If you're looking to buy a new home, it's important to understand how to calculate your mortgage payments. This will help you determine how much house you can afford and set a budget for your home search. A mortgage is a loan secured by property, usually real estate, and lenders define it as the money borrowed to pay for that property. Your monthly mortgage payment includes the principal, which is the original amount borrowed, and the interest, which is the cost of borrowing that money. There are several additional costs to consider, such as property taxes, homeowners insurance, and private mortgage insurance (PMI) if your down payment is less than 20%. You can use a mortgage calculator to estimate your monthly payments, taking into account factors like the loan amount, interest rate, loan term, and down payment. These calculators can also help you compare loan scenarios and plan for other costs. Additionally, understanding the concept of amortization can help you see how extra payments impact the overall interest you pay. By calculating your potential mortgage payments, you can make informed decisions about your home purchase and ensure that your monthly payments fit comfortably within your budget.

| Characteristics | Values |

|---|---|

| Loan amount | The amount borrowed from a lender or bank. |

| Down payment | The upfront payment of the purchase, usually a percentage of the total price. |

| Interest rate | The cost of borrowing money, expressed as an annual percentage. |

| Loan term | The number of years it will take to pay off the mortgage. |

| Property taxes | Annual tax levied by the city, county, or municipality. |

| Homeowners insurance | Annual fee for a standard insurance policy that covers damage to property and belongings. |

| HOA fees | Monthly dues paid to a homeowners association, which manages planned neighborhoods or condo communities. |

| Mortgage insurance | Required if the down payment is less than 20% of the home's purchase price. |

| Closing costs | Attorney fees, title service costs, recording fees, survey fees, property transfer taxes, brokerage commissions, mortgage application fees, appraisal fees, inspection fees, etc. |

| Renovations | Initial renovations may include changing flooring, repainting walls, updating the kitchen, or overhauling the interior/exterior. |

| Debt-to-income ratio | Lenders use the 28/36 rule, where housing expenses shouldn't exceed 28% of gross income, and total debt payments shouldn't exceed 36%. |

What You'll Learn

![]()

Calculating monthly mortgage payments

There are several online mortgage calculators available that can help estimate monthly mortgage payments. These calculators require inputs such as the loan amount, interest rate, and loan term (number of years). For example, if you enter a loan amount of $200,000, an interest rate of 4%, and a loan term of 30 years, the calculator will display the monthly payment, total interest, and other details.

It is important to note that monthly mortgage payments are not the only financial consideration when owning a house. There are also recurring and non-recurring costs, such as property taxes, home insurance, HOA (homeowners association) fees, and mortgage insurance. Property taxes are levied by the city, county, or municipality, while homeowners insurance covers damage to the property and its contents. HOA fees are paid by homeowners in certain communities to manage amenities, maintenance, and insurance. Mortgage insurance is required if the down payment is less than 20% of the home's purchase price.

Additionally, there are closing costs associated with obtaining a mortgage, which can include attorney fees, title service costs, recording fees, inspection fees, and more. These costs can amount to thousands of dollars and are typically paid by the buyer, although they can sometimes be negotiated with the seller or lender.

When calculating monthly mortgage payments, it is essential to consider all these factors to get an accurate understanding of the financial commitment involved in owning a home.

The True Cost of a Mortgage

You may want to see also

![]()

Using a refinance calculator

A refinance calculator is a useful tool to help you decide whether to refinance your mortgage. It can show you the potential savings of a new mortgage and help you evaluate whether it will help you meet your financial goals.

To use a refinance calculator, you will need to input details of your existing mortgage and information about your financial situation. This includes the remaining loan amount, the number of years left to pay, and the interest rate. You will also need to provide details about your income, such as recent pay stubs and bank statements.

With this information, the calculator will be able to estimate your new monthly payment and provide a breakdown of your savings. It will also take into account any fees associated with refinancing, such as closing costs, which can vary depending on your location, loan type, loan size, and mortgage lender.

When using a refinance calculator, you can compare the monthly payment of your current loan to the proposed payment on the new loan. It is generally considered worthwhile to refinance if the total interest expected to be paid over the life of the new loan is less than the cost of acquiring it. You can also calculate the breakeven point, which is the number of months it will take for the savings from the new loan to outweigh the costs of refinancing. If you plan to sell your home before reaching this breakeven point, refinancing may not be financially beneficial.

There are several free refinance calculators available online, such as those offered by Zillow and Bank of America. These calculators can help you understand the potential benefits of refinancing, including lowering monthly payments, reducing interest rates, or changing the length of your loan.

Wells Fargo's Mortgage Knowledge: How They Know Your Loan

You may want to see also

![]()

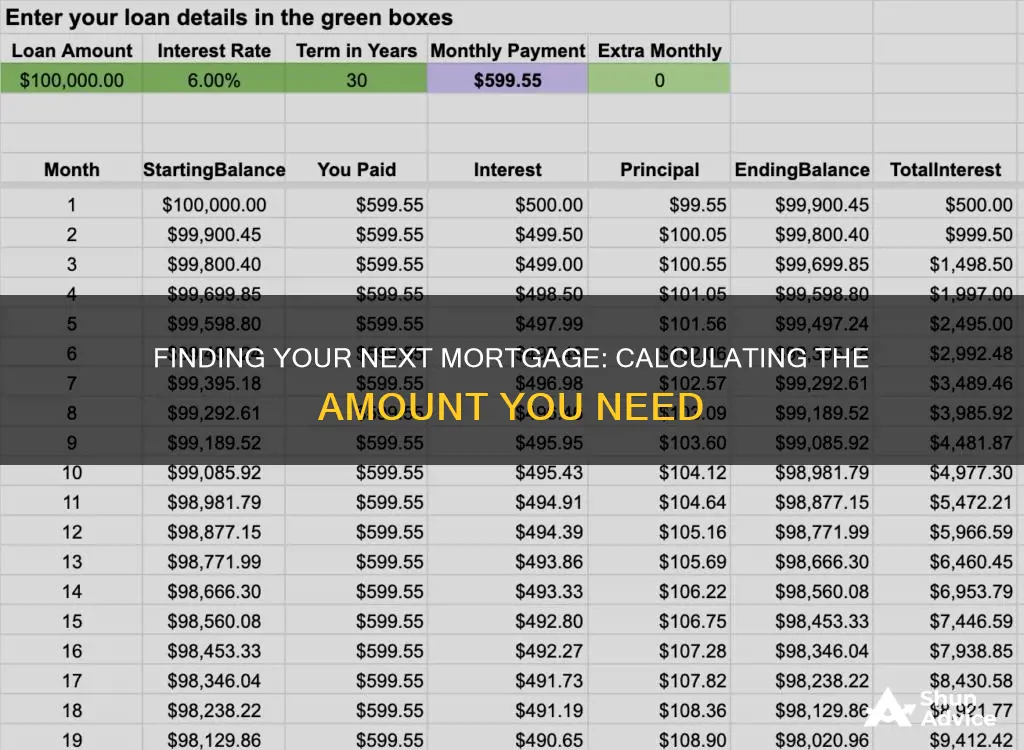

Using an amortization calculator

When taking out a mortgage, amortization refers to the process of paying off the loan over time through fixed monthly payments. An amortization calculator can be a useful tool for borrowers to understand how each payment affects their loan. It can also be used to calculate the monthly payment amount and determine the portion of each payment that goes towards interest.

To use an amortization calculator, you will need to input the following information about your loan:

- Loan amount: The amount of money you are borrowing for your mortgage.

- Loan term: The length of your loan, which could be 15 or 30 years, for example.

- Interest rate: The interest rate you are paying on your mortgage.

- Loan start date: The month when you made your first payment.

After entering this information, the amortization calculator will provide you with an amortization schedule, which is a table that details each periodic payment on the loan. The schedule will show how much of each payment is applied to interest and how much is applied to the principal (the amount borrowed) over the duration of the loan. It will also show the estimated balance that remains after each payment is made.

For example, let's say you take out a $20,000 loan with a 5% interest rate over five years. The amortization calculator will calculate that your fixed monthly payment will be $377.42 for the duration of the loan. In the first month, a portion of this payment will go towards interest, while the remaining portion will go towards the principal. As the loan progresses, the amount applied to interest will decrease, while the amount applied to the principal will increase.

It is important to note that the amortization calculator provides an estimate and may not include all costs associated with the loan. For example, it may not consider mortgage closing costs, loan fees, or variable rates that come with adjustable-rate mortgages. Therefore, borrowers should carefully review the loan agreement and consider all associated costs before making a decision.

Comparing Your Mortgage: How Does it Stack Up?

You may want to see also

![]()

Estimating how much house you can afford

Understanding the Components of a Mortgage

Before estimating your budget, it's helpful to understand the components that make up a mortgage. A mortgage is a loan secured by the property you intend to purchase. It typically includes the following key elements:

- Loan amount: This is the amount you borrow from a lender or bank. It is the purchase price of the property minus any down payment you make.

- Down payment: This is the upfront payment you make towards the purchase. It is usually a percentage of the total price, and it reduces the amount you need to borrow.

- Interest rate: This is the percentage of the loan amount that the lender charges you for borrowing the money. A lower interest rate can significantly reduce your monthly payments.

- Loan term: The loan term is the number of years over which you agree to repay the loan, typically 15 or 30 years.

Calculating How Much You Can Afford

When estimating how much house you can afford, it's essential to consider your financial situation holistically. This includes factors such as your income, existing debts, credit score, and savings goals. A good rule of thumb is the 28/36 rule, which suggests that your housing costs should not exceed 28% of your gross monthly income, and your total debt, including housing costs, should not exceed 36% of your gross monthly income.

Using Mortgage Calculators

To get a more precise estimate, you can use mortgage calculators offered by various financial institutions and real estate platforms. These calculators consider multiple factors, including your income, down payment, monthly debts, interest rates, loan terms, and property taxes. Here are some popular mortgage calculators you can use:

- Zillow's Affordability Calculator: This calculator allows you to estimate a comfortable mortgage amount based on your income, down payment, and monthly debts. It also provides advanced filters to include property taxes, homeowner's insurance, and HOA dues.

- Bankrate's Mortgage Calculator: This calculator helps you determine your budget by estimating monthly payments, including homeowners insurance premiums and property taxes. It also allows you to compare different loan terms.

- NerdWallet's Mortgage Calculator: This calculator helps you estimate your monthly mortgage payments, annual amortization, and total loan payments based on the loan amount, interest rate, and loan term.

- Chase's Mortgage Affordability Calculator: This calculator provides a rough estimate of your potential budget by considering your income, expenses, interest rate, and loan term.

- Redfin's Home Affordability Calculator: This calculator estimates how much home you can afford by taking into account your annual income, savings for a down payment, monthly debts or spending, and where you live. It also offers advanced filters to include homeowners insurance, mortgage interest rate, and property tax rate.

Considering Upfront Costs and Closing Costs

Remember that buying a home involves more than just the mortgage. There are upfront costs such as earnest money, closing costs, and home inspection fees. Closing costs can include attorney fees, title service costs, recording fees, property transfer taxes, and more. These costs can quickly add up, so it's important to factor them into your budget.

In summary, estimating how much house you can afford involves considering your financial situation, using mortgage calculators, and being mindful of the upfront and closing costs associated with the home-buying process. By following these steps, you can make a well-informed decision about one of the most significant purchases in your life.

Navy Federal: Your Mortgage Journey Companion

You may want to see also

![]()

Understanding the components of a mortgage

The main factors that determine your monthly mortgage payments are the size and term of the loan. The size of the loan is the amount of money you borrow, and the term is the length of time you have to pay it back. Generally, a longer term means a lower monthly payment, which is why 30-year mortgages are the most common. However, with a longer term, you will pay more interest over time.

There are several components that make up your monthly mortgage payment. These include:

- Principal: This is the amount of money you borrow to buy a house, also known as the loan amount. You pay off the principal over the term of your loan.

- Interest: This is the cost of borrowing money from your lender, usually a percentage of the amount borrowed. The interest is determined by the interest rate and the loan balance and term.

- Taxes: Your mortgage payments may include property taxes, also known as real estate taxes. These are assessments collected by your local government.

- Insurance: You may be required to have mortgage insurance, also known as private mortgage insurance (PMI). This is necessary if your down payment is less than 20%. Additionally, you will need to consider homeowners insurance, which protects both you and your lender from damage to the structure of the house and liability issues.

- Escrow: An escrow account is a reserve set aside to pay for property taxes and insurance premiums. Regularly scheduled escrow payments can help eliminate the burden of large annual payments.

- HOA fees: If you live in a planned neighbourhood or condo community, you may need to pay homeowners association (HOA) fees. These dues are used for the maintenance of common areas.

It's important to note that your monthly mortgage payment may also include other costs, such as attorney fees, title service costs, recording fees, and more. Using a mortgage calculator can help you estimate your monthly payments and understand the impact of each component.

The Wait for Mortgage Underwriting: How Long Till Approval?

You may want to see also

Frequently asked questions

You can calculate your new mortgage amount by using a mortgage calculator. You will need to input the loan amount, interest rate, loan term, and down payment. You can also factor in other monthly housing costs, such as homeowners insurance, property taxes, and private mortgage insurance (PMI), to get a more accurate estimate.

A monthly mortgage payment typically includes the principal, interest, property taxes, and insurance, also known as PITI. The principal is the original amount borrowed, while the interest is the cost of borrowing. Property taxes are assessed by the local government and are usually charged annually and divided into monthly amounts. Homeowners insurance protects against damage or loss to the property.

A fixed-rate mortgage has an interest rate that remains the same for the entire loan term, while an adjustable-rate mortgage (ARM) has a fixed interest rate for a predetermined length of time, typically the first few years, after which it adjusts to a new interest rate at scheduled intervals.

There are several other costs associated with a mortgage, including closing costs, initial renovations, and miscellaneous expenses such as new furniture or appliances. Closing costs can include attorney fees, title service costs, recording fees, survey fees, property transfer taxes, and more. These costs typically fall on the buyer but can sometimes be negotiated with the seller or lender.