When it comes to rentals and mortgages, the biggest difference is who owns the property. With a mortgage, you take out a loan from a bank to purchase your own home, which you then pay back with interest over a long period, typically 15 to 30 years. On the other hand, renting involves paying the owner of the property on a monthly basis, with rental agreements usually lasting 12 months. While renting provides flexibility and freedom, mortgages offer an opportunity to build long-term equity as your home appreciates in value. This equity can be leveraged for home equity loans or lines of credit to finance large expenditures.

| Characteristics | Values |

|---|---|

| Ownership | Rental agreements mean you don't own the property, whereas a mortgage is a loan to help you purchase the property. |

| Duration | Rental agreements are shorter, usually lasting 12 months with the option to renew. Mortgage payments typically last 15-30 years. |

| Monthly payments | Monthly mortgage payments are often cheaper than monthly rental payments for a similarly-sized property. |

| Additional costs | Owning a home comes with additional costs and commitments that rental properties do not. |

| Equity | Renting does not allow you to build long-term equity. A mortgage generates equity over time, especially if the home appreciates in value. |

| Rent-to-own | Rent-to-own agreements act as a middle ground between a standard lease and a mortgage, allowing you to save for a down payment. These are more expensive and more of a commitment than traditional rentals. |

What You'll Learn

![]()

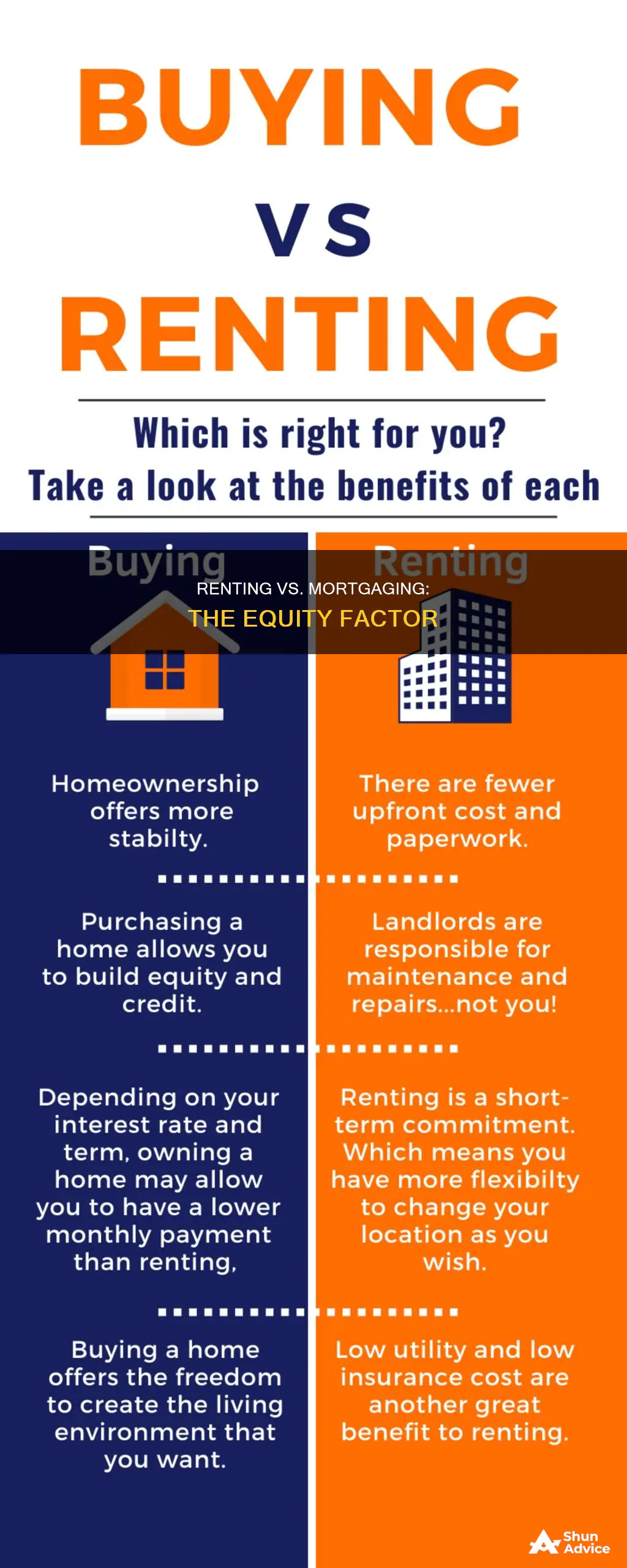

Renting doesn't build equity, unlike mortgages

Renting a property and taking out a mortgage on a property are two very different things. The most significant difference is that with renting, you do not own the property, whereas with a mortgage, you do. When you rent, you pay the owner of the property monthly. When you take out a mortgage, you borrow money from a bank to buy a property that you will own. You then pay back the loan with interest over time, typically with monthly payments.

Mortgages are a long-term financial commitment, often lasting between 15 and 30 years. They require a significant financial commitment upfront, but they also generate equity over time, especially if the property increases in value. Equity is the difference between the amount you owe on a mortgage and the property's market value. It is an asset that you can borrow against to meet important financial needs, such as paying off high-cost debt or funding a child's education.

Renting, on the other hand, does not give you the same opportunity to build long-term equity. While there are rent-to-own agreements that can serve as a middle ground between renting and mortgaging, these are usually more expensive than traditional rentals and require a long-term commitment. With renting, you also do not have the same flexibility as you would with owning a property. For example, you may be limited in what changes you can make to the property, and you may need to renew your rental agreement annually.

Overall, while renting can be a more flexible and short-term option, it does not provide the same financial benefits as owning a property through a mortgage. With a mortgage, you can build equity and have more control over your living situation. However, it is important to note that owning a home also comes with additional costs and commitments that rental properties do not.

Mortgages: Primary Residence Determinants and Their Impact

You may want to see also

![]()

Mortgages are loans from banks to buy a home

Mortgages are loans provided by banks to help you purchase your own home. They give you the money to buy the house, and you pay them back over time with interest. The cost of a mortgage is typically broken down into monthly payments that last anywhere from 15 to 30 years.

When you take out a mortgage, you are essentially taking a loan from a bank to buy a home. The bank will lend you the money you need to purchase the property, and you will be responsible for paying back the loan, usually over a long period. The monthly payments you make will consist of both the principal amount (the original sum borrowed) and the interest charged by the bank.

The interest rate on a mortgage can be fixed for the entire term of the loan or adjustable, meaning it will change periodically. A fixed-rate mortgage offers the advantage of predictable payments, while an adjustable-rate mortgage may provide more flexibility if interest rates decrease. It's important to shop around and compare rates from different lenders to find the best deal.

In addition to the interest rate, there are other factors to consider when taking out a mortgage. Down payment requirements can vary, with conventional mortgages typically requiring at least 20% down to avoid paying private mortgage insurance (PMI). However, there are also government-backed mortgage options, such as Federal Housing Administration (FHA) loans, that allow for lower down payments.

It's also worth noting that mortgages can be used to build equity in your home. Equity is the difference between the amount you owe on your mortgage and the current market value of your home. As you make payments and the property's value increases over time, your equity grows. This can be a significant advantage of owning a home over renting, as it allows you to build long-term wealth.

Overall, mortgages are a way for individuals to achieve the dream of homeownership by providing the necessary funds to purchase a property. It is important to carefully consider the terms, interest rates, and financial commitments involved before taking out a mortgage.

Hawaii's Mortgage Mystery: How Do Locals Afford It?

You may want to see also

![]()

Rent-to-own agreements are a middle ground

Renting and mortgages differ in terms of equity because, with a mortgage, you will eventually own the property, whereas with a rental agreement, you will not. A mortgage is a loan provided by a bank to help you purchase your own home. You pay the bank back over time with interest, and this cost is broken down into monthly payments. Each of these payments contributes to your equity in the property.

Rent-to-own agreements are more flexible than mortgages, as you are not required to purchase the home at the end of the agreement. However, they are also more of a commitment than a traditional rental, and you may lose money if you don't make a purchase at the end of the rental period. These agreements are also more expensive overall than a standard rental, and you may be responsible for property taxes, insurance, and repairs.

Before signing a rent-to-own agreement, it is important to carefully read the contract and consider the various financial elements. These agreements often include an upfront option fee, which is a set price that you pay to secure your option to buy. This fee is usually non-refundable and can be expected to be between 2% and 7% of the property's value. During the period that you live in the home prior to purchase, you will pay rent, and a portion of these payments will also go towards your future down payment.

It is also important to note that, while you are living in the home, you are still a renter according to the law, and the seller has the same legal rights as a landlord. You will need renters' insurance, and the insurance does not cover the seller.

Strategies for Managing Multiple Mortgages and Financial Freedom

You may want to see also

![]()

Home equity loans are for existing homeowners

When it comes to rentals and mortgages, the key difference is in the ownership of the property. With a mortgage, you take out a loan from a bank to purchase your own home, which you then pay back with interest over a long period, typically 15-30 years. On the other hand, renting involves paying the owner of the property on a monthly basis, with rental agreements usually lasting only 12 months. While buying a house requires a significant upfront financial commitment, it allows you to build equity over time, especially if the property appreciates in value.

Home equity loans are specifically for existing homeowners who have accumulated a sufficient level of equity in their homes. These loans are a type of second mortgage, allowing homeowners to borrow a lump sum of money against their current home equity. The loan is secured by the borrower's equity, which is the difference between the property's value and any existing mortgage balance. For example, if your home is valued at $250,000 and you owe $150,000 on your mortgage, you have $100,000 in equity that can be used as collateral for a home equity loan.

Home equity loans are typically used for large expenses, such as home repairs or renovations, debt consolidation, or education fees. They are a good option for those who know exactly how much they need to borrow and want to benefit from a fixed-rate payment. The loan term can range from 5 to 30 years, and the amount borrowed is generally limited to 80% of the total value of the borrower's equity.

It is important to note that failure to repay a home equity loan could result in foreclosure, as your home serves as collateral for the loan. Additionally, interest on the loan is only tax-deductible if it is used to buy, build, or substantially improve the home. Before taking out a home equity loan, it is advisable to carefully consider the risks and benefits, as well as consult a financial professional.

Cashing Out Refinance Mortgages: Strategies for Homeowners

You may want to see also

![]()

Home equity loans are secured by your equity

While renting a home, you don't get the opportunity to build long-term equity. On the other hand, buying a house with a mortgage generates equity over time, especially if the property appreciates in value.

Home equity is the difference between the amount you owe on a mortgage and the current market value of your home. It is an asset that you can borrow against to meet important financial needs. Home equity loans are a popular way for homeowners to tap into their home's value without selling it.

Home equity loans are a type of instalment loan that has to be repaid over a fixed term, which can range from five to 30 years. They are a popular choice for homeowners who want to take on some kind of home improvement project, as they provide an easy source of cash and can be valuable tools for responsible borrowers. However, failure to repay a home equity loan could put you at risk of foreclosure, as your home is the collateral for the loan.

Wall Street's Mortgage Business: How It Works

You may want to see also

Frequently asked questions

Rentals and mortgages differ in terms of equity in that rentals do not allow you to build equity, while mortgages do. This is because, with a mortgage, you own the property, whereas with a rental, you do not.

Home equity is the difference between the amount you owe on a mortgage and the current market value of the home.

You can build equity by making payments on your mortgage and by the property increasing in value.

A home equity loan is a type of loan that is secured by your home equity. It allows you to borrow a lump sum of money against your current home equity for a fixed rate over a fixed period.

The main difference is in their intent. A traditional mortgage is used to purchase a new home, whereas a home equity loan is used to borrow against existing equity in your home.