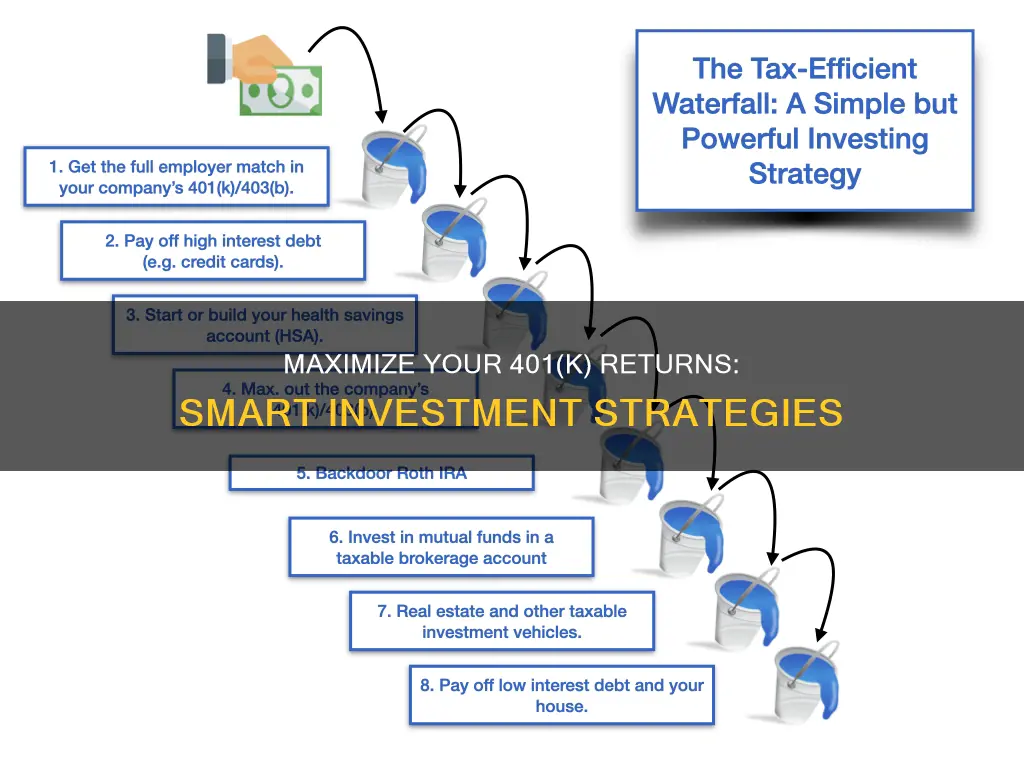

Investing in your 401(k) is a smart way to build long-term wealth and secure your financial future. It's a powerful tool that allows you to save for retirement while taking advantage of tax benefits and potential employer matching contributions. This guide will provide a comprehensive overview of how to maximize your 401(k) investments, including understanding different investment options, setting clear financial goals, and creating a well-diversified portfolio. We'll also discuss strategies for managing risk, staying informed about market trends, and making adjustments to your investment plan as needed. By following these steps, you can make the most of your 401(k) and achieve your retirement goals with confidence.

What You'll Learn

- Understand Your 401(k) Options: Research and compare different investment choices offered by your employer

- Diversify Your Portfolio: Spread investments across various asset classes to minimize risk

- Consider Risk Tolerance: Assess your financial goals and risk comfort level to guide investment decisions

- Regularly Review and Rebalance: Periodically adjust your portfolio to maintain desired asset allocation

- Take Advantage of Employer Matching: Maximize contributions by utilizing any employer-matching programs available

![]()

Understand Your 401(k) Options: Research and compare different investment choices offered by your employer

Understanding the investment options available in your 401(k) plan is a crucial step towards building a secure financial future. When you have a comprehensive understanding of the choices, you can make informed decisions that align with your financial goals and risk tolerance. Here's a guide to help you navigate this process:

Research the Investment Options: Start by reviewing the investment choices provided by your employer. Most 401(k) plans offer a range of investment funds, including stocks, bonds, mutual funds, and sometimes alternative investments. Study the descriptions and objectives of each fund. Understand the nature of the investments, such as whether they are growth-oriented, income-focused, or a mix of both. Look for funds that align with your investment strategy and risk profile. For instance, if you're risk-averse, consider more conservative options like bonds or balanced funds.

Compare Performance and Fees: Evaluate the historical performance of the investment options. Review the returns over different time periods to gauge how each fund has performed in the past. Keep in mind that past performance doesn't guarantee future results, but it can provide valuable insights. Additionally, consider the associated fees and expenses. These may include management fees, transaction costs, or 12b-1 fees, which are marketing and distribution expenses. Lower fees generally mean more of your money works for you, so compare these costs across different funds.

Diversify Your Portfolio: Diversification is a key principle in investing. It involves spreading your investments across various asset classes, sectors, and geographic regions to reduce risk. Review the investment options and assess how they contribute to a well-diversified portfolio. Aim for a mix that aligns with your investment goals and risk tolerance. Diversification can help protect your savings during market fluctuations and ensure long-term growth potential.

Consider Your Time Horizon: Your investment time horizon is the length of time you plan to keep your money invested. It's essential to match your investment choices with your financial goals and retirement timeline. For example, if you're close to retirement, you might opt for more conservative investments to preserve capital. On the other hand, if you have a longer time horizon, you can consider more aggressive growth-oriented options. Regularly review and adjust your investments as your life circumstances and goals evolve.

Seek Professional Guidance: If you feel overwhelmed or unsure about making investment decisions, consider consulting a financial advisor or planner. They can provide personalized advice based on your unique financial situation and goals. A professional can help you navigate the complexities of 401(k) investments, ensure tax efficiency, and offer strategies to optimize your retirement savings. Remember, seeking guidance is a sign of financial responsibility and can lead to better-informed investment choices.

The Maverick Investor: Will Thompson's Unconventional Path to Success

You may want to see also

![]()

Diversify Your Portfolio: Spread investments across various asset classes to minimize risk

When it comes to investing in your 401(k), one of the most important strategies to adopt is diversification. This strategy involves spreading your investments across various asset classes to minimize risk and maximize potential returns. By diversifying, you reduce the impact of any single investment's performance on your overall portfolio, ensuring a more stable and secure financial future.

The core idea behind diversification is to allocate your funds across different types of assets, such as stocks, bonds, real estate, and commodities. Each asset class has its own unique characteristics and risk profile. For instance, stocks offer the potential for high returns but come with higher risk, while bonds provide a more stable, lower-risk investment option. By diversifying, you create a balanced portfolio that can weather market fluctuations and provide a more consistent performance over time.

To start diversifying your 401(k), consider the following steps. Firstly, evaluate your risk tolerance and investment goals. Are you comfortable with higher-risk investments for potentially greater returns, or do you prefer a more conservative approach? Understanding your risk tolerance will guide your asset allocation decisions. Next, research and identify the various investment options available within your 401(k) plan. These may include different mutual funds, exchange-traded funds (ETFs), or even individual stocks and bonds.

Once you've identified the available investment options, create a well-rounded portfolio by allocating your contributions across these different asset classes. For example, you might choose to invest a portion of your 401(k) in a growth-oriented stock fund, another part in a bond fund for stability, and potentially a small allocation to a real estate investment trust (REIT) for diversification into the real estate sector. Regularly review and rebalance your portfolio to ensure it remains aligned with your risk tolerance and investment objectives.

Diversification is a long-term strategy, and it's important to remain committed to it, especially during market volatility. By spreading your investments, you reduce the impact of any short-term market fluctuations, allowing your portfolio to grow and compound over time. Remember, the goal is to build a resilient investment portfolio that can weather various economic cycles and provide financial security for your retirement.

Impeachment Impact: Navigating Investments Through Political Turmoil

You may want to see also

![]()

Consider Risk Tolerance: Assess your financial goals and risk comfort level to guide investment decisions

When it comes to investing in your 401(k), understanding your risk tolerance is crucial. Risk tolerance refers to your ability and willingness to withstand fluctuations in the value of your investments. It's an essential factor in determining the types of investments you should consider. Here's how you can assess your risk tolerance and use it to guide your investment decisions:

Evaluate Your Financial Goals: Start by defining your short-term and long-term financial goals. Are you saving for retirement, a down payment on a house, or a child's education? Your goals will influence the level of risk you're willing to take. For instance, if you have a long time horizon until retirement, you might be more comfortable with riskier investments that have historically shown higher returns over the long term. On the other hand, if you need to access your funds soon, you may prefer more conservative investments to preserve capital.

Assess Your Risk Comfort Level: Consider your emotional and psychological comfort with market volatility. Some individuals thrive in volatile markets, quickly recovering from losses and capitalizing on short-term gains. Others may find such volatility stressful and prefer a more stable investment environment. Reflect on your risk tolerance by asking yourself questions like: Can I handle significant market downturns without panicking? Am I comfortable with the possibility of lower returns in exchange for potential higher gains? Understanding your risk comfort level will help you choose between aggressive, moderate, or conservative investment strategies.

Diversify Your Portfolio: Risk tolerance is not a one-size-fits-all concept. It's essential to diversify your investments to manage risk effectively. Diversification means spreading your money across different asset classes, sectors, and geographic regions. For example, you could allocate a portion of your 401(k) to stocks, bonds, mutual funds, or exchange-traded funds (ETFs). Diversification ensures that your portfolio can weather market fluctuations, as different asset classes perform differently at various times.

Regularly Review and Adjust: Risk tolerance is not static; it can change over time due to life events, economic conditions, or shifting financial goals. Regularly review your 401(k) investments and assess whether they still align with your risk tolerance. Life changes, such as a new job, marriage, or the birth of a child, might prompt you to adjust your investment strategy. For instance, if you've recently started a family, you may want to increase your allocation to more conservative investments to ensure financial security for your loved ones.

By considering your risk tolerance and regularly evaluating your investment choices, you can make informed decisions about your 401(k) that align with your financial goals and comfort level with risk. Remember, investing is a long-term journey, and finding the right balance between risk and reward is key to building a successful retirement nest egg.

Retirement Savings: Investing Not Required

You may want to see also

![]()

Regularly Review and Rebalance: Periodically adjust your portfolio to maintain desired asset allocation

Regularly reviewing and rebalancing your 401(k) portfolio is a crucial practice to ensure your investments stay on track and align with your financial goals. This process involves periodically assessing the performance of your investments and making adjustments to bring them back to your desired asset allocation. Here's a step-by-step guide to help you navigate this essential aspect of managing your retirement savings:

Understand Your Asset Allocation: Begin by identifying your target asset allocation, which is the desired percentage of your portfolio invested in different asset classes such as stocks, bonds, and cash equivalents. For instance, you might aim for a 60/40 split between stocks and bonds. Understanding your target allocation is key to knowing when and how to rebalance.

Schedule Regular Reviews: Set a calendar reminder to review your 401(k) portfolio at regular intervals. Quarterly or semi-annual reviews are common, but you can adjust this frequency based on your risk tolerance and investment strategy. During these reviews, analyze the performance of each asset class and compare it to your target allocation. This process ensures that your investments are growing in line with your expectations.

Rebalance When Necessary: If your portfolio deviates from your target asset allocation, it's time to rebalance. Rebalancing involves buying or selling assets to return your portfolio to the desired allocation. For example, if your stock holdings have outperformed and now make up 70% of your portfolio, you would need to sell some stocks and buy more bonds or other asset classes to reach the 60/40 target. Regular rebalancing helps manage risk and ensures your investments remain diversified.

Consider Market Conditions: Market fluctuations can impact your asset allocation. During market downturns, certain asset classes may be over-represented in your portfolio. In such cases, rebalancing can help reduce risk by selling assets that have appreciated and buying those that have underperformed. Conversely, in a bull market, you might need to rebalance to prevent over-exposure to certain sectors or asset classes.

Automate the Process (Optional): To make rebalancing easier, consider setting up automatic contributions or transfers within your 41(k) plan. Many employers offer the option to automatically invest contributions in a default investment strategy, which can help maintain your desired asset allocation over time. Additionally, some financial institutions provide automated rebalancing services, where they periodically adjust your portfolio to keep it aligned with your goals.

By implementing regular portfolio reviews and rebalancing, you take control of your 401(k) investments and increase the likelihood of achieving your retirement savings objectives. Remember, this process requires discipline and a long-term perspective, but it is a powerful tool for managing your financial future.

Unleashing Investment Strategies: Exploring Options Beyond the Paid-Off Home

You may want to see also

![]()

Take Advantage of Employer Matching: Maximize contributions by utilizing any employer-matching programs available

Maximizing your contributions to a 401(k) plan is a smart financial move, and one of the most effective ways to do this is by taking advantage of employer-matching programs. These programs are essentially free money that your employer is offering to encourage you to save for retirement. Here's how you can make the most of this opportunity:

First, understand the matching policy at your workplace. Many companies will match a certain percentage of your contributions, often up to a specific amount. For example, they might match 50% of your contributions, but only up to 6% of your salary. This means that if you contribute 6% of your salary, the employer will add an additional 3% to your 401(k) account, effectively doubling your savings. It's a simple way to boost your retirement savings without any additional effort from your side.

To maximize this benefit, ensure that you contribute enough to reach the maximum match. If your employer matches 50% of your contributions, aim to contribute at least 6% of your salary to get the full match. Even if you can't contribute the full amount, try to get as close as possible, as every little bit helps. You can adjust your contributions periodically to ensure you're getting the most out of the program.

Additionally, consider increasing your contributions when your salary increases. As your income grows, so can your 401(k) contributions. This way, you can take full advantage of the employer match at higher salary levels. Regularly reviewing and adjusting your contributions will ensure that you're making the most of this valuable benefit.

Remember, employer-matching programs are a great way to boost your retirement savings without any additional cost to you. It's essentially free money, so make sure you're not leaving it on the table. By understanding and utilizing these programs effectively, you can significantly enhance your financial security for the future.

Student Loans vs. Investing: Navigating the Trade-offs

You may want to see also

Frequently asked questions

Investing in your 401(k) is a great way to build long-term wealth. Here are some strategies to consider: First, understand your risk tolerance. You can choose between various investment options like stocks, bonds, mutual funds, or exchange-traded funds (ETFs). Diversification is key; allocate your contributions across different asset classes to balance risk and potential returns. Consider the following: target date funds, which are designed to adjust their asset allocation as you approach retirement, or index funds that track a specific market index, offering broad market exposure. Regularly review and rebalance your portfolio to maintain your desired asset allocation.

Yes, investing in stocks or mutual funds within your 401(k) is possible and can be a powerful way to grow your savings. Stocks represent ownership in companies and offer the potential for higher returns but also come with higher risk. Mutual funds, which are pools of money from many investors, allow you to invest in a diversified portfolio of stocks, bonds, or other securities. These investment options can provide long-term growth potential. However, it's essential to assess your risk tolerance and investment goals before making any changes to your 401(k) investments.

Contributing to your 401(k) offers significant tax benefits. Firstly, contributions are typically made pre-tax, reducing your taxable income for the year. This means you pay taxes on the money you contribute later when you withdraw it during retirement. Additionally, in many countries, including the United States, contributions to traditional 401(k) plans are tax-deductible, providing an immediate tax benefit. The earnings on your investments within the 401(k) grow tax-deferred, allowing your savings to compound over time.

Managing your 401(k) investments when changing jobs is straightforward. When you leave an employer, you have several options: roll over your 401(k) to an Individual Retirement Account (IRA), keep it in a new employer's 401(k) plan if they allow it, or take a distribution. Rolling over to an IRA provides flexibility and control over your investments. If you choose to keep it in a new employer's plan, understand the investment options and fees associated with the new plan. Regularly reviewing and rebalancing your portfolio remains essential, regardless of the plan you choose.