If you're wondering how to invest your Thrift Savings Plan (TSP) after retiring, there are several options to consider. Firstly, you can keep your funds in the TSP and let them grow, especially if you're not sure what to do next. This option offers simplicity and allows your savings to benefit from compound interest. Alternatively, you can transfer your TSP to a Rollover IRA, providing more investment options and control. Another choice is to transfer your TSP to your new employer's 401(k) plan, reducing the number of retirement accounts to manage. You could also take a lump sum distribution, giving you full control, but this option may result in higher taxes and penalties. Finally, you can use your TSP to purchase an annuity, providing a guaranteed income for life, although this option has higher fees and limited flexibility. Each option has advantages and disadvantages, so it's essential to understand your choices and seek professional advice to make an informed decision.

| Characteristics | Values |

|---|---|

| What is TSP? | Thrift Savings Plan (TSP) is a retirement savings plan for federal employees. It is the government's version of a 401(k). |

| Contribution limit for 2024 | $23,000 |

| Additional contribution limit for people aged 50 or older | $7,500 |

| Contribution limit for active military members deployed in combat zones who receive tax-free income | $69,000 |

| Withdrawal before age 59 1/2 | 10% early withdrawal penalty |

| TSP balance required to keep the money in TSP after retirement | $200 |

| RMD age in 2033 | 75 |

| TSP rollover options | Rollover IRA, new employer's 401(k), lump sum distribution, annuity |

| TSP rollover methods | Direct, indirect |

What You'll Learn

![]()

Keep in TSP and let it grow

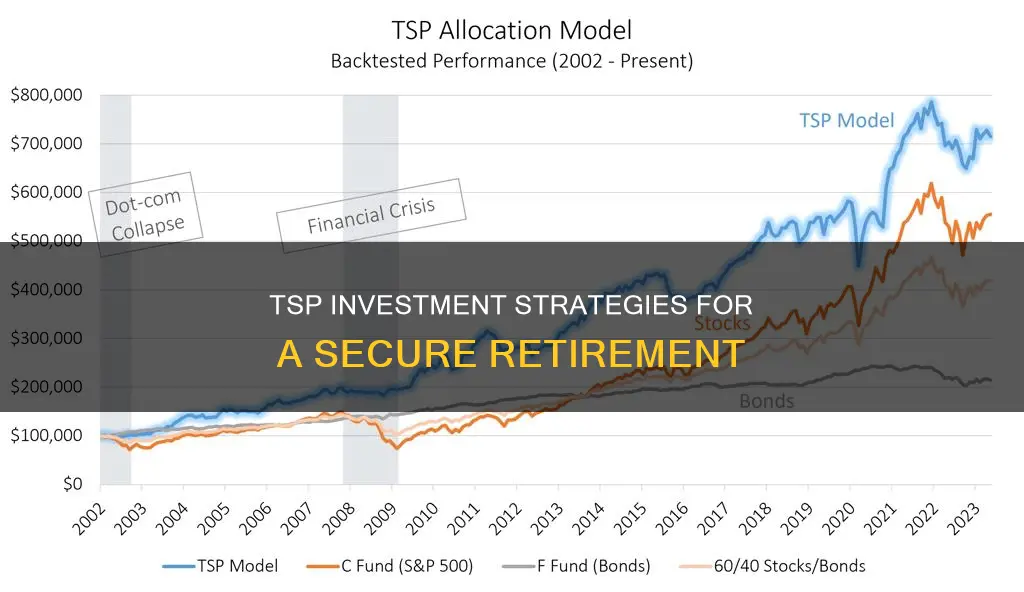

For those unfamiliar with the acronym, the TSP, or Thrift Savings Plan, is a retirement savings and investment plan for federal employees and members of the uniformed services, offering the same type of savings and tax benefits that many private corporations provide to their employees with 401(k) plans. After retiring, it can be tempting to withdraw all your funds from your TSP and spend them or invest them elsewhere. However, leaving your money in your TSP account and letting it continue to grow can be a wise decision for several reasons.

Firstly, the TSP offers extremely low expenses ratios, which means more of your money is working for you. The expenses ratios for TSP funds are typically lower than those of comparable mutual funds, and keeping your money in the TSP can result in significant savings over time. Additionally, the TSP offers a range of investment funds, providing diverse investment options to suit your risk tolerance and financial goals. From conservative options like the G Fund (Government Securities Investment Fund) to more aggressive choices like the C Fund (Common Stock Index Investment Fund), you can tailor your investment strategy within the TSP to match your needs.

Another advantage of keeping your money in the TSP is the potential for continued growth. Historically, the stock market has trended upward over time, and leaving your funds invested gives them the opportunity to benefit from long-term market gains. Even if you are no longer making contributions, compound interest can work its magic, and the longer your investments have time to grow, the larger your nest egg can become. Of course, past performance does not guarantee future results, and market fluctuations will occur, but historically, riding out the ups and downs has been rewarded with positive long-term returns.

Finally, managing your own investments can be time-consuming and complex, and the TSP simplifies this process. With the TSP, you don't need to worry about choosing individual stocks or bonds, and you benefit from professional investment management. The TSP's investment funds are managed by experienced professionals who carefully monitor the markets and adjust their strategies to maximize returns while managing risk. This means you can maintain a hands-off approach, avoiding the stress and potential costs of actively managing your own investments.

In summary, leaving your retirement savings in the TSP and letting it grow can be a smart financial strategy. The TSP offers low fees, diverse investment options, the potential for long-term growth, and professional investment management. Of course, everyone's situation is unique, and it's important to consider your own financial goals, risk tolerance, and other sources of retirement income when making decisions about your TSP funds. It is always a good idea to consult with a financial advisor to discuss your specific circumstances and determine the best course of action for your retirement savings.

Savings Woes: Firms' Investment Blues

You may want to see also

![]()

Transfer TSP to a Rollover IRA

Transferring your Thrift Savings Plan (TSP) to a Rollover IRA is a common option for retirees. Here is a detailed guide on how to do this:

Understanding the TSP and Rollover IRA

The TSP is a retirement savings plan for federal employees, similar to a 401(k). It offers tax advantages, such as tax-deferred growth or tax-free withdrawals in retirement. On the other hand, a Rollover IRA is an individual retirement account that allows you to transfer your retirement savings from an employer-sponsored plan, like the TSP.

Step 1: Evaluate Your Options

Before initiating a transfer, it's essential to understand the pros and cons of each option. You can keep your savings in the TSP, transfer to a new employer's plan (if allowed), roll over into an IRA, or cash out your balance. Each option has different tax implications and potential penalties. For example, cashing out your TSP before the age of 59 1/2 may result in an early withdrawal penalty of 10% on top of applicable taxes.

Step 2: Choose the Right Type of IRA

When rolling over your TSP to an IRA, you have two main options: a traditional IRA or a Roth IRA. If you choose a traditional IRA, ensure it has the same tax treatment as your TSP to avoid immediate tax liabilities. For instance, roll over a pre-tax TSP to a traditional IRA or contributions from a Roth TSP to a Roth IRA. Moving from a traditional TSP to a Roth IRA will trigger taxes on the converted amount.

Step 3: Open an IRA Account

After deciding on the type of IRA, it's time to choose a brokerage firm, such as Vanguard or Fidelity, and open an IRA account. This process should be straightforward and quick, usually taking less than 15 minutes.

Step 4: Initiate the Rollover

Contact the TSP administrator and your new IRA provider to initiate the rollover process. Follow their instructions carefully, as they may require specific paperwork and certifications. The new financial institution must accept a check from the U.S. Treasury and provide rollover information for your distribution request.

Step 5: Complete the Rollover

This step involves filling out the required paperwork, which may require coordination between the TSP and your new IRA provider. Once the paperwork is completed, the TSP will liquidate your account and issue a U.S. Treasury check to your new financial institution.

Important Considerations:

- Tax Consequences: Be mindful of potential tax liabilities when converting from a pre-tax TSP to a Roth IRA.

- Expense Ratios: TSP investment funds have low expense ratios, so consider the higher expenses associated with publicly traded funds in an IRA.

- Portfolio Management: You will need to make investment decisions for your IRA, so consider seeking advice from a financial advisor or using a robo-advisor.

- Fees and Expenses: Understand the fees and expenses associated with both the TSP and IRA options before making a decision.

- Investment Options: IRAs often offer a broader range of investment choices compared to the TSP, but may not have the same low-cost options.

Remember, it's important to carefully consider all your options and seek advice from a financial advisor to choose the best path for your retirement savings.

Retirement Plans: Navigating the Investment Danger Zone

You may want to see also

![]()

Transfer TSP to a new employer's 401(k) plan

Transferring your Thrift Savings Plan (TSP) to a new employer's 401(k) plan is a good option if the new plan has strong investment options and/or you want to reduce the number of retirement accounts you need to maintain.

Advantages

Your retirement assets will maintain their tax advantages, and there are no penalties or fees for transferring your money. You can borrow against your 401(k) if you want to, and you will minimise the number of retirement accounts you have.

Disadvantages

You are limited to your new plan's investment options, so this is important if your new 401(k) plan has limited investment choices or higher-than-average expense ratios, which cause lower returns. Some employers have a minimum waiting period before you can sign up for their retirement plan, so you may have to wait before you can roll over your TSP assets.

How to Transfer

Firstly, check with your 401(k) plan administrator to confirm that they accept TSP rollovers. Some plans may not accept rollovers. Once you have confirmed that your 401(k) plan allows TSP rollovers, you will need to log in to your TSP account and request a rollover. You can then choose a rollover method. It is recommended that you do a direct rollover, where the TSP will transfer the funds directly to your 401(k) plan administrator. This will ensure that you avoid any taxes and penalties. With an indirect rollover, you will incur income taxes and an early withdrawal penalty if you don't complete the transaction within 60 days of receiving the money.

Other Options

You could also keep your TSP account, roll your TSP assets into an IRA, withdraw your TSP assets in a lump sum, or transfer the assets to a qualified annuity.

Pay Down Mortgage or Invest in RRSP: Which is the Smarter Financial Move?

You may want to see also

![]()

Take a lump sum distribution

Taking a lump sum distribution from your Thrift Savings Plan (TSP) when you retire gives you complete control over your money. However, this option does come with consequences. If you take a lump sum, you will need to pay taxes on the entire amount in the year you receive it. This may push you into a higher tax bracket and result in a larger tax bill. Depending on the TSP amount, taxes and penalties might eat up a third or even half of your TSP.

You will be able to use your assets immediately and have full control over them. However, you will have to pay the huge tax payment and the 10% early withdrawal penalty, which will reduce your overall balance by a third to half, depending on your tax bracket. You will also lose tax deferral benefits and any potential earnings.

Lump Sum Distribution vs Pension Payments

Those approaching retirement and eligible for a pension often weigh up accepting the traditional, lifetime monthly payments or taking a lump-sum distribution. Monthly pension payments are a fixed dollar amount that begins at retirement and lasts until the retiree's death. Some plans offer a survivor's benefit for a living spouse. A lump-sum distribution, on the other hand, is a one-time cash disbursement at retirement. The retiree is solely responsible for managing the funds throughout retirement.

People who take a lump sum may outlive their money, while traditional pension payments continue until death. However, a lump-sum distribution allows individuals to spend or invest the money. A pension payment annuity is commonly a fixed payment, but a lump sum offers flexibility and, if invested properly, may also provide regular income.

How to Avoid Taxes on a Lump Sum Distribution

You can avoid taxes on a lump sum pension payout by rolling over the proceeds into an individual retirement account (IRA) or other eligible retirement accounts. However, even if you plan on rolling over your pension payout, some companies withhold 20% for potential federal tax liabilities. This occurs when the pension company sends you a check for your pension payout, and you only receive 80% of your lump-sum distribution. To avoid this, do not receive the payout directly. Instead, perform a direct rollover by requesting that the money be sent directly to your retirement account at the new investment company.

Debt-Free Investing: Why Paying Off Debts Unlocks Investment Opportunities

You may want to see also

![]()

Purchase an annuity

Annuities are insurance products that can guarantee a fixed income for life, eliminating the risk of outliving your retirement savings. They are highly customizable and can be purchased from insurance companies, brokerage firms, or banks. However, only life insurance companies can legally issue annuity contracts.

You make a premium payment to an insurance company, either as a lump sum or a series of payments, and in return, you receive regular income for a specified period, often for life. Annuities can be set up in various ways: you can collect payments for a set number of years or request guaranteed payments for life. You can also choose when to start receiving income, with immediate annuities paying out within a month of purchase, and deferred annuities delaying payments to allow your savings to grow.

Types of Annuities

There are several types of annuities, each with different levels of risk and return:

- Fixed annuities offer a guaranteed, fixed interest rate for a specified period, after which the contract pays a return based on market interest rates. They are considered the safest option as they are not tied to market performance, but their potential returns are lower.

- Variable annuities invest in market-based accounts such as mutual funds, so returns depend on the performance of these underlying investments. They offer higher potential returns but also carry the risk of losing part of your contributions if the investments perform poorly.

- Fixed index annuities offer a middle ground in terms of risk and return, with performance tied to a market-based fund but with a cap and floor on gains and losses.

Benefits of Annuities

- Guaranteed income: Annuities are the only financial product that can provide a guaranteed lifetime income, ensuring you never outlive your savings.

- Tax advantages: Earnings on deferred annuities are tax-deferred, and annuities purchased within a tax-advantaged retirement plan can further enhance these benefits.

- No contribution limits: Unlike other retirement savings vehicles such as 401(k)s and IRAs, deferred annuities have no limits on how much you can contribute.

- Customizable: Annuities can be tailored to your needs through optional add-ons or riders, providing additional benefits such as a death benefit or the ability to pass the annuity to heirs.

Considerations When Buying an Annuity

- Complexity and fees: Annuities can be complex financial products with various fees, including upfront commissions, annual fees, and surrender charges for early withdrawal. It is important to understand all the costs involved and how the annuity is structured.

- Inflation risk: While annuities provide a guaranteed income, this income may not keep pace with inflation. Inflation protection can be added at an additional cost, but it may not always be the best solution.

- Lock-in period: Annuities typically have a lock-in period during which you cannot withdraw your funds without incurring penalties.

- Limited flexibility: Once an annuity is purchased, it is usually final, and you may lose the ability to make large withdrawals.

Steps to Buying an Annuity

If you decide to purchase an annuity, here are the key steps to follow:

- Assess your financial situation and goals: Understand your current and future financial needs and how an annuity can help you achieve your goals. Consult a financial advisor if needed.

- Choose an annuity product: Select an annuity type that meets your needs and aligns with your goals, considering factors such as income, growth, and death benefits.

- Research annuity providers: Find companies with strong credit ratings that specialise in the type of annuity you want.

- Apply and sign the contract: Work with your chosen provider and financial advisor to apply for and customise the annuity contract to your needs.

- Fund the annuity: Transfer the money for the premium payment, considering the tax consequences of different payment types.

Annuities can provide peace of mind and a guaranteed income stream for retirees, but it is important to carefully consider the benefits and drawbacks before purchasing one.

The Debt-Equity Dilemma: Navigating the Payoff Crossroads

You may want to see also

Frequently asked questions

Keeping your TSP after retirement lets you take advantage of the low expenses of TSP funds and the wider range of investment options from the new TSP mutual fund window. You can also keep your TSP to let it grow, as you can leave the money in your TSP as long as your vested balance is at least $200.

By keeping your TSP, you cannot make any more contributions or take out any loans. It can also be a headache to manage lots of retirement plans and keep track of assets across platforms.

You can transfer your TSP to a Rollover IRA or to your new employer's 401(k) plan.