payment.

- Subtract the monthly mortgage payment from the interest to determine the principal payment.

- Subtract the principal from the loan amount to get the outstanding loan balance.

You can also use an amortization calculator, which will do the math for you. These calculators take into account your loan amount, loan term, interest rate, and loan start date to estimate the total principal and interest paid over the life of the loan.

It is important to review your mortgage amortization schedule to understand how much you will pay each month and how much money from each of your payments goes towards interest. This can help you make informed decisions about your loan and inspire you to pay extra each month to drive down the principal balance.

Mortgage Freedom: Marking Your Loan as Paid Off

You may want to see also

![]()

Paying off the principal

There are several ways to pay off your mortgage principal earlier. One way is to make additional principal payments on your loan without reamortizing or recasting your mortgage. This will put you ahead of schedule and reduce the number of mortgage payments until your mortgage is paid off. Your monthly payment will remain the same, but you will pay off your debt sooner.

Another way to pay off your mortgage principal earlier is to reamortize or recast your mortgage. This involves making a large lump-sum payment to your lender, typically a minimum of $10,000, which goes towards your loan's principal balance and reduces the amount you owe. Your lender will then reamortize your balance, adjusting the amortization schedule. This option is best for homeowners who want to keep their current interest rate and have the cash to make a substantial lump-sum payment.

You can also pay off your mortgage principal earlier by making extra payments each month or by sending any unexpected windfalls, such as holiday bonuses, tax returns, or credit card rewards, to your mortgage company. Making an extra mortgage payment each year could significantly reduce the term of your loan.

Before making any extra payments towards your mortgage principal, it is important to review your closing disclosure to verify that there are no prepayment penalties tied to your loan. Most borrowers are not subject to a prepayment penalty, but it is important to check to avoid any unexpected fees.

Putting Your Mortgage Deed in a Trust: What You Need to Know

You may want to see also

![]()

Tax implications

Re-amortizing a mortgage loan involves the borrower paying a lump sum to reduce the loan balance. The mortgage lender then re-amortizes the loan, creating an updated payment schedule based on the lower loan balance. This process is also known as a loan recast and maintains the original interest rate and term length of the loan.

The tax implications of re-amortizing a mortgage are important to consider. Some types of interest, including home mortgage interest, may be tax-deductible. By partitioning principal from interest contributions, you can determine the total amount of interest paid over the life of the mortgage. This information can be used to potentially reduce your taxable income.

Additionally, early repayment of a loan can result in prepayment penalties, which could impact your tax liability. It is important to review the terms of your loan agreement to understand any potential penalties for early repayment.

When considering re-amortization, it is advisable to consult with a tax professional or financial advisor. They can provide personalized guidance based on your specific circumstances and help you navigate the tax implications of re-amortizing your mortgage.

Furthermore, it is worth noting that the eligibility requirements for re-amortization may vary. For instance, you typically cannot recast a government-backed loan, such as an FHA, VA, or USDA loan. Lenders may also have their own specific criteria, such as minimum principal reduction requirements or equity thresholds, that must be met to qualify for re-amortization.

Exploring Options: Strategies to Temporarily Pause Mortgage Payments

You may want to see also

Frequently asked questions

Amortization is the process of paying off a debt or loan over time in predetermined installments. With mortgage amortization, a portion of your monthly payment goes toward the principal, or the amount you borrowed, and another portion goes to interest.

You can calculate amortization by using an amortization calculator. You can input variables such as the loan amount, loan term, interest rate, and loan start date to see how your payments will change over the length of the loan.

A mortgage amortization schedule is a breakdown of your monthly mortgage payment over time. It shows how much of each payment goes toward the loan principal and how much goes toward interest.