A fully amortizing loan is a type of loan where the borrower makes scheduled payments that cover both the principal and interest over a specified period, resulting in the total repayment of the loan by the end of the term. This is a common repayment structure for loans, including mortgages, and it allows borrowers to budget more easily and plan their finances with confidence. The interest rate on a fully amortizing loan can be fixed or adjustable, but the loan is structured so that the borrower pays off the entire principal by the end of the loan term.

| Characteristics | Values |

|---|---|

| Amortization schedule | A schedule that outlines the division of payments, i.e., how much of each payment is applied to interest and principal over the loan's lifetime. |

| Payment structure | Each payment contributes to gradually reducing the outstanding principal while also covering the interest charges. |

| Certainty of repayment | Provides certainty that the loan will be fully paid off by the end of the term. |

| Payment amount | The amount of each payment that goes toward principal and interest changes over time, with the majority of the early payments covering interest and a larger portion of the principal paid down over time. |

| Interest rate | Can be fixed or adjustable. In the case of a fixed-rate loan, each payment is an equal dollar amount, while in an adjustable-rate loan, the payment amount changes as the interest rate changes. |

| Budgeting | Allows borrowers to budget more easily as they know how their monthly loan payment is divided up. |

| Common loan types | Mortgages are a typical example of self-amortizing loans. |

What You'll Learn

![]()

Fixed-rate vs. adjustable-rate mortgages

When considering taking out a loan, it is important to understand the repayment model. One common repayment structure is a fully amortized loan. Fully amortizing loans have schedules such that the amount of your payment that goes toward principal and interest changes over time so that your balance is fully paid off by the end of the loan term.

Fixed-rate mortgages and adjustable-rate mortgages (ARMs) are the two types of mortgages that have different interest rate structures. With a fixed-rate mortgage, the interest rate remains the same throughout the loan's term. The only thing that changes is the relative amount of principal and interest being paid month-to-month. At the beginning of the loan, you pay way more interest than you do principal. Over time, the scale tips in the other direction. Fixed-rate mortgages typically come in 30-year and 15-year terms, but there are also flexible term options anywhere from eight years to 29 years. The 30-year mortgage, which offers the lowest monthly payment, is often a popular choice. However, the longer your mortgage term, the more you will pay in overall interest. The monthly payments for shorter-term mortgages are higher so that the principal is repaid in a shorter time frame. Shorter-term mortgages offer a lower interest rate, which allows for a larger amount of principal to be repaid with each mortgage payment. So, shorter-term mortgages usually cost significantly less in interest.

On the other hand, an ARM's interest rate can change multiple times over the loan term. The monthly mortgage payment will change, too, if the index rises and falls. The interest rate for an adjustable-rate mortgage is variable. The initial interest rate on an ARM is usually below the interest rate on a comparable fixed-rate loan. The low rate will stay the same for a certain period of time, with the common types being 5, 7 or 10 years. After the fixed-rate period ends, your interest rate will adjust up or down based on an index, like the London Interbank Offered Rate (LIBOR). ARMs are more complicated than fixed-rate loans, so understanding the pros and cons requires an understanding of some basic terminology.

Becoming a Loan Signing Agent: Nevada Requirements

You may want to see also

![]()

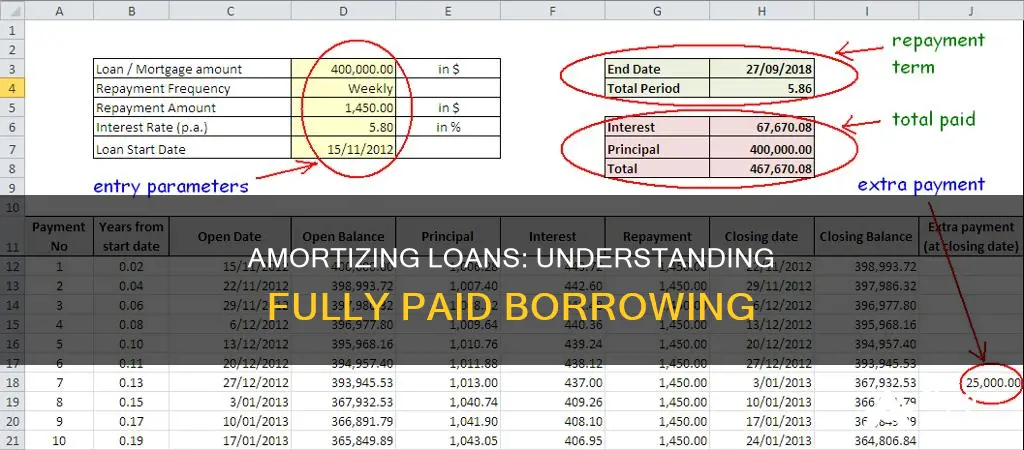

Amortization schedules

An amortization schedule is a table that outlines each periodic payment on an amortizing loan. It shows how much of each payment is comprised of interest and how much is repayment of the principal. It also shows the interest and principal paid to date, and the remaining principal balance after each pay period.

For example, a borrower with a $300,000 30-year mortgage at a 6% interest rate will pay $1,799 per month for the duration of the loan. Their first payment will consist of $1,500 paid towards interest and the remaining $299 paid towards the principal. Over time, the borrower will pay less towards interest and more towards the principal with each payment until the loan is paid off.

Underwriter's Decision: Approving Your Loan Application

You may want to see also

![]()

Repayment models

A fully amortizing loan is a common repayment structure where the borrower pays off their balance according to the loan's amortization schedule. The amortization schedule outlines how much of each payment goes towards the principal and interest over the course of the loan term. By following this schedule, the borrower will fully repay the loan by the end of the term.

At the beginning of a fully amortizing loan, the majority of the payments are devoted to interest, with only a small portion going towards the principal. As the loan progresses, the scales gradually tip, and towards the end of the loan term, the majority of the payments cover the principal, with a smaller portion allocated to interest. This shift in the payment breakdown allows borrowers to build equity over time.

The amortization schedule for a fixed-rate loan remains constant throughout the loan term, providing predictability for borrowers. While the combined principal and interest payment stays the same, the allocation towards each component changes monthly, with the amount going towards the principal balance increasing and the interest portion decreasing. This dynamic ensures the loan balance is zero at the end of the term.

On the other hand, adjustable-rate mortgages (ARMs) have varying interest rates, which can lead to adjustments in the amortization schedule. Typically, the initial interest rate is fixed for a period of 5, 7, or 10 years, after which the rate may change annually. The loan will re-amortize each time the interest rate adjusts, ensuring that the loan balance is fully paid off by the end of the term, even with fluctuating interest rates.

Fully amortizing loans offer advantages such as budgeting ease and certainty of repayment in monthly increments. However, a significant drawback is the requirement to pay a substantial amount of interest upfront, particularly within the first few years of the loan. This can result in limited equity accumulation if the borrower decides to sell their home or property early on in the loan term.

Grace Loan Advance: Understanding This Unique Financial Offering

You may want to see also

![]()

Interest-only loans

An interest-only loan is a type of loan that is, in most cases, structured as an adjustable-rate mortgage (ARM). In this loan structure, the borrower is only required to pay the interest on the loan for a specified period of time, typically five, seven, or ten years. During this introductory period, the borrower's monthly payments are significantly lower compared to a fully amortizing loan, as they are only paying off the interest and not the principal debt.

The interest-only period provides borrowers with the benefit of lower initial monthly payments, which can increase their cash flow and potentially allow them to afford a pricier home. However, it is important to note that during this period, the borrower is not building any equity in the property, as only the repayment of the principal debt achieves that. Once the interest-only period ends, the borrower must begin paying off both the interest and the principal, resulting in significantly higher monthly payments.

At the end of the interest-only mortgage term, borrowers have several options. They may choose to refinance their loan, which can provide new terms and potentially lower interest payments. They could also sell the home to pay off the loan or make a one-time lump-sum payment if they have saved enough during the interest-only period. It is crucial for borrowers to cautiously estimate their expected future cash flow to ensure they can meet the larger monthly obligations when both interest and principal payments are required.

Becoming a Loan Signing Agent: Maryland Requirements

You may want to see also

![]()

Balloon payments

A balloon payment is a large, one-time payment that is due at the end of a loan term. Balloon payments are commonly associated with mortgages, but they can also be used for auto loans and business loans. The loan is structured so that the borrower makes small monthly payments, followed by a single, much larger sum at the end of the loan period. The initial payments may cover all or almost all of the interest owed on the loan, with the balloon payment covering the principal.

Balloon loans are often packaged into two-step mortgages, where the borrower receives a lower interest rate at the start of the loan, which then shifts to a higher interest rate after an initial borrowing period. The term lengths are typically shorter than traditional mortgages, ranging from 5 to 10 years. This means that the borrower benefits from lower monthly payments during the initial period. However, they will need to be able to afford the large balloon payment at the end of the loan term.

The risk introduced by balloon payments is that the borrower may not have the financial means to make the final payment. In this case, the borrower may be able to refinance the loan to avoid the balloon payment. However, if the borrower's financial condition declines or the value of the property falls, refinancing may not be possible. If the borrower cannot pay the balloon mortgage, even at the last payment, they could face foreclosure.

Selling a Boat with a Loan: What You Need to Know

You may want to see also

Frequently asked questions

A fully amortizing loan is a type of loan in which the borrower makes scheduled payments that cover both the principal and interest over a specified period. The loan will be fully paid off by the end of the term.

A fully amortizing loan ensures that the entire principal will be paid off by the end of the loan's term. In contrast, a partially amortizing loan will leave a balloon payment at the end of the loan's term.

A fully amortizing loan gives clarity and predictability to both lenders and borrowers. It allows borrowers to budget more easily as they know how their monthly loan payment is divided.

A fully amortizing loan is common in mortgage agreements. For example, a 30-year fixed-rate mortgage with a $400,000 principal amount and a 4.5% interest rate. The borrower will make 360 monthly payments of $1,934.52, paying off the loan in full by the end of the term.