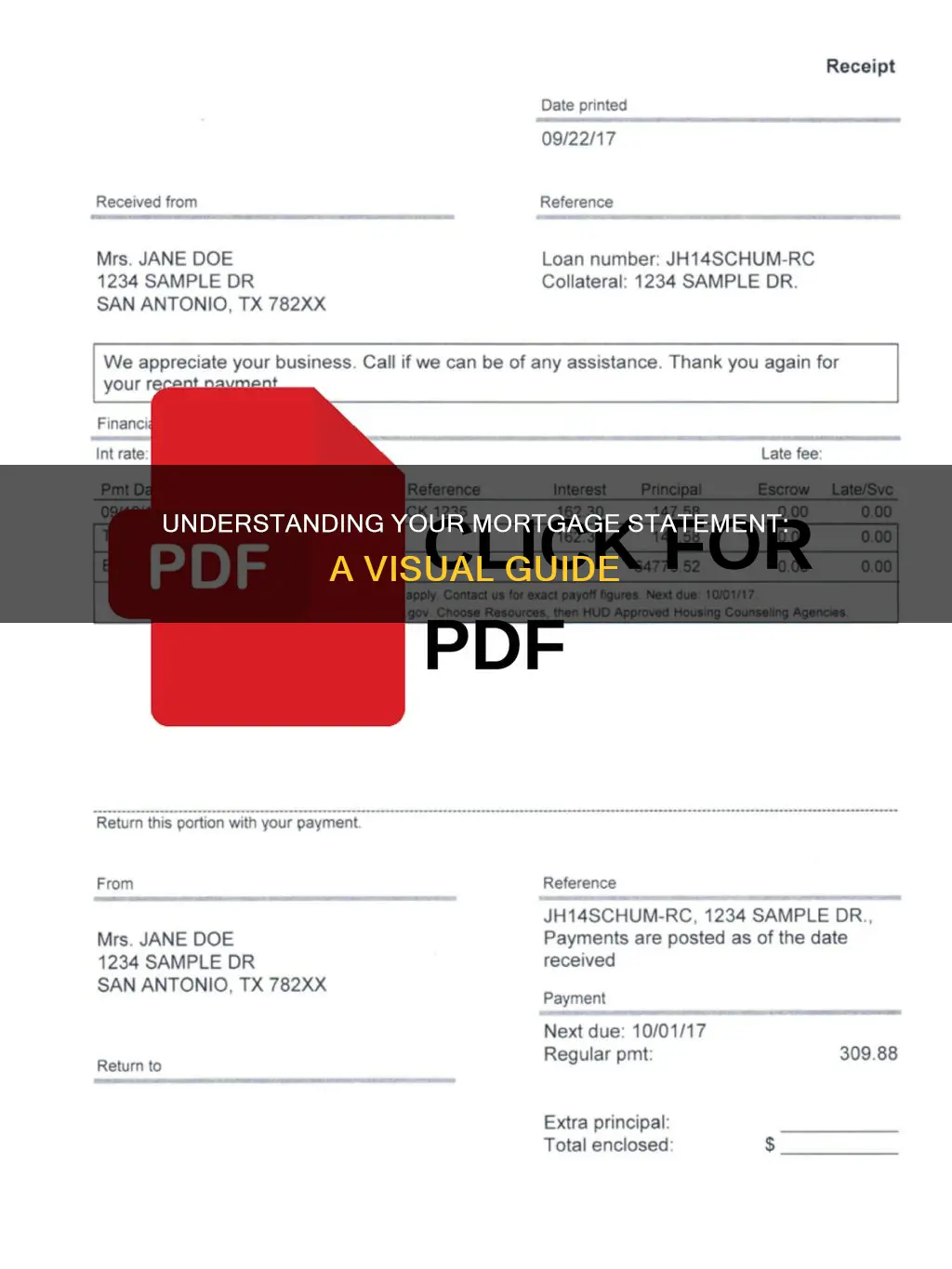

A mortgage statement is a document that provides an overview of your loan and the progress you're making in paying it off. It contains important information about your loan balance, monthly payments, and payment history. It also includes details such as the account or loan number, payment due date, amount due, and outstanding principal. The statement may also show your maturity date, i.e., how close or far you are from paying off your balance in full. Mortgage statements are typically issued monthly, but some lenders may send them quarterly.

| Characteristics | Values |

|---|---|

| Purpose | To keep the borrower informed about the health of their loan |

| Format | Standardized |

| Frequency | Monthly, or quarterly |

| Contents | Contact information, loan number, payment due date, amount due, outstanding principal, escrow balance, transaction activity, payment history, maturity date, interest rate changes, late fees |

| Payment Methods | By mail, by phone, in person |

![]()

Contact information

- Customer Care or Servicer Contact Details: This includes phone numbers, email addresses, physical addresses, and even fax numbers in some cases. The statement may provide separate contact information for general inquiries, technical support, and specific departments or individuals handling your account.

- Hours of Operation: Along with the contact numbers, the mortgage statement should specify the hours during which the customer care team or loan servicer can be reached. This information helps borrowers know the best times to call or visit the lender's office for assistance.

- Online Support: In today's digital age, many lenders offer online support through their websites or mobile apps. The contact information section of the mortgage statement may include website links, online account access instructions, or mobile app download information. These online resources often provide borrowers with convenient access to their loan details, payment history, and other relevant information.

- Mailing Addresses: Mortgage statements usually provide multiple mailing addresses for different purposes. For instance, there may be separate addresses for sending payments, submitting documents, or making information requests. It is important to use the correct address to ensure timely processing and avoid any delays.

- Email Addresses: Email communication is becoming increasingly common in the mortgage industry. The contact information section may include specific email addresses for different purposes, such as general inquiries, document submissions, or complaints. Using the appropriate email address helps ensure a prompt response and efficient handling of your query.

- Social Media Presence: Some lenders also include their social media handles or links to their social media profiles. This allows borrowers to connect with them on platforms like Facebook, Twitter, or LinkedIn. Social media can be a convenient channel for quick inquiries, sharing updates, and staying informed about the lender's latest offerings or promotions.

FHA Mortgages: Government Influence and Impact Explored

You may want to see also

![]()

Loan number

The loan number is a crucial component of a mortgage statement. It is a unique identifier for the client's loan and is essential for proper account identification and management. This number is typically displayed when logging into the servicer's website or mobile application and is required when contacting the servicer for any account-related inquiries or issues.

The loan number is a key reference point for both the borrower and the loan servicer, ensuring that communications regarding the loan are accurate and efficient. It helps borrowers keep track of their loan details, payment history, and progress toward paying off the mortgage. Additionally, it assists loan servicers in managing the loan, addressing any issues or discrepancies, and providing accurate advice to their clients.

By referring to the loan number, borrowers can access valuable information about their loan, such as the current balance, interest rates, payment breakdown, and any associated fees. This information empowers borrowers to make informed decisions regarding their loan, including refinancing options or accessing their home's equity. It also enables them to identify and address any errors or discrepancies in a timely manner, avoiding potential financial pitfalls.

Furthermore, the loan number plays a vital role in customer support. When borrowers contact their mortgage servicer, having the loan number readily available ensures that their inquiry is addressed promptly and accurately. It helps the servicer quickly locate the specific loan details, track payment history, and provide tailored solutions or recommendations to the borrower. This streamlined process enhances the overall customer experience and ensures effective issue resolution.

In summary, the loan number is a critical piece of information within a mortgage statement. It serves as a central reference point for both borrowers and loan servicers, facilitating efficient communication, accurate record-keeping, and informed decision-making. By utilising the loan number, borrowers can stay informed about their loan's status and take control of their financial obligations.

Mortgage Brokers: Verifying License Numbers and Legitimacy

You may want to see also

![]()

Payment due date

The payment due date is a critical component of a mortgage statement. It is the deadline by which your monthly mortgage payment must be received. Typically, mortgage payments are due on the first of the month, and if you have set up auto-payments, this due date serves as a reminder of when the funds will be debited from your bank account. It is important to note that if you pay by mail, you should allow several days for the payment to arrive before the due date to avoid late fees. Most servicers offer a grace period of around two weeks or 15 days before charging a late fee.

The amount due on the payment due date includes the full payment, comprising the principal, interest, and any applicable fees or charges. It is important to review the breakdown of the amount due to understand how your payment is allocated each month. This allocation may include escrow payments, which cover property taxes, homeowners insurance, and mortgage insurance.

If you are unable to make the payment by the due date, it is important to be aware of any late fees that may apply. These late fees should be outlined in your mortgage statement. Additionally, if you have made extra payments or overpayments, it is worth noting that this can affect the maturity date, bringing you closer to paying off your loan balance in full.

The payment due date section of your mortgage statement may also include important messages or alerts about your account. It is advisable to review this section regularly to stay informed about any changes or updates to your mortgage terms.

Understanding Your Mortgage Bill: A Breakdown

You may want to see also

![]()

Amount due

The "Amount Due" section of a mortgage statement is a critical component that outlines the financial obligations associated with your loan. This section is typically found at the bottom of the billing statement and provides a detailed breakdown of the upcoming payment you need to make.

The amount due encompasses the full payment that must be received by the due date. This includes the principal, which is the outstanding balance of your mortgage loan, and the interest accrued on that principal amount. If applicable, it may also include escrow payments. Escrow is a portion of your monthly payment that covers property taxes, homeowners insurance, and mortgage insurance. By paying more than the amount due, you can reduce the total interest paid over the life of the loan.

Late fees are another aspect that may be included in the amount due. Most lenders offer a grace period, typically ranging from 15 to 60 days, before charging a late fee. However, it's important to be mindful of these additional charges to avoid any unexpected costs.

The amount due section also provides transparency into how your payment is allocated. It breaks down the distribution of funds towards the principal, interest, escrow (if applicable), and any other fees or charges. This information empowers you to understand how each dollar of your mortgage payment is spent.

Additionally, the mortgage statement may include important messages or alerts related to your account. These messages could provide updates or notifications about rate changes, especially if you have an adjustable-rate mortgage (ARM). Staying vigilant about these messages can help you make informed decisions, such as exploring refinancing options or converting to a fixed-rate loan.

Understanding Mortgage Increases: Factors Behind Rising Payments

You may want to see also

![]()

Interest rate changes

Types of Interest Rates:

There are two primary types of interest rates for mortgages: adjustable-rate mortgages (ARMs) and fixed-rate mortgages. With an adjustable-rate mortgage, your interest rate will fluctuate over time. This means that your monthly payments can increase or decrease depending on market conditions and other factors. On the other hand, a fixed-rate mortgage locks in your interest rate for the entire duration of the loan, keeping your monthly payments consistent.

Factors Affecting Interest Rate Changes:

Several factors influence interest rate changes, and these can be broadly categorized into personal and market factors. Personal factors include your credit history, income, debt-to-income (DTI) ratio, down payment amount, and occupancy status. Lenders use these factors to assess your risk level and determine the interest rate offered. For example, a lower DTI ratio often results in a lower interest rate. Market factors, such as economic conditions, inflation, competition in the local market, and government-backed loans, also play a significant role in interest rate fluctuations. When the economy is thriving, with low unemployment and high spending, mortgage rates tend to increase. Conversely, during economic downturns, interest rates typically decrease to encourage borrowing.

Impact on Monthly Payments:

Notices and Information:

If you have an adjustable-rate mortgage (ARM), it is crucial to review your monthly mortgage statement for interest rate changes. While your loan servicer is required to notify you of upcoming rate adjustments, staying informed helps you prepare for any budget adjustments. Additionally, these notices will detail how the changes will affect your monthly payments. By reviewing these statements, you can make informed decisions, such as whether to refinance to a fixed-rate loan or shop for new insurance.

Planning for Interest Rate Increases:

To plan for potential interest rate increases, consider the following:

- Review your amortization schedule: This schedule, provided with your closing papers, shows how your payments are allocated between interest and principal. It helps you understand how interest rate changes will impact your payments over time.

- Monitor market conditions: Stay informed about economic trends and interest rate forecasts. Understanding the broader context can help you anticipate potential rate changes.

- Maintain a good credit score: A higher credit score can put you in a better position to negotiate lower interest rates or secure more favourable loan terms.

- Make a larger down payment: A substantial down payment can help you secure a lower interest rate and reduce your monthly payments.

Understanding the Components of Your Mortgage

You may want to see also

Frequently asked questions

A mortgage statement is a document that includes key details about your loan. It is a financial report card for your loan that outlines your payment history, outstanding balance, interest accrued, and other key details.

A mortgage statement contains information about your account, payment history, and how much is due for your next mortgage payment. It also includes the outstanding principal, which is the amount of money you owe on your mortgage loan.

Mortgage statements are typically issued monthly, but some lenders may send them quarterly. You will receive a statement from your lender or servicer for each billing cycle.

The primary purpose of a mortgage statement is to keep a borrower informed about the health of their loan. It serves as a reference point for understanding their financial obligations and tracking their progress toward paying off the mortgage.

A mortgage statement will include your account/loan number, payment due date, amount due, and outstanding principal. It will also include an explanation of the amount due, transaction activity, and any important messages.