Considering investing in long-term collateralized debt obligations (CDOs) can be a complex decision, as it involves assessing various financial and market factors. Long-term CDOs are a type of fixed-income security that can offer diversification and potential returns, but they also carry risks, especially in volatile markets. Before making an investment, it's crucial to understand the underlying assets, the structure of the CDO, and the potential impact of economic conditions on its performance. This introduction aims to provide a starting point for evaluating the pros and cons of investing in long-term CDOs, helping investors make informed decisions based on their financial goals and risk tolerance.

What You'll Learn

- Market Conditions: Assess current market trends and interest rates to gauge potential returns

- Risk Assessment: Evaluate the risk of default and potential losses in a long-term investment

- Credit Quality: Understand the creditworthiness of the underlying asset to make informed decisions

- Tax Implications: Consider tax effects and potential savings or costs over the investment period

- Diversification: Explore how CDS fits into your overall investment strategy and portfolio diversification

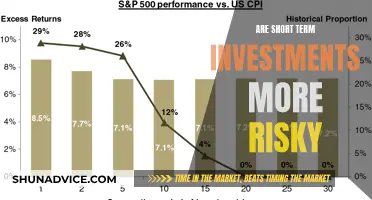

![]()

Market Conditions: Assess current market trends and interest rates to gauge potential returns

When considering an investment in long-term Credit Default Swaps (CDS), it is crucial to thoroughly analyze the current market conditions, particularly the state of interest rates. The relationship between interest rates and CDS is intricate and can significantly impact your investment strategy. Firstly, understanding the current interest rate environment is essential. Interest rates play a pivotal role in the bond market, influencing the yield and value of fixed-income securities. When interest rates rise, bond prices typically fall, and vice versa. This dynamic is particularly relevant for long-term investments, as interest rate changes over an extended period can have a substantial effect on the overall performance of your CDS portfolio.

Assess the current market trends to identify potential shifts in interest rates. Central banks and financial institutions often adjust interest rates in response to economic conditions. For instance, during economic downturns, central banks may lower interest rates to stimulate borrowing and investment, which could lead to a decline in interest rates over the long term. Conversely, in periods of economic growth, interest rates might rise to control inflation, potentially impacting the value of long-term CDS investments. By monitoring these trends, you can anticipate how interest rate movements will affect the creditworthiness of the underlying reference entities in your CDS.

The assessment of market conditions should also include an analysis of the credit quality of the reference entities in the CDS. Interest rates and creditworthiness are closely intertwined. When interest rates rise, the cost of borrowing increases, which can negatively impact the financial health of companies and governments, potentially leading to higher default risk. Therefore, evaluating the creditworthiness of the reference entities is vital to understanding the potential returns on your long-term CDS investment. A thorough credit analysis should consider factors such as the entity's financial stability, debt levels, and ability to meet financial obligations.

Additionally, staying informed about economic indicators and global market events is essential. Economic data, such as GDP growth, inflation rates, and employment statistics, can influence interest rate decisions and, consequently, the performance of CDS. Global events, including geopolitical tensions or financial crises, may also impact interest rates and credit markets, affecting the overall market sentiment and the value of your CDS investment. By keeping a close eye on these factors, you can make more informed decisions regarding the timing and strategy of your long-term CDS investment.

In summary, assessing market conditions and interest rates is a critical step in determining the potential returns of a long-term CDS investment. It involves understanding the interest rate environment, monitoring market trends, evaluating credit quality, and staying informed about economic and global events. By carefully analyzing these factors, investors can make more strategic decisions, ensuring their long-term CDS investments align with their financial goals and risk tolerance.

Notes Receivable: Short-Term Investment or Long-Term Liability?

You may want to see also

![]()

Risk Assessment: Evaluate the risk of default and potential losses in a long-term investment

When considering a long-term investment in Credit Default Swaps (CDS), a thorough risk assessment is crucial to ensure a well-informed decision. The primary risk in CDS is the potential for default, which can lead to significant financial losses. Here's a step-by-step guide to evaluating these risks:

- Understand the Underlying Reference: Start by thoroughly researching the underlying asset or entity that the CDS is referencing. This could be a company, a government, or even a basket of securities. Assess the creditworthiness of the reference entity. Look for factors such as their financial health, revenue streams, and historical performance. For instance, if you're considering a CDS on a corporate bond, examine the company's balance sheet, debt levels, and its ability to meet financial obligations.

- Evaluate Default Probability: Default risk is the core concern in CDS. Use statistical models and historical data to estimate the probability of default over the investment horizon. Credit rating agencies provide valuable insights, but remember that ratings can change, so monitor these closely. Consider economic indicators and industry-specific risks that could impact the reference entity's ability to pay. For example, a prolonged recession might increase the likelihood of defaults.

- Assess Recovery Rates: In the event of default, recovery rates determine how much of the principal amount an investor can expect to receive. Research and analyze historical recovery rates for similar defaults. Lower recovery rates mean more significant potential losses if default occurs. This factor is crucial in understanding the potential upside and downside of the investment.

- Consider Market Factors: Market dynamics play a significant role in CDS risk assessment. Volatility in the market can impact the value of the CDS contract. Evaluate the liquidity of the CDS market, as illiquid markets might lead to wider bid-ask spreads, affecting the cost of entering or exiting the position. Additionally, monitor interest rate changes, as they can influence the value of CDS, especially for long-term investments.

- Stress Testing and Scenario Analysis: Perform stress tests to simulate various adverse scenarios. This involves pushing the reference entity's financial metrics to extreme levels to assess the potential impact on the CDS investment. Scenario analysis can help identify potential triggers for default and the corresponding losses. For instance, a sudden drop in stock prices or a significant increase in interest rates could lead to default and substantial losses.

By following these steps, investors can make a more informed decision about investing in long-term CDS. It is essential to stay updated on market trends, economic forecasts, and the financial health of the referenced entities to manage risks effectively.

Understanding Long-Term Notes Payable: An Investing Activity Analysis

You may want to see also

![]()

Credit Quality: Understand the creditworthiness of the underlying asset to make informed decisions

When considering an investment in Long-Term Credit Default Swaps (CDS), understanding the credit quality of the underlying asset is paramount. CDS are financial instruments that protect against the default of a debt obligation, typically a bond or loan. The creditworthiness of the underlying asset directly impacts the risk and potential returns of the CDS investment. Here's a detailed breakdown:

Assessing Credit Quality:

- Credit Rating: Start by examining the credit rating of the underlying asset. Credit rating agencies like Moody's, S&P, and Fitch assign ratings indicating the likelihood of default. Higher-rated securities (e.g., AAA) are generally considered less risky, while lower-rated ones (e.g., BB or B) are more speculative and carry higher default risk.

- Industry and Sector Analysis: Consider the industry and sector in which the underlying asset operates. Some sectors are inherently more prone to default due to economic cycles, regulatory changes, or other factors. For instance, real estate-backed securities might be more vulnerable during economic downturns.

- Financial Health and Performance: Analyze the financial health and performance of the issuer. This includes reviewing financial statements, cash flow projections, and debt-to-equity ratios. Strong financial health indicates a higher likelihood of timely debt payments and reduces the risk of default.

Making Informed Decisions:

- Risk Tolerance: Your risk tolerance plays a crucial role. If you're risk-averse, you might prefer investing in CDS with higher-rated underlying assets. More aggressive investors might target lower-rated securities, seeking higher potential returns but at increased risk.

- Diversification: Diversifying your CDS portfolio across different credit ratings and sectors can help mitigate risk. Don't put all your eggs in one basket.

- Market Sentiment and News: Stay informed about market sentiment and news related to the underlying asset. Economic indicators, regulatory changes, and industry trends can significantly impact credit quality and CDS prices.

Monitoring and Adjustments:

- Regular Monitoring: Credit quality can change over time. Regularly monitor the underlying asset's credit rating, financial health, and industry performance.

- Adjustments: Be prepared to adjust your CDS portfolio based on changes in credit quality. If a security's credit rating deteriorates, consider selling the CDS or hedging your position.

Remember, investing in CDS involves complex risks. Thorough research, a clear understanding of your risk tolerance, and ongoing monitoring are essential for making informed decisions.

Nurture Your Future Self: A Guide to Long-Term Self-Investment

You may want to see also

![]()

Tax Implications: Consider tax effects and potential savings or costs over the investment period

When considering an investment in long-term Constant Dividend Securities (CDS), it's crucial to delve into the tax implications to ensure you make an informed decision. Tax laws and regulations can significantly impact your overall returns, and understanding these effects is essential for long-term financial planning. Here's a breakdown of the tax considerations:

Tax Treatment of CDS:

The tax treatment of CDS can vary depending on your jurisdiction and the specific structure of the investment. In many countries, CDS are treated as fixed-income securities, which means they are subject to income tax on the interest or dividends received. This is similar to the taxation of bonds or other fixed-income instruments. It's important to note that the tax rate applied to CDS income may vary based on your tax bracket and the holding period of the investment.

Tax Savings or Costs:

- Tax Deductions: One of the potential advantages of CDS is the possibility of tax deductions. If you are in a higher tax bracket, you might be able to deduct the interest or dividend income from CDS, thus reducing your taxable income. This can result in significant tax savings, especially over a long investment horizon. For example, if you invest in a CDS with a 5% annual return and hold it for 10 years, the tax savings could accumulate over time.

- Capital Gains Tax: CDS investments may also generate capital gains if the value of the security increases over time. Understanding the capital gains tax rate applicable to your jurisdiction is crucial. In some cases, long-term capital gains may be taxed at a lower rate than ordinary income, providing an incentive for investors to hold CDS for extended periods.

- Tax Efficiency: The tax efficiency of CDS can be enhanced by strategic investment timing. For instance, if you anticipate a tax increase in the future, you might consider investing in CDS now to take advantage of current tax rates. This strategy can help optimize your after-tax returns.

Long-Term Considerations:

When investing in long-term CDS, it's essential to consider the potential tax implications over the entire investment period. Tax laws can change, and different governments may introduce new regulations that could impact your tax liability. Staying informed about tax policy changes and consulting with a tax professional can help you navigate these complexities. Additionally, understanding the tax treatment of any distributions or redemptions from the CDS is crucial for accurate financial planning.

In summary, investing in long-term CDS involves careful consideration of tax effects. By understanding the tax treatment, potential deductions, and capital gains implications, investors can make strategic decisions to optimize their after-tax returns. It is always advisable to seek professional tax advice to ensure compliance with local tax laws and to make the most of any tax-efficient investment opportunities.

Cracking the Code: Long-Term Crude Oil Investment Strategies

You may want to see also

![]()

Diversification: Explore how CDS fits into your overall investment strategy and portfolio diversification

When considering the inclusion of Credit Default Swaps (CDS) in your investment strategy, it's essential to understand how they can contribute to portfolio diversification. CDS are financial instruments that allow investors to speculate on or hedge against the default risk of a particular bond or loan. They are a form of insurance, where one party agrees to pay another party in the event of a default by a specified borrower. This makes CDS a valuable tool for managing credit risk, which is a critical component of any investment portfolio.

Diversification is a key principle in investment management, aiming to reduce risk by allocating assets across various sectors, industries, and asset classes. CDS can be a powerful tool in this regard, as they provide exposure to credit risk without directly investing in the underlying debt instruments. By incorporating CDS into your portfolio, you can gain exposure to a wide range of credit risks, including those from different countries, sectors, and credit ratings. This broadens your investment horizons and can help reduce the overall volatility of your portfolio.

For instance, if you have a portfolio heavily weighted towards government bonds, adding CDS that cover corporate bonds can introduce a new dimension of risk and return. This strategy allows you to participate in the credit markets while maintaining a diversified approach. Similarly, if your portfolio is concentrated in a specific industry, CDS can provide exposure to credit risks in other sectors, thus reducing the impact of any single industry's performance on your overall portfolio.

However, it's important to note that CDS should be used strategically and in conjunction with other investment tools. While they offer diversification benefits, they also come with their own set of risks, such as counterparty risk and the potential for significant price fluctuations. Therefore, investors should carefully consider their risk tolerance and ensure that CDS are used as part of a well-rounded investment strategy.

In summary, CDS can be a valuable addition to your investment strategy for portfolio diversification. They offer exposure to a wide range of credit risks, allowing you to manage and mitigate potential losses. By incorporating CDS, investors can create a more balanced and resilient portfolio, ensuring that their investments are not overly exposed to any single market or sector. As with any investment decision, thorough research and a clear understanding of the risks involved are essential.

Unveiling the Secrets: A Guide to Spotting Long-Term Investment Gems

You may want to see also

Frequently asked questions

Credit Default Swaps are financial derivatives that allow investors to speculate on the creditworthiness of a company or entity. They are essentially insurance contracts that protect investors against potential credit events, such as a company defaulting on its debt.

Long-term CDS can be attractive for investors seeking to hedge against potential credit risks over an extended period. By investing in these derivatives, you can gain exposure to the credit market while potentially benefiting from favorable interest rate environments.

CDS carry several risks. Firstly, they can be complex and may not be suitable for all investors. The value of CDS can be influenced by various factors, including credit ratings, market sentiment, and economic conditions. Secondly, CDS are leveraged instruments, meaning small price movements can result in significant gains or losses.

Valuing CDS requires a thorough understanding of credit risk and market dynamics. Investors should consider factors such as the underlying credit, the duration of the swap, and the current market conditions. It is recommended to consult financial advisors or use specialized valuation models to assess the potential returns and risks.

Tax treatment for CDS can vary depending on the jurisdiction and the specific structure of the investment. In some cases, CDS may be treated as a speculative investment, while in others, they might be considered a hedging instrument. It is essential to seek professional tax advice to understand the potential tax consequences and ensure compliance with relevant regulations.