Investing is a powerful tool for growing your wealth, but understanding how revenue from investments works is crucial for making informed financial decisions. When you invest, you essentially lend money to a company or purchase an asset with the expectation that it will generate returns over time. These returns can come in various forms, such as dividends, interest, or capital gains. Dividends are a portion of a company's profits paid out to shareholders, while interest is the income earned from lending money to others. Capital gains occur when the value of an investment increases, and you sell it for a profit. The revenue from investing is a key factor in financial planning, as it can provide a steady stream of income, contribute to long-term wealth accumulation, and offer a means to achieve financial goals.

What You'll Learn

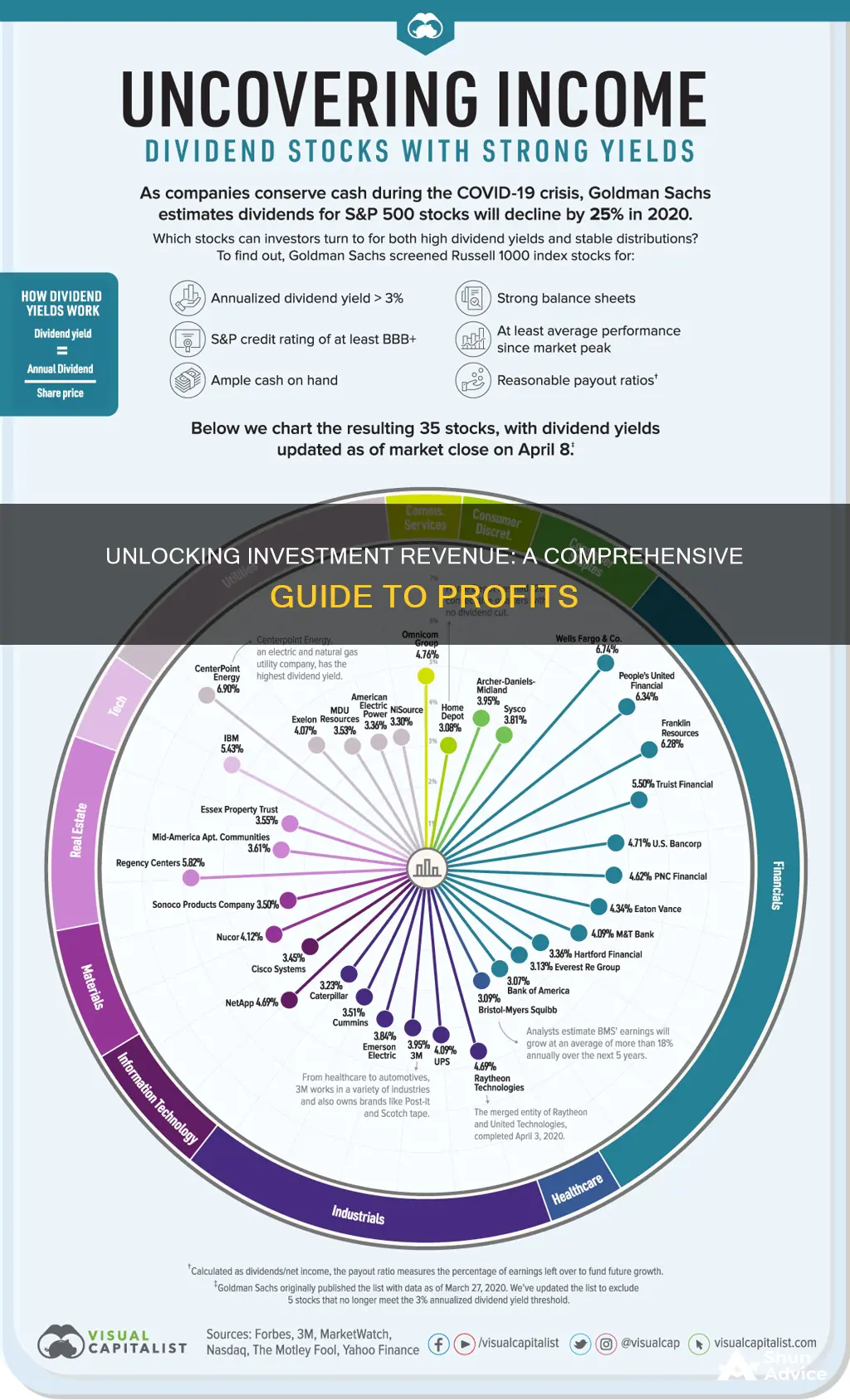

- Understanding Investment Returns: How are profits calculated from investments

- Types of Investment Income: Interest, dividends, capital gains, and more

- Tax Implications: How taxes affect investment revenue

- Risk and Return: The relationship between risk and potential profits

- Investment Strategies: Methods to maximize investment revenue

![]()

Understanding Investment Returns: How are profits calculated from investments?

When you invest, you're essentially putting your money to work with the expectation of generating a return. This return is the profit or gain you make from your investment. The process of calculating investment returns involves several key concepts and formulas that investors should understand. Here's a detailed breakdown:

- Capital Appreciation: This is the most common way investors make money from their investments. It refers to the increase in the value of an asset, such as a stock or a property, over time. For example, if you buy a stock for $100 and it appreciates to $150 over the year, you've made a capital gain of $50. This gain is realized when you sell the asset.

- Dividend Income: Many investments, especially stocks, offer dividends, which are a portion of the company's profits distributed to shareholders. Dividends can be a regular source of income for investors. The return on investment (ROI) is calculated by dividing the annual dividend by the initial investment and then multiplying by 100 to get a percentage. For instance, if you receive a $10 dividend on a $100 investment, your ROI for that year would be 10%.

- Interest and Coupon Payments: For fixed-income investments like bonds, the return is typically generated through interest payments. Bonds pay interest at a fixed rate, known as the coupon rate. The formula to calculate the return on a bond investment is similar to that of dividend income. You divide the annual interest payment by the bond's purchase price and then multiply by 100.

- Total Return: This metric provides a comprehensive view of an investment's performance, including both capital gains and income. It is calculated by adding the capital gain (or loss) and the income generated (dividends, interest, etc.) over a specific period. For instance, if you made a $50 capital gain and received $10 in dividends, your total return would be $60.

- Compound Returns: This concept is crucial for long-term investors. Compound returns mean that not only do you earn a return on your initial investment, but you also earn returns on the accumulated gains from previous periods. Over time, compound returns can significantly boost your investment's value. For example, if an investment generates a 10% return annually, after three years, the total return would be 10% + 10% of 10% + 10% of 10% of 100%, resulting in a higher overall gain.

Understanding these concepts will help investors make informed decisions about their investment strategies, risk tolerance, and expected returns. It's important to remember that investment returns can vary widely depending on market conditions, asset types, and individual investment choices.

Networking: Your Secret Weapon for Success

You may want to see also

![]()

Types of Investment Income: Interest, dividends, capital gains, and more

When you invest your money, you're essentially lending it to a company, government, or other entity in exchange for a return. This return is what we call investment income, and it comes in various forms. Understanding these different types of income is crucial for investors as it directly impacts their overall returns and financial goals. Here's a breakdown of the most common ones:

Interest: This is the most basic and common form of investment income. When you deposit money into a savings account or buy a bond, you're lending your funds to the bank or the issuer of the bond. In return, they pay you interest, which is a percentage of the principal amount (the initial sum you invested) over a specified period. Interest rates can vary widely depending on the type of investment and market conditions. For instance, savings accounts typically offer lower interest rates compared to corporate bonds, which carry higher risk but also higher potential returns.

Dividends: Dividends are a share of the profits a company distributes to its shareholders. When a company earns a profit, it can choose to reinvest it into the business or distribute a portion of it to its investors. Investors who own shares in a company are entitled to a portion of these profits in the form of dividends. Dividend payments can be regular (annual, quarterly) or irregular, depending on the company's performance and decisions. Dividend-paying stocks are often favored by income-seeking investors, as they provide a steady stream of income.

Capital Gains: Capital gains are the profit realized from the sale of a capital asset, such as stocks, bonds, or real estate. When you buy an asset at a certain price and sell it at a higher price, the difference is a capital gain. This type of income is often associated with long-term investments, where the asset is held for an extended period. Capital gains are typically taxed at a different rate than regular income, and the tax rate can vary depending on the holding period and the investor's tax bracket.

Rental Income: This is the income generated from renting out an asset, such as a property or equipment. For example, if you own a rental house, you can earn rental income by leasing it to tenants. This type of income is more common in the real estate market, but it can also apply to other assets like machinery or equipment. Rental income can provide a steady cash flow, but it also comes with responsibilities like property maintenance and tenant management.

Other Income Sources: Beyond the above, there are other ways to generate investment income. Some investors explore peer-to-peer lending, where they lend money directly to individuals or businesses, often through online platforms. This can offer higher interest rates but also carries higher risk. Additionally, some investors engage in real estate investment trusts (REITs), which allow them to invest in income-generating real estate without directly owning property.

Understanding these various types of investment income is essential for investors to make informed decisions and build a diversified portfolio. Each income stream has its own characteristics, risks, and potential rewards, and investors should carefully consider their financial goals, risk tolerance, and time horizon when choosing investment vehicles.

Heavy Price Tag, Heavy Considerations

You may want to see also

![]()

Tax Implications: How taxes affect investment revenue

Understanding the tax implications of investment revenue is crucial for investors as it directly impacts their overall returns. When you invest, whether in stocks, bonds, real estate, or other assets, the income generated from these investments is typically subject to taxation. This is an essential aspect of the revenue cycle in investing, as it determines how much of your investment gains you can keep after accounting for taxes.

The tax treatment of investment income varies depending on the type of investment and the tax laws in your jurisdiction. In many countries, investment income is classified as either ordinary income or capital gains. Ordinary income, such as dividends or interest, is usually taxed at the same rates as your regular income. This means that the tax rate applied to these earnings is often higher than the rate for capital gains. For instance, in the United States, qualified dividends and long-term capital gains are typically taxed at lower rates than ordinary income.

Capital gains, on the other hand, are taxes levied on the profit realized from the sale of an asset. The tax rate for capital gains can vary based on the holding period of the investment and the investor's income level. Short-term capital gains are generally taxed as ordinary income, while long-term capital gains often qualify for reduced rates. For example, in the US, long-term capital gains are taxed at 0%, 15%, or 20%, depending on the taxpayer's income.

Taxes can significantly impact investment returns, and understanding the rules can help investors make more informed decisions. Investors should be aware of the tax consequences of different investment strategies. For instance, tax-efficient investing involves strategies like tax-loss harvesting, where investors sell investments at a loss to offset capital gains, thus reducing their taxable income. Additionally, tax-advantaged accounts, such as retirement accounts, offer tax benefits that can enhance investment returns over time.

It is essential to consult with tax professionals or financial advisors to navigate the complex world of investment taxation. They can provide personalized advice on tax-efficient investment strategies, help optimize tax treatments, and ensure compliance with tax laws. By understanding the tax implications, investors can make better-informed choices, potentially increasing their after-tax returns and overall investment success.

TD Ameritrade: Your Investment Companion

You may want to see also

![]()

Risk and Return: The relationship between risk and potential profits

The concept of risk and return is fundamental to understanding the world of investing. It is a principle that governs the financial markets and is a key consideration for any investor. At its core, the relationship between risk and return is a trade-off: the higher the potential return, the greater the risk involved. This principle is often referred to as the 'risk-return trade-off' and is a critical aspect of investment strategy.

When investing, individuals or institutions allocate capital with the expectation of generating a profit. This profit is directly linked to the level of risk taken. Higher-risk investments often promise greater potential returns, while lower-risk options typically offer more modest gains. For example, a conservative investor might choose government bonds, which are generally considered low-risk, for a steady but small return. In contrast, a more aggressive investor might invest in high-risk, high-reward assets like startup companies or volatile stocks, aiming for substantial profits but at the cost of increased risk.

The relationship is not linear; it is a complex interplay of various factors. Market volatility, economic conditions, company-specific risks, and even geopolitical events can all influence the risk-return dynamic. For instance, during economic downturns, the stock market may experience a significant decline, leading to potential losses for investors. However, this same period could also present opportunities for those willing to take on higher risk, as markets tend to recover over time.

Understanding this relationship is crucial for investors to make informed decisions. It involves assessing one's risk tolerance, which is the level of uncertainty an investor can handle without experiencing significant financial distress. Investors with a higher risk tolerance might be more inclined to take on substantial risks for the potential of high returns. Conversely, those with a lower tolerance may prefer safer investments, even if they offer lower potential profits.

In summary, the relationship between risk and return is a delicate balance that investors must navigate. It requires a comprehensive understanding of the market, a clear definition of one's investment goals, and a realistic assessment of risk tolerance. This understanding enables investors to make strategic choices, ensuring their financial decisions align with their risk appetite and long-term objectives.

Unraveling the IRA Investment Mystery: A Comprehensive Guide

You may want to see also

![]()

Investment Strategies: Methods to maximize investment revenue

Understanding how revenue from investments works is crucial for anyone looking to grow their wealth. Investment revenue is essentially the profit or gain generated from an investment, and it can come in various forms. When you invest, you typically aim to earn a return on your capital, which can be achieved through different strategies. Here are some methods to maximize investment revenue:

- Diversification: One of the fundamental principles of investing is diversification. This strategy involves spreading your investments across various asset classes such as stocks, bonds, real estate, and commodities. By diversifying, you reduce the risk associated with any single investment. For example, if you invest solely in tech stocks, a downturn in the tech sector could significantly impact your overall portfolio. However, by diversifying into different sectors and asset types, you create a more balanced approach. This method ensures that your revenue streams are not solely dependent on one market or industry, providing a more stable and consistent return over time.

- Long-Term Investing: Maximizing investment revenue often requires a long-term perspective. Short-term market fluctuations can be common, but over an extended period, the market tends to trend upwards. Long-term investing allows you to ride out these short-term volatility periods and benefit from the overall growth of the markets. For instance, investing in index funds or exchange-traded funds (ETFs) that track a broad market index can provide exposure to a diverse range of companies, reducing risk. This strategy is particularly effective for retirement planning, where consistent, long-term growth can accumulate significant wealth over time.

- Compound Interest and Reinvestment: Compound interest is a powerful tool for growing your investment revenue. When you reinvest the earnings or dividends from your investments, you earn interest on the new, larger principal amount. This process can lead to exponential growth over time. For instance, if you invest $10,000 and earn a 5% annual return, you'll have approximately $12,500 after the first year. Reinvesting this $12,500 at the same rate will result in $13,761 at the end of the second year. This compound effect can significantly boost your revenue, especially when combined with regular contributions to your investment portfolio.

- Risk Assessment and Management: Maximizing revenue requires a careful assessment and management of risk. Every investment carries some level of risk, and understanding your risk tolerance is essential. Some investments are more volatile and carry higher risks, while others provide more stable returns. Diversification, as mentioned earlier, is a way to manage risk. Additionally, you can consider investing in assets that have historically shown resilience during market downturns. For example, gold is often seen as a safe-haven asset, and its value tends to increase when other markets decline. Managing risk effectively ensures that your revenue-generating investments remain stable and consistent.

- Research and Education: Staying informed and continuously learning about the investment landscape is vital. Keep up with market trends, economic indicators, and industry-specific news. Educate yourself on different investment products, their characteristics, and potential risks. This knowledge will enable you to make more informed decisions and adapt your strategies accordingly. Consider consulting financial advisors or using online resources to gain insights and stay updated on the latest investment opportunities and best practices.

By implementing these investment strategies, you can work towards maximizing your revenue potential while managing risk effectively. Remember, investing is a long-term game, and a well-diversified, patient approach is often the key to success.

The Power of Compounding: Unlocking the Secret to Rapid Investment Growth

You may want to see also

Frequently asked questions

Revenue from investing typically comes from the returns on your investments. This can be in the form of capital gains, which are the profits made when you sell an asset for a higher price than its purchase price. Additionally, investing in dividend-paying stocks or funds can provide regular income in the form of dividends.

Capital gains are the profit realized from the sale of a property or investment, such as stocks or real estate. It is the difference between the original purchase price and the selling price. Dividends, on the other hand, are a portion of a company's profits paid out to shareholders. They are usually a regular payment and can be reinvested to earn more returns.

Maximizing investment revenue involves a strategic approach. Diversification is key; spread your investments across different asset classes like stocks, bonds, and real estate to reduce risk. Regularly review and rebalance your portfolio to ensure it aligns with your financial goals. Consider investing in growth stocks or funds that have the potential for higher returns over time. Also, stay informed about market trends and economic factors that can impact your investments.

Yes, investing always carries some level of risk. Market volatility can cause fluctuations in the value of your investments, and there's a chance of losing some or all of your capital. It's important to understand your risk tolerance and invest accordingly. Additionally, external factors like economic downturns or geopolitical events can impact investment performance. Proper research and a long-term investment strategy can help mitigate these risks.

To calculate the total revenue, you need to consider both capital gains and dividend income. Start by adding up all the capital gains realized from selling investments. Then, sum up the dividend payments received over a specific period. These figures will give you an estimate of your total revenue from investing. It's a good practice to keep detailed records of your investment transactions and income to ensure accurate calculations.