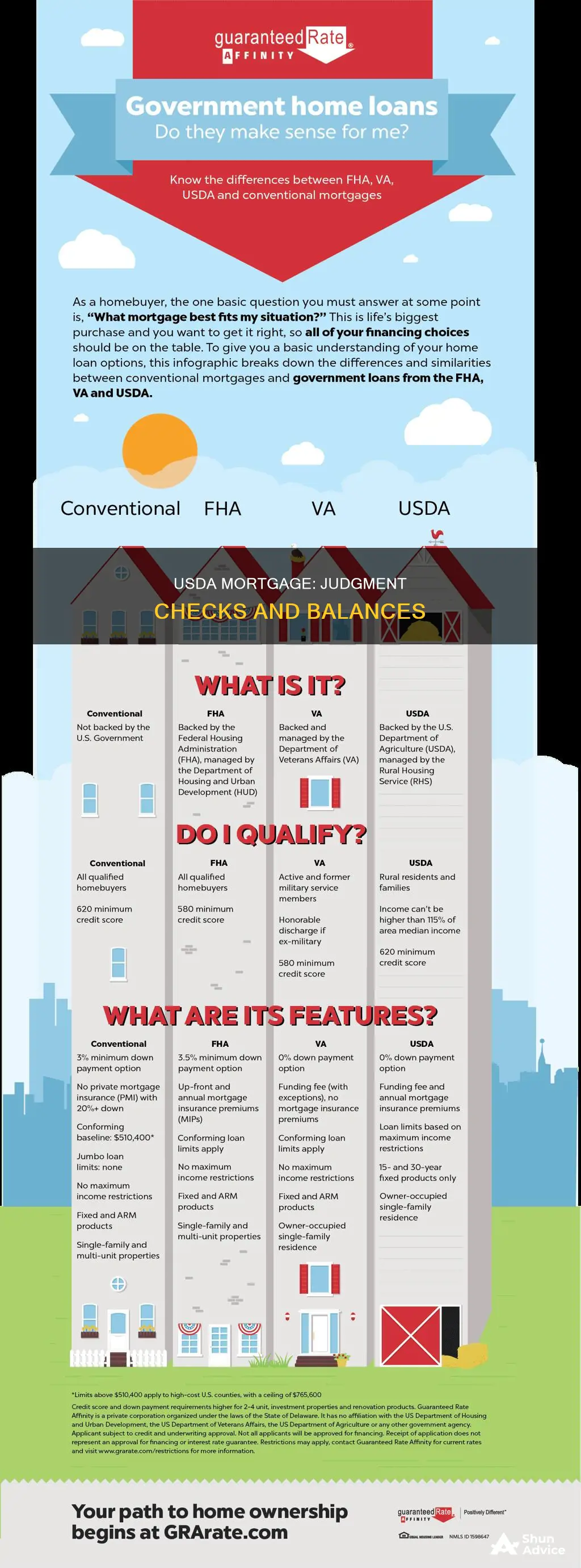

USDA loans are a popular mortgage choice for borrowers as they require no down payment and have flexible credit score requirements compared to conventional loans. However, to get approved, borrowers must meet specific eligibility criteria, including minimum credit standards, stable employment history, and purchasing a property that meets USDA guidelines. The USDA also assesses the borrower's debt-to-income ratio (DTI), comparing monthly debt payments to gross monthly income. Additionally, the property must be appraised by a USDA-approved inspector to ensure it meets the required standards and is located in an eligible rural area.

| Characteristics | Values |

|---|---|

| Credit score | Must meet the lender's benchmark |

| Credit report | Should not include bills sent to collection, recently opened lines of credit, or other factors that lower the credit score |

| Debt-to-income ratio (DTI) | Monthly housing expenses should be 29% or less of gross monthly income; general debts should not exceed 41% of gross monthly income |

| Property type | Must be in a "rural" area as defined by the USDA and must meet property condition requirements |

| Employment history | Must demonstrate stable employment |

What You'll Learn

![]()

Credit scores and credit reports

Before applying for a USDA mortgage, it is highly recommended to review your credit reports. Credit scores are derived from the information contained in these reports, and any inaccuracies or outdated items can impact your score. By law, you can obtain free copies of your credit reports from AnnualCreditReport.com. This allows you to verify the factual correctness of your credit history and address any discrepancies.

USDA loans are known for their more flexible credit requirements compared to conventional loans. However, maintaining a good credit score during the application process is vital. Any negative changes to your credit profile, such as unpaid bills sent to collection or new lines of credit, can lower your score and lead to loan denial. Therefore, it is advisable to minimise activities that could negatively impact your credit score while your application is being processed.

Additionally, the USDA loan program considers debt-to-income ratios (DTIs) as a critical factor in mortgage underwriting. DTIs compare your monthly debt payments with your gross monthly income. The USDA sets specific DTI thresholds for housing expenses (29% or less) and general debts (41% or less). Staying within these guidelines improves your creditworthiness and increases your chances of obtaining a USDA mortgage.

SunTrust Mortgage: Navigating Foreclosure and Your Options

You may want to see also

![]()

Debt-to-income ratios

When applying for a USDA mortgage, your debt-to-income ratio (DTI) is a crucial factor in determining your eligibility. Lenders use your DTI to assess whether you can afford to take on a mortgage payment alongside your existing debts.

Your DTI reflects the percentage of your gross monthly income that goes towards paying off debts. To calculate it, you must first add up all your regular, required, and recurring monthly debt payments, ensuring you only include the minimum payments. Then, divide this total by your monthly pre-tax income. The result is your DTI, expressed as a percentage.

A lower DTI indicates a lower risk to lenders. USDA loans typically require a maximum housing DTI of 29% and a maximum total DTI of 41%. However, if your credit score is above 660, you may be able to exceed the 41% guideline. Additionally, a consistent work history of one to two years is generally required, with a longer work history typically needed for self-employed individuals.

It's important to note that your DTI does not include all your monthly expenses, such as groceries, utilities, or taxes. Lenders use your gross monthly income, which is higher than your take-home pay, so it's essential to create a household budget to accurately determine the maximum mortgage payment you can afford.

Securitization Obscures Default Mortgages: Hiding in Plain Sight

You may want to see also

![]()

Property type and condition

Secondly, the property must be a standard single-family home, as USDA loans typically do not finance income-producing properties, multi-unit dwellings, or manufactured homes that don't meet specific HUD requirements. The home's lot size should also be considered, as excessive acreage, especially if used for farming, may disqualify the property.

Most importantly, the USDA requires the property to be in good condition and safe for occupancy. This means addressing any structural issues, safety hazards, lack of basic amenities, pest infestations, and environmental hazards. Structural issues could include major problems with the foundation, roof, or overall structure. Safety hazards, such as exposed wiring or the absence of smoke detectors, must be rectified. Basic amenities like functional electricity, heating, and water systems are essential. Pest infestations, particularly termites or other wood-destroying insects, are a concern. Additionally, environmental hazards, such as the presence of lead-based paint in older homes, need to be addressed.

USDA-approved lenders will send out an appraiser to assess the home's value and condition to ensure it meets these standards. It is beneficial to consult with a USDA loan specialist to understand property requirements and identify eligible homes that meet your needs.

Lower Fees, Bigger Benefits: Refinancing Your Mortgage

You may want to see also

![]()

Employment history

Lenders typically require documentation of an applicant's earnings, such as tax returns and financial statements. They also assess the stability of the applicant's income, considering any fluctuations in income received. Lenders may also require additional documentation for self-employed individuals, including tax returns and profit and loss statements for the previous two years.

It is important to note that lenders are generally less concerned with the specific job or job title and are more focused on the stability of the applicant's income. As such, changing jobs or having multiple employers within the past two years does not automatically disqualify an applicant. However, lenders may require explanations for significant employment gaps or career changes.

USDA guidelines allow for explainable employment gaps of six months or more, provided that the applicant can document the reason for the gap, has been employed for at least six months following the gap, and has a two-year employment history prior to the gap. Additionally, applicants who have been unemployed for an extended period or have had sporadic employment may be viewed as high-risk by lenders, potentially impacting their eligibility for a USDA mortgage.

To increase the chances of approval, it is recommended to work with an experienced mortgage lender before applying. This allows applicants to confirm that their income meets USDA limits and that their employment history aligns with the requirements for mortgage approval.

Understanding the Mortgage Process: A Step-by-Step Guide

You may want to see also

![]()

Income requirements

The USDA loan program is designed to help borrowers of modest financial means secure a mortgage with no down payment. As such, there are strict income requirements that must be met to qualify for this type of loan.

The USDA uses an income multiplier and set income limits to determine eligibility. The income multiplier, or 'income limit threshold', is currently set at 115% of the median income for an area. This means that to be eligible for a USDA loan, a borrower's total income cannot exceed this threshold. The limit is adjusted for family size, with a two-person household allowed a higher income than a single-person household, for example. The USDA also takes into consideration elderly family members and any dependents under 18 or in full-time education.

The income limits are set by county and metropolitan area, with data provided by the US Census Bureau. These limits are reviewed and adjusted annually. The USDA publishes a full list of income limits by location, which can be used to check eligibility.

When assessing income, the USDA takes into account the total income of all members of the household, regardless of whether they are listed on the loan application. This includes regular income from employment, but also any additional income such as overtime, bonuses, commission, and seasonal work. Other sources of income, such as child support, alimony, and retirement benefits, are also considered. Self-employed applicants must provide tax returns to verify income.

The USDA also considers expenses and debt-to-income ratios when assessing eligibility. The total mortgage payment, including property taxes and insurance, should not exceed 29% of the borrower's monthly income. Additionally, the total debt, including the mortgage, car payments, credit cards, student loans, and other debts, should not exceed 41% of the borrower's monthly income. These ratios are used to assess the borrower's ability to repay the loan.

Refinancing Your Mortgage: A Guide to Lowering Payments

You may want to see also

Frequently asked questions

The USDA looks at two types of debt-to-income (DTI) ratios: monthly housing expenses and debts in general. Monthly housing expenses should be 29% or less of your gross monthly income, while debts in general should not exceed 41% of your gross monthly income. Additionally, the USDA requires borrowers to meet minimum credit standards, demonstrate stable employment history, and purchase a property that meets eligibility guidelines.

The USDA has an eligible property map that you can refer to in order to determine if a property is considered "rural." Additionally, the property must meet broad property condition requirements, including the condition of the roofing, foundations, electrical services, plumbing, and HVAC systems.

There are several reasons why a USDA loan may be denied, including changes to your credit profile during the application process, issues with the property appraisal, or not meeting the minimum credit standards or employment history requirements. If your loan is denied, you can try to get approved with manual underwriting by providing additional documentation and explanations for any issues. You may also need to reduce your debt levels and lower your costs for several months before reapplying.