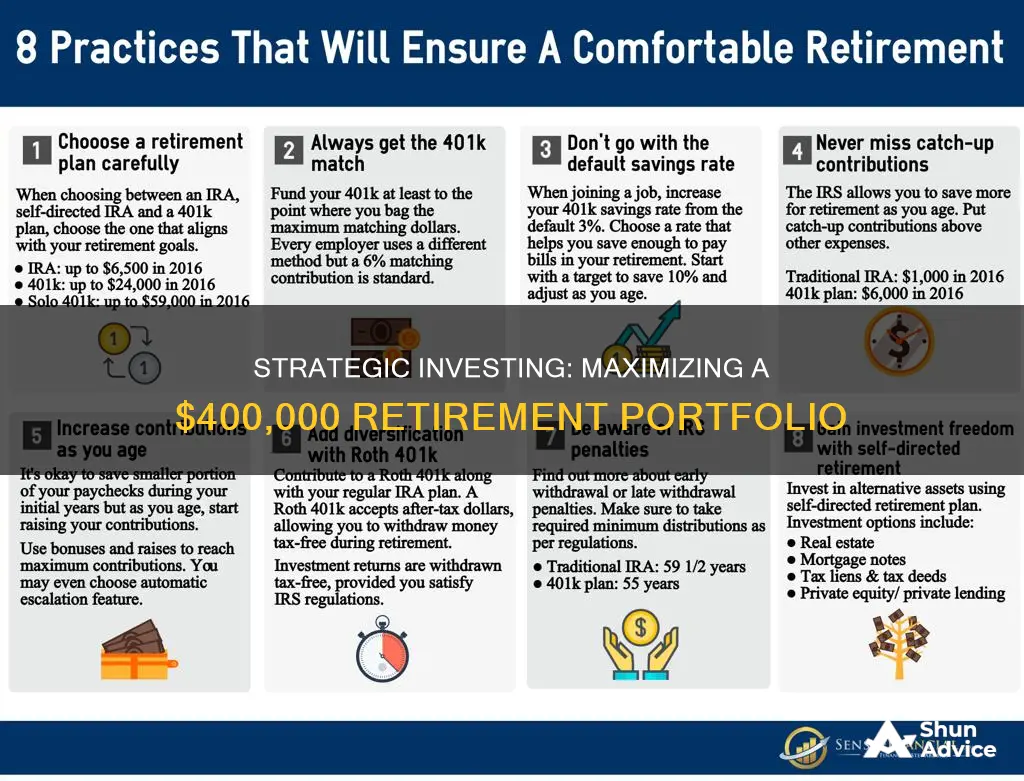

Investing a $400,000 retiree portfolio requires careful planning to ensure a comfortable retirement. The first step is to calculate retirement income and expenses, including Social Security payments, health care, and monthly bills. Next, consider the 4% rule, which suggests taking 4% of savings annually in retirement, adjusted for inflation. For a $400,000 portfolio, this equates to $20,000 in the first year. However, with the high cost of living, additional income sources like part-time work may be necessary.

To build a sustainable investment portfolio, diversification is key. This includes investing in stocks, bonds, real estate, and more. As retirement approaches, the focus should shift from aggressive growth investments to income and capital preservation, with a balanced approach across equity and fixed-income mutual funds. It is recommended to consult financial experts for advice tailored to individual needs and risk tolerance.

| Characteristics | Values |

|---|---|

| Age of retiree | 64 |

| Amount of money to invest | $400,000 |

| Recommended approach | Keep investing and believing in the economy |

| Recommended investment types | Dividend-paying stocks, dividend-growth funds, intermediate- to longer-term bond funds |

| Recommended allocation | 70% fixed income and 30% equities |

| Timeframe for investment | 12 to 18 months |

| Recommended action | Rebalance portfolio a few times a year |

What You'll Learn

![]()

Stocks, real estate, and other growth instruments

Stocks

Investing in the stock market involves purchasing shares of companies, which can be done through individual stocks or dividend stocks. While the stock market offers the potential for substantial growth, it also comes with high risk due to its volatile nature. Various interconnected factors can influence stock market performance, making it unpredictable for investors. Therefore, if capital preservation is your primary goal, the stock market may not align with your risk tolerance. Nonetheless, stocks remain an essential part of a well-diversified retirement portfolio, providing growth potential and a hedge against inflation.

Real Estate

Real estate investing typically involves buying rental properties or commercial real estate to generate cash flow from rental income. However, it is important to consider the impact of market unpredictability on this investment strategy. Factors like inflation, the job market, and geopolitics can affect both residential and commercial real estate values. Additionally, rental income is susceptible to vacancies, and real estate investing often requires a large initial investment, along with property management fees and taxes, which can diminish returns.

Other Growth Instruments

There are alternative growth instruments to consider for your retirement portfolio:

- High-yield savings accounts: While safer for conservative investors, these may not provide the passive income desired for investing in other instruments.

- Index funds: These mirror specific market benchmarks and offer diversification across various stocks or bonds. However, they are still susceptible to market volatility.

- Private equity: This involves investing directly in private companies, typically requiring a significant initial investment. While offering high return potential, it is also high risk, as your money may be tied up for years without guaranteed returns.

- Precious metals: Gold or silver can preserve capital, but their value fluctuates based on global demand, making capital preservation unpredictable.

- Mortgage note funds: These funds pool money from investors to purchase distressed mortgage notes and restructure payments, providing income through distributed returns. This option offers capital preservation and a consistent income stream.

Diversification and Risk Management

Diversification is a crucial aspect of building a robust retirement portfolio. It involves spreading your investments across different asset classes, markets, and locations to minimise risk. As you approach retirement age, actively managing your portfolio to reduce risk becomes essential. This may include shifting from aggressive growth investments to more conservative options, such as corporate bonds, preferred stock offerings, and moderate instruments with competitive returns and lower risk.

Additionally, consider your risk tolerance, which refers to your willingness to endure volatility in your investments. As you age, your risk tolerance may change, leading to a greater focus on capital preservation and income generation through fixed-income securities. Instruments like certificates of deposit, Treasury securities, and fixed and indexed annuities can provide guaranteed principal or income. However, a balanced portfolio should not become exclusively invested in guaranteed instruments until your 80s or 90s.

Building a Personal Investment Portfolio: Strategies for Success

You may want to see also

![]()

Risk tolerance and time horizon

When it comes to investing, risk tolerance and time horizon are key factors in determining your investment strategy. Risk tolerance refers to the amount of risk or volatility in the value of their investments that an investor is willing to accept. Time horizon, on the other hand, refers to the amount of time until you need the money you're investing. These two factors are crucial in deciding how to allocate your assets across different investment options.

As a retiree with a $400,000 portfolio, your risk tolerance and time horizon will play a significant role in shaping your investment decisions. Here are some important considerations:

Understanding Your Risk Tolerance

Risk tolerance is influenced by various factors, including age, financial situation, investment goals, and investment experience. As a retiree, your risk tolerance may be different from that of a younger investor. While age is a factor, it doesn't mean that you should automatically switch from stocks to less risky investments like bonds. With people living longer, you may still have a long time horizon and can remain an aggressive investor.

Your financial situation also plays a role in determining your risk tolerance. If you have a high net worth and more liquid capital, you may have a higher risk tolerance than someone with limited funds. Consider your savings, emergency funds, and stable income sources when assessing your risk capacity.

Evaluating Your Time Horizon

As a retiree, your time horizon is crucial in deciding how to allocate your $400,000 portfolio. If you have already retired, your time horizon may be shorter, and you might want to adopt a more conservative investment approach. However, if you have a long life expectancy or plan to work during retirement, your time horizon could be longer, allowing for a more aggressive investment strategy.

Asset Allocation and Diversification

Based on your risk tolerance and time horizon, you can determine the appropriate asset allocation for your portfolio. As a retiree, you may want to consider a mix of stocks, bonds, and short-term investments. Stocks can provide long-term growth potential, while bonds offer more stability. Diversification within asset classes is also essential to reduce risk. This includes investing in different company sizes, industry types, geographies, and bond maturities and risks.

Seeking Professional Advice

Determining your risk tolerance and time horizon can be complex, and it's crucial to get it right to prevent financial ruin. Consider working with a financial professional to assess your situation and complete an investor profile questionnaire. They can help you balance your willingness to take risks with your financial ability to withstand losses and create an investment plan that aligns with your goals.

In conclusion, as a retiree with a $400,000 portfolio, understanding your risk tolerance and time horizon is essential for making informed investment decisions. By considering these factors, you can allocate your assets appropriately, diversify your investments, and work towards achieving your financial goals during retirement. Remember to seek professional advice if needed to ensure your investment strategy aligns with your risk tolerance and time horizon.

Crafting a Diversified Portfolio with Fidelity Investments

You may want to see also

![]()

Active vs. passive portfolio management

Active portfolio management and passive portfolio management are two opposing strategies that investors can use to generate returns on their investment accounts. Active portfolio management involves a manager who tries to beat the performance of a given benchmark index by using their judgment in selecting individual securities and deciding when to buy and sell them. This strategy typically results in higher investment returns but also attracts higher transaction fees.

Proponents of active management believe that a skilled investment manager can generate returns that outperform a benchmark index by picking the right investments, taking advantage of market trends, and attempting to manage risk. For example, an active manager might attempt to earn better-than-market returns by overweighting certain industries or individual securities or by allocating more to conservative investments to control the portfolio's overall risk. An actively managed individual portfolio also allows the manager to consider tax implications, such as harvesting capital losses to offset capital gains.

On the other hand, passive portfolio management, also known as index fund management, attempts to match the performance of a benchmark index and minimize expenses. Advocates of passive investing argue that capturing overall market returns is best achieved through low-cost, market-tracking index investments. This approach is based on the efficient market concept, which states that since all investors have access to the same information about a company, it is challenging to gain an advantage over other investors. Therefore, reducing investment costs is the key to improving net returns.

Passive investing creates cost efficiencies by eliminating the need for research and reducing trading costs due to less frequent trading. Additionally, it often results in fewer capital gains distributions, leading to relative tax efficiency. Popular passive investment choices include index funds and exchange-traded funds (ETFs).

While active management aims for superior returns, it also entails greater risks and higher fees. In contrast, passive management focuses on minimizing costs and replicating a specific benchmark or index.

To achieve the best of both worlds, some investors blend the two approaches using the core/satellite strategy. This strategy involves investing the majority of funds in cost-efficient passive investments designed to track a specific benchmark, while the remaining funds are actively managed to boost returns and lower overall portfolio risk.

Investing in New York's 529: A College Savings Guide

You may want to see also

![]()

Retirement savings by age

Starting Early:

The power of compounding is your best friend when it comes to retirement savings. The earlier you start, the more time your savings have to grow. It's critical to begin saving for retirement as soon as possible, ideally in your 20s. This gives your money more time to compound and grow, helping you build a substantial nest egg over time.

Savings Benchmarks:

While every situation is unique, having savings benchmarks based on age can help you stay on track. Here are some general guidelines:

- By age 30, aim to save at least one time your current salary.

- By age 35, aim for one to one-and-a-half times your salary.

- By age 40, aim for three times your salary.

- By age 50, aim for six to eleven times your salary.

- By age 60, your savings goal should be eight to twelve times your salary.

- By age 67, Fidelity's guideline suggests saving ten times your pre-retirement income.

Investment Strategies:

When you're younger, focus on growth investments, such as stocks and equities. As you approach retirement age, gradually shift towards income and capital preservation. Diversification is essential at any age to maintain stable and reliable investment returns.

Adjustments and Reviews:

Life events, market uncertainty, and the rising cost of living can impact your savings plan. It's crucial to review your portfolio periodically and make adjustments as needed. Major life changes, such as paying off student loans, getting married, or having children, may require you to re-evaluate your savings strategy.

Retirement Income:

When planning for retirement, consider your expected income sources, such as Social Security benefits, pension plans, and any other investments. This will help you determine how much you need to save independently to maintain your desired lifestyle during retirement.

Remember, retirement savings depend on various factors, including your risk tolerance, financial goals, and life plans. It's always a good idea to consult a financial advisor for personalized advice and to ensure you're on the right track.

Graph Savings: A Smart Investment Strategy?

You may want to see also

![]()

Retirement income and outflows

Retirement income and expenditure planning is a critical aspect of retirement, and understanding your income sources and managing your outflows is essential to sustaining your retirement portfolio. A retiree with a portfolio of $400,000 has a substantial sum to generate retirement income, and there are several strategies to consider to make the most of this amount.

The first step is to understand your income sources. As a retiree, you may have several income streams, including Social Security benefits, pension plans, annuities, part-time work, or investments. It is important to understand the timing and amount of each income source to plan your cash flow effectively. For example, Social Security benefits can be claimed at different ages, and the amount received varies depending on when you start claiming. Similarly, pension plans may offer different payout options, and understanding the pros and cons of each can help you make an informed decision.

Next, you need to assess your essential and discretionary expenses. Essential expenses are your must-haves, such as housing, utilities, food, and healthcare. These are the costs that must be covered by your retirement income. Discretionary expenses are the nice-to-haves, like travel, entertainment, and gifts. By separating your expenses, you can prioritize your spending and ensure your essential needs are met first. It also helps you identify areas where you may be able to cut back if necessary.

Managing your investment portfolio is another key aspect of retirement income and outflows. A portfolio of $400,000 can provide a comfortable retirement income, but it needs to be managed wisely. A common rule of thumb is the 4% rule, which suggests that you can safely withdraw 4% of your portfolio value each year for retirement income, adjusting the amount for inflation. This rule aims to balance between preserving your capital and providing a sustainable income. However, it is important to note that this rule may not apply to everyone, and your specific situation, risk tolerance, and market conditions should be considered when deciding on a withdrawal rate.

To manage your portfolio effectively, consider working with a financial advisor who can help you create a personalized investment plan. Diversification is key to managing your portfolio. Spreading your investments across different asset classes, such as stocks, bonds, and alternative investments, can help manage risk and provide a more consistent income stream. Additionally, regular portfolio rebalancing is important to ensure your asset allocation remains aligned with your risk tolerance and income needs.

Finally, it is important to plan for the unexpected. Retirement can bring unforeseen expenses, such as medical emergencies or the need for long-term care. Having an emergency fund set aside can help cover these unexpected costs without derailing your retirement plan. Additionally, consider insurance options to protect against these risks, such as long-term care insurance or a comprehensive health insurance plan. By planning for the unexpected, you can ensure that your retirement portfolio remains resilient and can provide for your needs throughout your retirement journey.

The TSP: Where Your Money Is Invested

You may want to see also

Frequently asked questions

This depends on your age and circumstances. As a general rule, it is recommended that you save 11 times your ending salary by the time you retire. T. Rowe Price analysis suggests that by age 45, you should have three times your current income saved, rising to five times by age 50 and seven times by age 55.

This depends on your age and risk tolerance. When starting out, aim for a portfolio that is heavy on equities, as these have historically outperformed fixed-income investments. As you get older, adopt a more conservative stance with a mix of stocks, fixed income, and cash.

Money managers often advise using the 4% rule to estimate how much money you will need for retirement. This means taking 4% of your savings each year, adjusted for inflation. For example, with $500,000 in savings, you can count on receiving $20,000 in the first year.

Start saving and investing as early as possible to take advantage of compounding returns.

Your portfolio should contain the appropriate balance of investments for growth, income, and capital preservation, based on your personal risk tolerance, investment objectives, and time horizon. Focus on growth until you reach middle age, then shift towards income and lower risk.