There is no one-size-fits-all answer to the question of how many investment portfolios an individual should have. The number of portfolios depends on several factors, including risk tolerance, investment goals, time horizon, and personal financial situation. Some experts recommend having a separate portfolio for each investment goal to ensure a more balanced approach to saving for the future. This strategy provides a clear direction for investments and helps individuals stay focused and motivated. However, others argue that managing multiple portfolios can be complicated, and a single portfolio for all goals may be more manageable for some individuals. Ultimately, the decision comes down to personal preferences and financial circumstances.

| Characteristics | Values |

|---|---|

| Number of investment portfolios | There is no consensus on the ideal number of investment portfolios an individual should have. It depends on factors such as investment goals, risk tolerance, time horizon, and investment amount. Some sources recommend having a separate portfolio for each investment goal to ensure more balanced saving for the future. |

| Number of stocks in a portfolio | The number of stocks in a portfolio depends on factors such as investment goals, risk tolerance, diversification, and investment amount. A diversified portfolio typically holds between 10 and 30 stocks across various sectors and industries to minimise risk. |

| Types of investments | A portfolio can include a variety of assets such as stocks, bonds, mutual funds, exchange-traded funds (ETFs), and other financial instruments. |

| Risk tolerance | Risk tolerance refers to an investor's ability to accept losses in pursuit of higher returns. It is influenced by factors such as time horizon, emotional response to market volatility, and investment goals. |

| Asset allocation | Asset allocation refers to the distribution of investments across different asset classes (e.g. stocks, bonds, cash). It is influenced by risk tolerance, investment goals, and time horizon. A common rule of thumb is to subtract the investor's age from 100 or 110 to determine the percentage of the portfolio allocated to stocks. |

| Rebalancing | Portfolios should be periodically rebalanced to maintain the desired asset allocation. This can be done by buying or selling assets or investing in different asset classes. Some portfolios, such as target-date funds, automatically rebalance over time. |

What You'll Learn

![]()

Diversification and risk reduction

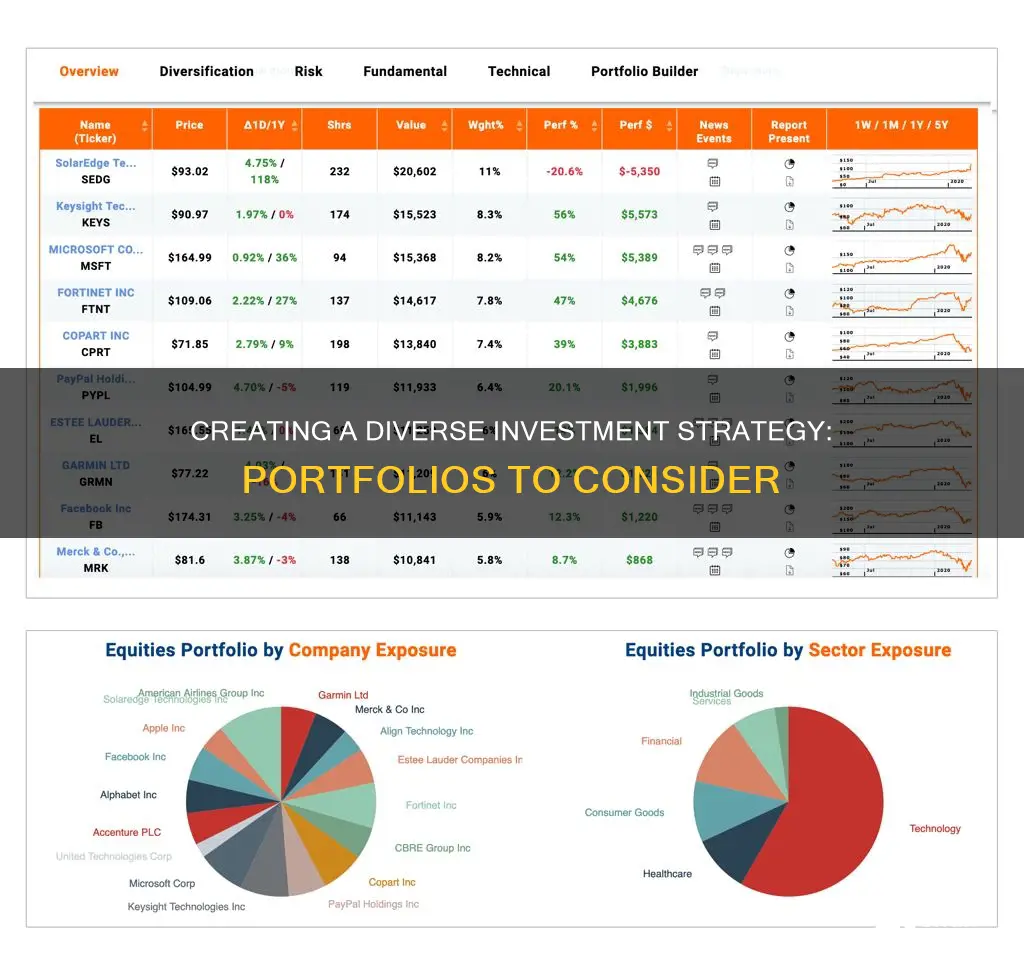

Diversification is a crucial strategy for managing investment risk and building long-term wealth. The idea is to spread your investments across different asset classes, industries, and geographic regions to reduce the overall risk of an investment portfolio. By holding a variety of investments, the poor performance of any one investment can potentially be offset by the better performance of another, leading to a more consistent overall return.

A well-diversified portfolio includes a mix of stocks, bonds, and potentially, alternative investments across various sectors, company sizes, and geographic regions. The right asset allocation depends on your individual risk tolerance, time horizon, and financial goals.

- Reducing Unsystematic Risk: Diversification helps to mitigate unsystematic or diversifiable risk, which is specific to a company, industry, market, economy, or country. By investing in a variety of assets, you reduce the impact of negative events affecting a particular company or industry.

- Stability and Volatility: Diversification can provide stability to your portfolio. While stocks offer higher expected returns over the long run, they can experience substantial short-term swings. High-quality bonds, on the other hand, tend to generate lower returns but provide stability. A mix of lower-risk and higher-risk assets allows for growth while providing a cushion against volatility.

- Correlation: Diversification taps into the concept of correlation, which shows how different investments move compared to one another. By combining investments that don't move in the same way (low correlation), you can protect your portfolio against extreme declines. For example, when stock prices fall, bond prices often rise, so owning both can reduce big swings in your portfolio's value.

- Different Asset Classes: Diversification involves investing in different asset classes beyond just equities. This includes bonds, commodities, real estate, and other alternative investments. Each asset class behaves differently based on macroeconomic conditions. For instance, rising interest rates may push down bond prices, but equity markets may still perform well due to a strong economy.

- Geographic Diversification: Investing in companies and holdings across different geographic locations is essential. Political, geopolitical, and international risks can impact specific regions, so diversifying globally can help manage these risks.

- Company and Industry Diversification: It's important to diversify across different companies and industries. Risk can be specific to a company, such as legislation, acts of nature, or consumer preference. Industry-specific risks, like a strike or negative news, can impact all companies in that sector. By diversifying across companies and industries, you reduce exposure to these risks.

- Time Frames: Consider diversifying across different time frames. Long-term investments often have higher inherent risk but may offer higher returns to compensate. Short-term investments are more liquid and yield lower returns.

- Avoid Over-Diversification: While diversification is essential, be careful not to over-diversify. Owning too many securities can dilute your returns and make it challenging to manage your portfolio effectively. It can also increase transaction fees and brokerage charges.

- Regular Rebalancing: Maintaining a diversified portfolio requires regular rebalancing. Over time, market movements can cause your asset allocation to drift from your intended strategy. Periodically rebalance your portfolio by shifting earnings into underperforming areas to maintain your desired asset mix.

- Risk Tolerance and Goals: The level of diversification and asset allocation should align with your risk tolerance and financial goals. Younger investors may opt for a more aggressive approach with a higher proportion of stocks, while older investors might favour a more conservative strategy with a larger allocation of bonds.

In conclusion, diversification is a powerful tool for reducing investment risk and enhancing long-term growth potential. By spreading your investments across various assets, industries, and regions, you can lower unsystematic risk, stabilise your portfolio, and potentially increase risk-adjusted returns. However, it's important to find the right balance and avoid over-diversification, ensuring your portfolio aligns with your risk tolerance and financial objectives.

Accessing Your ENT Investment Portfolio: A Step-by-Step Guide

You may want to see also

![]()

The number of stocks to hold

Firstly, it's important to understand the two primary risks associated with investing in stocks: market risk and company risk. Market risk, also known as systematic risk, is the possibility of losing money due to macroeconomic events unrelated to specific companies. Company risk, on the other hand, is the risk of losing money due to issues with a particular company.

To minimise company risk, it's advisable to hold a diverse range of stocks. If you hold only one stock and it performs poorly, you could lose a significant portion of your investment. However, if you hold a variety of stocks and one underperforms, the impact on your overall portfolio is reduced.

A portfolio of 10 or more stocks across various sectors or industries is generally considered much less risky than holding just a few stocks. The average diversified portfolio typically holds between 20 and 30 stocks, with some sources recommending a minimum of 25. This level of diversification effectively reduces unsystematic risk while maintaining expected returns.

However, it's important to note that too much diversification can be counterproductive. Holding too many stocks can make it challenging to achieve returns above market returns and may increase costs without significantly reducing risk.

The optimal number of stocks to hold depends on individual factors such as your country of residence, investment time horizon, market conditions, and how closely you follow financial news. Additionally, your risk tolerance and investment goals will influence the mix of stocks, bonds, and other assets in your portfolio.

If you're a novice investor, it's generally recommended to start with around 20 stocks, investing an equal amount in each. As you gain experience and conduct more thorough analysis, you may be able to reduce the number of stocks while still maintaining adequate diversification.

Ultimately, there is no magic number for the ideal number of stocks to hold. The key is to strike a balance between diversification and focus, ensuring you understand why you've invested in each stock while minimising exposure to company-specific risks.

Savings and Investments: Planning for Your Future

You may want to see also

![]()

Investment accounts

Number of Investment Accounts

The number of investment accounts or portfolios an individual should have is dependent on their specific needs and goals. While some financial experts suggest having multiple portfolios for different goals, others recommend a more simplified approach with a single portfolio. The appropriate strategy depends on various factors.

Benefits of Multiple Investment Accounts

Having separate portfolios for each investment goal provides a sense of direction and discipline to your investments. It ensures that your savings are aligned with specific objectives, such as a child's education, retirement, or purchasing a home. This approach helps prevent overdrawing funds for one goal at the expense of others. It also enables better tracking of progress and motivates you to stay on course.

Simplicity of a Single Investment Account

On the other hand, managing multiple portfolios can be more complicated and time-consuming. Consolidating investments into a single portfolio can make it easier to oversee and reduce the administrative burden. It may be more suitable for those who want a simplified approach without the hassle of managing multiple accounts.

Types of Investment Accounts

Regardless of the number of portfolios, it's important to choose the right type of investment accounts. There are several options available, including taxable brokerage accounts, retirement accounts such as IRAs, 401(k)s, and others. Each type of account has its own advantages and tax implications, so it's essential to understand them before deciding.

Diversification Within Investment Accounts

Diversification is a critical aspect of effective portfolio management. It involves spreading your investments across different asset classes, sectors, and geographies to reduce risk. A well-diversified portfolio can help minimize unsystematic risks associated with individual companies or industries. The general recommendation is to hold at least 10-15 stocks, with 20-30 being an ideal range for effective diversification.

Regular Rebalancing

Over time, the allocation of assets within your portfolio may deviate from your initial plan due to market performance. Therefore, it's important to periodically rebalance your portfolio to restore its original composition. This can be done by buying or selling assets to match your desired asset allocation.

In conclusion, the number of investment accounts an individual should have depends on their preference for focused goal-based investing or a simplified approach. Diversification and regular rebalancing are essential components of successful long-term investing, regardless of the number of portfolios.

Investment Strategies: University of Michigan's Portfolio Management

You may want to see also

![]()

Risk tolerance

There are three main levels of risk tolerance: aggressive, moderate, and conservative. Aggressive investors have a higher risk tolerance and are willing to risk more money for the possibility of better returns. They commonly invest in stocks and may have little to no allocation to bonds or cash. Younger investors often fall into this category as they have more time to recover from any market downturns.

Moderate investors seek to balance risk and return, typically investing in a mix of stocks and bonds. This strategy is suitable for those with medium-term investment goals.

Conservative investors have a lower risk tolerance and seek investments with guaranteed returns and little to no volatility. They often invest in less volatile assets such as bank certificates of deposit (CDs), money markets, or U.S. Treasuries. Retirees or those close to retirement age typically fall into this category as they may be unwilling to risk losing their principal investment.

It's important to note that risk tolerance can change over time and may be influenced by various factors, including age, investment goals, income, and personal comfort level. As investors age, they may become more conservative as they have less time to recover from market downturns. Additionally, those with a higher net worth and more liquid capital may have a greater risk tolerance, while those with limited financial resources may be more risk-averse.

To assess your risk tolerance, consider the following questions:

- What are your investment goals?

- What is your time horizon?

- How comfortable are you with short-term losses?

- Do you have non-invested savings?

- How closely do you plan to track your investments?

By understanding your risk tolerance, you can make informed decisions about the number and types of investment portfolios that align with your financial goals and comfort level with risk.

Viewing Your Acorns Investment Portfolio: A Simple Guide

You may want to see also

![]()

Asset allocation

Diversification

Diversification is a fundamental principle in investment portfolio management. By spreading your investments across different asset classes, industries, and geographic regions, you reduce the risk associated with any single investment or market segment. Diversification helps protect your portfolio from significant losses in the event of a company's failure or an industry's decline. It is recommended to hold at least 10-15 stocks in your long-term investment portfolio, with 20-30 being an ideal range for effective diversification and reduced investment risk.

Risk Tolerance

Your risk tolerance is a crucial factor in determining your asset allocation. It refers to your ability to withstand investment losses and accept higher-risk investments for potentially higher returns. Younger investors with a longer time horizon until retirement often have a higher risk tolerance and can allocate a larger portion of their portfolio to stocks. As you approach retirement, it is generally advisable to shift towards a more conservative approach, increasing the allocation of bonds and other fixed-income instruments.

Time Horizon

The time horizon for your investments plays a significant role in asset allocation. If you are investing for the long term, you can typically handle more volatility and allocate more towards stocks or aggressive growth strategies. In contrast, shorter-term goals may require a more conservative approach with a focus on capital preservation and lower-risk investments.

Regular Rebalancing

Over time, the performance of different investments in your portfolio can cause your original asset allocation to shift. Regular rebalancing involves adjusting your portfolio back to your desired allocation. This can be done by buying or selling certain assets or adjusting future contributions. Some investment vehicles, such as target-date funds, automatically rebalance over time.

Goal-Based Portfolios

Consider creating separate portfolios for different financial goals. This approach provides a clear sense of direction for your investments and helps ensure that you are saving adequately for each goal. It also allows you to tailor your asset allocation and investment strategies to the specific time horizon and risk profile associated with each goal.

In conclusion, effective asset allocation is a critical component of successful investment portfolio management. By considering factors such as diversification, risk tolerance, time horizon, and regular rebalancing, you can construct a portfolio that aligns with your financial goals and helps you make progress towards achieving them.

Social Security Investment Strategies: Maximizing Your Savings

You may want to see also

Frequently asked questions

There is no one-size-fits-all answer to this question. It depends on your financial goals, risk tolerance, and preferences. Some experts recommend having a separate portfolio for each investment goal to ensure more balanced saving for the future. This approach provides a sense of direction for your investments and helps you stay focused and motivated.

Having multiple investment portfolios can help you stay focused on your financial goals and ensure that your investments are aligned with your objectives. It also allows you to diversify your investments across different asset classes, sectors, and industries, reducing the risk associated with any single investment or market downturn. Additionally, separate portfolios can help you track your progress and make necessary adjustments to stay on course.

Managing multiple investment portfolios can be more complicated and time-consuming. It may also increase costs associated with trading and maintaining multiple accounts. Additionally, having too many portfolios can lead to over-diversification, diluting the potential returns and making it challenging to monitor and manage your investments effectively.

The ideal number of investment portfolios depends on your individual circumstances and goals. Consider your financial objectives, risk tolerance, time horizon, and the amount of time and effort you are willing to dedicate to managing your investments. Seek advice from financial planners or advisors to determine the right number and structure of portfolios for your needs.