Understanding how and when to calculate mortgage payoff is essential for several reasons. It can help you determine when you'll become mortgage-free and plan for your future financial goals. It can also help you assess the impact of making extra payments or refinancing your mortgage. A payoff statement, or payoff letter/quote, is a document that details the exact amount of money needed to fully pay off your mortgage loan. This amount is based on the principal, the interest rate, the number of payments made, and the number of payments remaining.

| Characteristics | Values |

|---|---|

| Determining factors | Type of loan, terms of the loan, options exercised by the borrower |

| Calculation | Based on principal, interest rate, number of payments made, and number of payments remaining |

| Payoff amount | Higher than the remaining balance on the home |

| Interest | Accrues in arrears |

| Payoff statement | A document detailing the exact amount of money needed to pay off the loan in full |

| Payoff statement usage | Useful for borrowers to request to understand the exact amount needed to pay off the home |

| Payoff statement request | Provided by the lender within 7 business days of the initial request |

| Online calculators | Help evaluate options to pay off a mortgage earlier, such as extra payments, bi-weekly payments, or paying back altogether |

What You'll Learn

![]()

Calculating the payoff amount

The payoff amount is the total amount that you will pay before your mortgage and all the interest is completely paid off. It is important to note that the payoff amount is generally higher than the remaining balance. This is because the payoff amount includes not only the outstanding balance but also any interest payments that you may owe and potential fees that your lender might charge.

The method for precisely determining the payoff amount will vary depending on factors like the type of loan, its terms, and the options exercised by the borrower. However, there is a standard formula used for calculating the loan payoff amount of a mortgage based on the principal, the interest rate, the number of payments made, and the number of payments remaining.

The principal is the amount borrowed, while the interest is the cost of borrowing the money. The principal amount is straightforward to calculate. It is the original loan amount minus any payments made towards the principal. For example, if you borrowed $300,000 and have paid off $50,000, your current principal balance is $250,000.

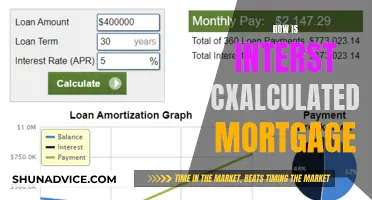

Calculating the interest amount is more complex. It depends on factors such as the interest rate, loan term, and remaining balance. To simplify the process, you can use an online mortgage calculator or consult your lender for an amortization schedule.

Additionally, you can use a mortgage payoff calculator to evaluate options to pay off your mortgage earlier, such as extra payments, bi-weekly payments, or paying back the loan altogether. These calculators can help you estimate how much money you can save in interest by making extra payments.

Understanding Mortgage Equity: Calculating Your Home's Value

You may want to see also

![]()

Principal and interest amounts

The principal is the amount borrowed, while the interest is the cost of borrowing the money. The interest rate on a mortgage has a direct impact on the size of a mortgage payment: higher interest rates mean higher mortgage payments.

The principal amount is straightforward to calculate. It's the original loan amount minus any payments made towards the principal. For example, if you borrowed $300,000 and have paid off $50,000, your current principal balance is $250,000. Calculating the interest amount is a bit more complex. It depends on factors such as the interest rate, loan term, and remaining balance.

At the beginning of a mortgage term, you owe more interest because your loan balance is high. Most of your monthly payment is applied to the interest you owe, and the remainder is applied to paying off the principal. Over time, as you pay down the principal, you owe less interest each month because your loan balance is lower. This means that over time, more of your monthly payment goes to paying down the principal.

There are several ways to reduce the principal and interest amounts. One way is to make extra payments towards the principal. This can be done biweekly, with your monthly payment, once a year, or whenever you have extra funds. Another option is mortgage recasting, which involves paying a lump sum towards the principal, plus a fee. Making a larger down payment will also reduce the principal amount.

Mortgages: Better Options for a Better Future

You may want to see also

![]()

Making extra payments

First, it's important to understand the difference between the principal and the interest of your loan. The principal is the amount of money you borrowed, while the interest is the cost of borrowing the money, typically calculated as a percentage of the principal. When you make your regular mortgage payment, the accrued interest is paid first, and the rest goes towards the principal.

If you want to make extra payments, ensure that they are applied to your principal. Otherwise, the bank or mortgage company will automatically allocate the extra payment towards interest, which does not save you any money. By applying extra payments directly to the principal, you can reduce the amount of interest paid over time and shorten the term of your loan.

You can make extra payments at any time, but it's important to check with your lender about their specific rules and requirements. Some lenders may allow you to specify if the payment is a regular payment (part interest and part principal) or only towards the principal. Additionally, be sure to familiarize yourself with any overpayment penalties or prepayment penalties in your mortgage agreement.

Before making extra payments, consider your unique financial situation and evaluate if it makes sense for you. For example, it may be more beneficial to pay off existing high-interest debt, such as credit cards, first to reduce your overall interest costs.

You can use a mortgage payoff calculator to help you estimate the impact of making extra payments. These calculators can take into account factors such as the remaining loan term, original loan amount, interest rate, and monthly payments to determine how much sooner you can pay off your mortgage and how much you can save in interest.

Pension Mortgages: Repayment Strategies and Options

You may want to see also

![]()

Mortgage payoff statement

A mortgage payoff statement, also known as a payoff letter or quote, is a document that outlines the exact amount of money required to pay off a mortgage loan in full. It is provided by the lending institution and is necessary for the borrower to have a clear idea of how much they owe. The payoff amount includes the remaining principal balance, any accumulated interest, and additional fees or charges.

The interest on a mortgage accumulates daily, which means that the total payable amount changes from day to day. This is why a mortgage payoff statement is essential, as it provides a snapshot of the loan at a specific point in time. It will also include a "`good-through` date, after which additional interest will be due, and a new payoff statement will need to be requested.

The payoff statement is important for both the borrower and the lender. For the borrower, it helps them understand their financial situation and make plans for the future. It can also be used when consolidating or refinancing debt. For the lender, it ensures that all financial claims are addressed and paid in full.

Calculating the mortgage payoff amount can be complex, depending on factors such as the type of loan, its terms, and the options exercised by the borrower. There are online calculators available that can assist in determining the payoff amount, but it is always recommended to contact the lender to confirm the accuracy of the calculation.

Understanding Interest-Only Mortgage Amortization

You may want to see also

![]()

How to get a payoff quote

A payoff quote is an important document for homeowners to have as it shows the remaining balance on your mortgage loan, including the outstanding principal balance, accrued interest, late charges/fees, and any other amounts. It is essential to have a payoff quote as it helps you understand your current loan balance and determine when you'll become mortgage-free. This, in turn, helps you plan your financial future.

There are a few ways to get a payoff quote. Firstly, you can contact your mortgage lender and request a verbal payoff quote over the phone. This will give you a general estimate of the money you need to pay off your loan, but it won't be an official or legally binding quote. Secondly, you can request a payoff letter, which is a more reliable and official document. You can request this from your lender, and they will send it to you within seven business days. This letter will include the total amount you owe and the date that the amount is valid through. It will also provide instructions on how to make the payment.

You can also use an online mortgage payoff calculator to help you evaluate your options for paying off your mortgage earlier. These calculators can show you how making extra payments, bi-weekly payments, or paying back the loan altogether will impact the total amount you pay and the length of your loan.

It is important to note that the exact amount you need to pay off your mortgage will depend on the specific terms of your loan, so it is always a good idea to get an official payoff quote from your lender.

Understanding Mortgage and Debt: Key Differences Explained

You may want to see also

Frequently asked questions

A mortgage payoff statement is a document that details the exact amount of money that is needed to fully pay off your mortgage loan. It is important to have this document as it helps you get a better handle on the exact amount that you’ll owe on your loan.

To calculate your mortgage payoff, you first need to determine the principal and interest amounts. The principal is the amount borrowed, and the interest is the cost of borrowing the money. The principal amount is the original loan amount minus any payments made towards the principal. Calculating the interest amount depends on factors such as the interest rate, loan term, and remaining balance.

You can request a payoff statement from your lender or servicer. They are required to send it back within 7 business days of the initial request.

The payoff amount includes the payment of any interest owed through the day you intend to pay off your loan. It may also include other fees incurred that have not yet been paid.

You can pay off your mortgage early by making extra payments, bi-weekly payments, or paying back the loan altogether. Making extra payments on the principal balance will help you pay off your mortgage debt faster and save thousands of dollars in interest.