The 2008 financial crisis was one of the worst economic downturns since the Great Depression. It was caused by a combination of factors, including the rise of subprime lending, housing speculation, and predatory lending practices. The crisis led to significant changes in the mortgage industry, with new regulations and guidelines aimed at stabilizing the economy and restoring trust in lending institutions. These changes have raised the bar for potential homeowners, with stricter requirements for credit scores, employment history, and debt-to-income ratios. The Dodd-Frank Act, which includes the Mortgage Act and the Consumer Financial Protection Act, has introduced banking regulations and created a Consumer Financial Protection Bureau to guard against predatory lending. Today's housing market is characterized by consumers with good payment histories and lower default risks, resulting in more comfortable lenders offering lower interest rates.

| Characteristics | Values |

|---|---|

| Regulatory changes | The US government introduced new regulations and guidelines to stabilise the economy and restore faith in the mortgage industry and lending institutions. |

| Stricter lending requirements | Borrowers now need to meet minimum credit scores, provide employment history, and adhere to debt-to-income ratio limitations. |

| Better-informed loan originators | Loan originators must complete a 20-hour mortgage education course, pass an ethical lending exam, and take continuing education courses to stay up-to-date with legal and guideline changes. |

| Higher standards for potential homeowners | Today's housing market favours consumers with a good payment history and a lower chance of defaulting on their debts. |

| Lower interest rates for low-risk borrowers | Mortgage industry regulators offer lower interest rates to those with a good credit history, while higher-risk consumers obtain loans with higher interest rates. |

| Increased supply and demand | There is now less supply and higher demand for housing, with more jobs available, making it possible for people to take on multiple jobs to pay their mortgages. |

| Subprime mortgage crisis | The collapse of several major financial institutions, including Lehman Brothers, and the failure of the PLS market, led to a severe global recession. |

| Reduced oversight and risk-taking | Regulatory and legal changes reduced oversight and encouraged risk-taking in the financial industry, with a significant increase in consumer debt. |

What You'll Learn

- The US government introduced new regulations and guidelines to stabilise the economy

- The Dodd-Frank Act introduced new banking regulations and created the Consumer Financial Protection Bureau

- The subprime mortgage crisis was a critical moment in US mortgage history

- The housing market stalled and interest rates rose, leading to the 2008 financial crisis

- The global recession of 2007-2009 influenced the current real estate environment

![]()

The US government introduced new regulations and guidelines to stabilise the economy

The US government's intervention reshaped the financial industry, with the Dodd-Frank Act bringing the most significant changes to financial regulation since the Great Depression. The Consumer Financial Protection Bureau was established to guard against predatory lending practices, which were a significant catalyst of the 2008 crisis. The "Volcker Rule" was also implemented, limiting banks' ability to make risky investments with customer deposits.

Loan originators are now required to undergo a 20-hour mortgage education course and pass an exam covering compliant and ethical mortgage lending. They must also take continuing education courses to stay up-to-date with any legal and regulatory changes. These tighter restrictions have increased the requirements for consumers seeking mortgages, who must now meet minimum credit score requirements, provide employment history, and adhere to debt-to-income ratio limitations.

The 2008 financial crisis was caused by a combination of factors, including the rise of subprime lending, increased housing speculation, and the failure of the PLS market. The crisis led to the collapse of major financial institutions, including Lehman Brothers, and a severe global recession. The US government's introduction of new regulations and guidelines was aimed at stabilising the economy, restoring faith in the mortgage industry, and preventing a similar crisis from occurring in the future.

Understanding Mortgages in 1031 Exchanges: What You Need to Know

You may want to see also

![]()

The Dodd-Frank Act introduced new banking regulations and created the Consumer Financial Protection Bureau

The 2008 financial crisis was caused by years of risky financial practices, including the growth of predatory mortgage lending, unregulated markets, and a massive amount of consumer debt. In response, the US government introduced the Dodd-Frank Act, which brought about the most significant changes to financial regulation since the Great Depression.

The Dodd-Frank Act also introduced the "Volcker Rule," limiting banks' ability to make risky investments with customer deposits. Banks now face stricter oversight and must undergo regular "stress tests" to prove they could survive economic shocks. Mortgage lenders must also verify borrowers' ability to repay loans. The Act also increased regulation of credit rating agencies, which has negatively impacted the financing and investment of firms worried about their credit ratings.

The Dodd-Frank Act has been subject to criticism, with some arguing that it could harm the competitiveness of US firms relative to their foreign counterparts. There are also concerns that its regulatory compliance requirements unduly burden community banks and smaller financial institutions. However, the Act has been defended as a necessary measure to prevent future economic crises and protect consumers from abuses that contributed to the 2008 crisis.

When to Apply for a Pre-Approval Mortgage

You may want to see also

![]()

The subprime mortgage crisis was a critical moment in US mortgage history

In the early to mid-2000s, high-risk mortgages became widely available, with lenders funding these mortgages by pooling and selling them to investors. This enabled more first-time homebuyers to obtain mortgages, increasing demand and driving up house prices. However, when house prices peaked, many borrowers could no longer afford their mortgage payments, leading to rising mortgage loss rates for lenders and investors.

The collapse of subprime lending caused a downward spiral in house prices, hurting the overall economy. It reduced construction, lowered wealth and consumer spending, impaired the ability of financial firms to lend, and decreased their ability to raise funds from securities markets. The crisis also led to the failure of several major financial institutions, including the bankruptcy of Lehman Brothers in September 2008, and disrupted the flow of credit to businesses and consumers.

In response to the crisis, the government introduced significant changes to financial regulation, including the Dodd-Frank Act, which created the Consumer Financial Protection Bureau to guard against predatory lending practices and required banks to maintain larger cash reserves. These regulatory changes aimed to protect against the risky financial practices that had led to the crisis and to ensure the stability of the financial system.

The True Cost of a Mortgage

You may want to see also

![]()

The housing market stalled and interest rates rose, leading to the 2008 financial crisis

The 2008 financial crisis was the result of a combination of factors, including regulatory and legal changes, risky financial practices, and the state of the housing market. In the years leading up to the crisis, the housing market experienced a significant boom, with home prices rising at an unprecedented scale. This was fuelled by several factors, including the increased availability of credit, government policies aimed at expanding homeownership, and speculation by home buyers.

However, when the housing market stalled and interest rates rose, the market became unstable. The rise in interest rates meant that borrowers were facing higher mortgage payments, which many could not afford. This led to an increase in foreclosure rates, as borrowers defaulted on their mortgages. The number of new homes sold in 2007 was 26.4% less than the previous year, and by January 2008, the inventory of unsold new homes was at its highest level since 1981.

The financial crisis was also caused by the collapse of several major financial institutions, such as Lehman Brothers, and the failure of the PLS market. The crisis was further exacerbated by the reduced oversight and increased risk-taking in the financial industry. The regulatory changes made it easier for investment banks to increase their debt and fuel the growth of mortgage-backed securities, supporting subprime mortgages.

The US government responded to the crisis by introducing new regulations and guidelines for the mortgage industry, aiming to stabilize the economy and restore faith in lending institutions. These regulations included stricter requirements for borrowers, such as minimum credit scores, employment history, and debt-to-income ratio limitations. The government also implemented changes to financial regulation, such as the creation of the Consumer Financial Protection Bureau and the implementation of the "Volcker Rule," limiting banks' ability to make risky investments.

Understanding the Mortgage Process: A Step-by-Step Guide

You may want to see also

![]()

The global recession of 2007-2009 influenced the current real estate environment

The global recession of 2007–2009 significantly influenced the current real estate environment. The recession was caused by a combination of factors, including the rise of predatory lending, the marketing of exotic financial products to consumers, and the failure of the PLS market. The US gross domestic product fell by 4.3%, making it the deepest and longest recession since World War II. The unemployment rate more than doubled, and the financial crisis led to a contraction in the economy, with the Federal Reserve taking various measures to mitigate the impact.

In response to the recession, the US government implemented new regulations and guidelines for the mortgage industry to stabilise the economy and restore trust in lending institutions. These regulations transformed the industry, introducing minimum credit score requirements, employment history checks, and debt-to-income ratio limitations for borrowers. Loan originators were mandated to complete a 20-hour mortgage education course and pass an ethical lending exam, ensuring they were well-informed and acted in the best interests of their clients.

The recession also led to a decline in home prices, which contributed to the financial crisis. Home prices fell by over 20% on average across the nation between 2007 and 2011, creating uncertainty for investors in mortgage-related assets. This decline in home prices and the subsequent increase in foreclosure rates resulted in a higher inventory of houses for sale, further impacting the real estate market.

The impact of the global recession on the real estate environment was profound and led to a higher standard for potential homeowners. Today's housing market favours consumers with a good payment history and a lower risk of defaulting on their debts. As a result, mortgage lenders feel more confident offering lower interest rates to these borrowers, while higher-risk consumers typically obtain loans with higher interest rates. The tightened lending standards and the shift towards lower-risk mortgage products have contributed to a more stable real estate environment.

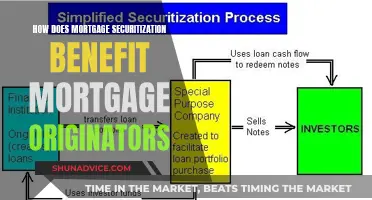

Mortgage Securitization: Benefits for Originators and the Market

You may want to see also

Frequently asked questions

The 2008 mortgage crisis was caused by a combination of factors, including predatory lending practices, government policies aimed at expanding homeownership, speculation by home buyers, and reduced lending standards. The crisis was also fueled by a massive amount of consumer debt and the creation of "toxic" assets.

The 2008 crisis had a significant impact on the mortgage industry, leading to a loss of more than $2 trillion from the global economy. It triggered a severe global recession, with the US home mortgage debt relative to GDP increasing from 46% in the 1990s to 73% in 2008. The crisis also resulted in new regulations and guidelines for the mortgage industry, including tighter lending standards and increased oversight of financial institutions.

Since the 2008 crisis, the mortgage industry has undergone significant changes to restore trust in lending institutions. These include stricter requirements for borrowers, such as minimum credit scores, employment history, and debt-to-income ratio limitations. Mortgage originators now need to complete extensive training and education to advise borrowers effectively and ethically. Overall, these changes have made obtaining a mortgage more challenging, with higher standards for potential homeowners.