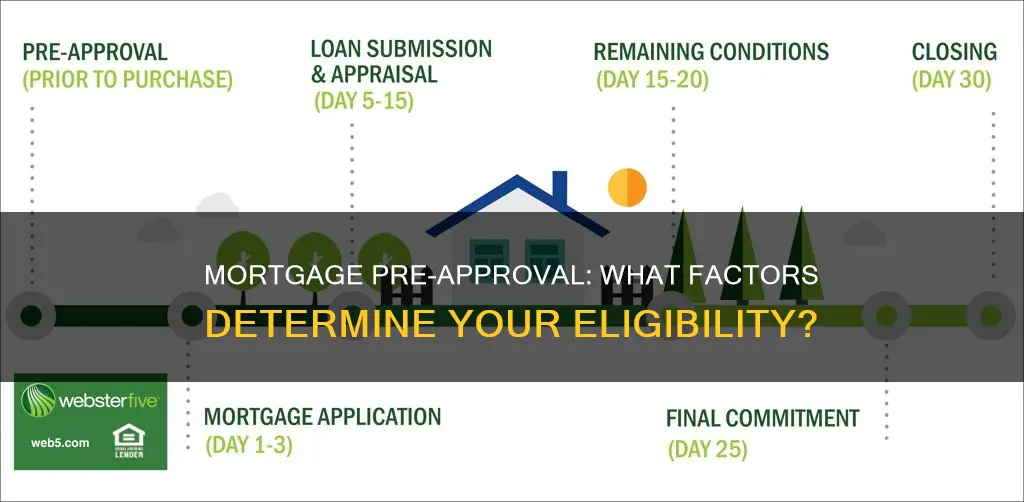

Getting a mortgage pre-approval is an important step in the home-buying process. It gives you an edge in a competitive market and helps you determine how much you can spend on a home. A mortgage pre-approval is a more thorough evaluation of your finances than pre-qualification. Lenders will conduct a hard credit inquiry and look at documentation such as proof of employment, income tax returns, debt-to-income ratio, and assets. They will then determine how much you can borrow and how much you could pay per month. If you are pre-approved, you will receive a pre-approval letter, which is an offer to lend you a specific amount, good for 90 days.

| Characteristics | Values |

|---|---|

| Purpose | To determine how much you can spend on a home |

| Requirements | Proof of income, employment, and assets; good credit score; strong employment history |

| Benefits | Shows sellers you're a serious buyer; puts you on the fast track to closing; gives you confidence in your search |

| Validity | Usually valid for 90 days, but can also be valid for 30 or 60 days |

What You'll Learn

![]()

Preapproval vs prequalification

Preapproval and prequalification are both types of mortgage approvals. They are steps that lenders take to verify that a client can afford a mortgage. However, there are some key differences between the two.

Prequalification

Prequalification is an early step in the homebuying journey. It is an informal evaluation of your finances, based on information you provide about your income, debt, assets, and credit history. Lenders will use this information to give you an estimate of what you might be able to borrow. It is important to note that the numbers provided by the borrower do not have to be accurate, and prequalification only gives a rough estimate. Prequalification can be completed quickly and conveniently online, in person, or over the phone. It is a good first step to help you fine-tune your budget and learn about different mortgage options.

Preapproval

Preapproval is a more official step that requires the lender to verify your financial information and credit history. It is a thorough look at your finances, where the lender will pull your credit history, verify your income, assets, and debts, and assess your financial situation. You will need to provide documentation such as W2s, recent pay stubs, bank statements, and tax returns. Based on this information, the lender will determine exactly how much you can be preapproved to borrow. Preapproval gives you a competitive edge over other buyers in the market and shows sellers that you are a serious buyer. It puts you on the fast track to closing and establishes your credibility as a homebuyer.

While prequalification and preapproval are sometimes used interchangeably, preapproval carries more weight and is considered more reliable by lenders, real estate agents, and sellers. Preapproval is an essential part of the journey to getting mortgage financing, while prequalification is an optional step. Preapproval is ideal if you know you are ready to buy a home and want to make an offer immediately.

Mortgage Data: Collection Methods and Sources

You may want to see also

![]()

Credit checks

Mortgage lenders will check your credit score when you start the pre-approval process for a home loan. This is known as a "hard pull", and it can negatively impact your credit score for a short time. It is a necessary part of applying for a mortgage and can't be avoided. However, it is important to note that within a 45-day window, multiple credit checks from mortgage lenders are recorded on your credit report as a single inquiry. This is because other lenders realize that you are only going to buy one home. Therefore, it is advisable to shop around and get multiple pre-approvals to find the best deal, as the impact on your credit score is the same, regardless of how many lenders you consult.

A credit check is a more specific estimate of what you could borrow from your lender. Lenders will pull your credit history, verify your income and assets, and assess your financial situation before giving you a mortgage pre-approval. They will also look at your debt-to-income ratio, with most lenders preferring that the result is no more than 43%.

It is important to check your credit report for errors before starting the mortgage pre-approval process, as errors can reduce your credit score. You can get a free copy of your credit report at annualcreditreport.com.

Factors That Influence Mortgage Rates and Payments

You may want to see also

![]()

Employment history

Lenders typically prefer a two-year history of steady employment, although shorter employment histories may be permitted for applicants with stable incomes or other positive factors. If you are self-employed, you will typically need to demonstrate a two-year job history, although this may be reduced to one year if you were previously employed in a similar field with a similar or greater income. In addition, self-employed applicants are usually required to provide business tax returns for two years unless the business is at least five years old.

Gaps in employment are not necessarily a deal-breaker, as lenders will take into account specific, valid reasons for time off work, such as maternity leave, finishing school, or temporary disability. However, lenders will be concerned about unemployment periods of six months or more, and you may need to provide explanations and documentation for these periods. Frequent job changes (more than three times in a year), a work history of only two years or less, and recent large fluctuations in income may also be red flags for lenders.

Mortgage Processors: Salary Insights and Payment Structure

You may want to see also

![]()

Debt-to-income ratio

Your debt-to-income ratio, or DTI, is a critical factor in determining your eligibility for a mortgage pre-approval. It compares your monthly debt payments to your monthly income, indicating how much of your income is dedicated to debt repayment. Lenders use this ratio to assess your ability to take on additional debt, such as a mortgage loan.

Calculating your debt-to-income ratio involves dividing your total monthly debt payments by your monthly pretax income. The result is expressed as a percentage. Lenders typically consider two types of DTI ratios: the front-end or housing ratio, which focuses solely on housing expenses; and the back-end ratio, which includes all types of debt, such as credit card payments, auto loans, and student loans.

Lenders generally prefer a lower DTI, indicating that less of your income is committed to debt repayment. While the ideal maximum DTI varies among lenders, it typically ranges from 36% to 43% for the back-end ratio. A DTI exceeding the lender's guidelines may lead to higher interest rates or less favourable loan terms.

To improve your debt-to-income ratio, you can employ various strategies, such as paying off existing debt, increasing your income, or opting for a less expensive home. Additionally, consolidating debt, making extra payments, and focusing on high-interest loans can help lower your DTI.

It's important to note that while your DTI is crucial, it doesn't consider all your expenses. Factors like food, health insurance, utilities, and entertainment are not included in the calculation. Therefore, when determining your ability to afford a mortgage, it's essential to consider your overall budget and financial goals, not just your DTI.

BBVA's Mortgage Services in Arizona: Pros and Cons

You may want to see also

![]()

Finalising preapproval

You will need to fill out a mortgage application and the lender will verify the information you provide. They will also perform a credit check. If you are preapproved, you will receive a preapproval letter, which is an offer to lend you a specific amount, good for 90 days. This is not a guarantee that you will get a mortgage, but it does show sellers that you are a serious buyer.

Before finalising a purchase, you should also order a home inspection to make sure the home’s components are in good working order and meet the loan program’s requirements. You should also hire a home appraiser to verify the home’s value and order a title report to make sure your title is clear of liens or issues with past owners.

Mortgage Reserves: Critical for Home Loan Approval and Peace

You may want to see also

Frequently asked questions

Pre-qualification is an optional, informal, and quick process that gives a rough estimate of how much you may be able to borrow for a home loan. It is based on information provided by the applicant about their finances, without verification. Pre-approval, on the other hand, is a more formal, detailed, and thorough evaluation of your finances, including a hard credit check. It gives a more specific estimate of the amount you can borrow.

Mortgage pre-approval gives you an edge in a competitive market. It shows sellers that you are a serious buyer with your finances in check and that you are likely to qualify for a loan. It also gives you confidence in your home search, as you know how much mortgage you can afford.

You will need to provide documents such as proof of employment, income tax returns, bank statements, and assets. You may also need to provide details of your debts and expenses.