Unitranche financing is a hybrid loan structure that combines senior and subordinated debt into a single loan with a blended interest rate. It is often used by mid-sized companies to fund acquisitions or ownership transitions, providing a simplified structure and certainty of closure when working with tight timelines. Unitranche loans are typically attractive to middle-market borrowers with annual sales of less than $100 million and an EBITDA of less than $50 million. The main goal of unitranche financing is to make debt financing terms more flexible and increase access to capital for companies.

| Characteristics | Values |

|---|---|

| Definition | A hybrid loan structure that combines senior and subordinated debt into one loan |

| Interest Rate | A blended interest rate that falls between the rate of the senior debt and subordinated debt |

| Borrowers | Middle-market corporate borrowers with sales of less than $100 million and an EBITDA of less than $50 million |

| Loan Amount | The average size of a unitranche loan is $100 million |

| Usage | Used to finance leveraged buyouts such as management buyouts and private equity acquisitions |

| Agreement | Requires a single credit agreement and one set of collateral documents |

| Repayment | Requires a one-time lump-sum repayment of the entire loan at maturity |

| Benefits | Simplicity, flexibility, and increased access to capital for companies |

| Providers | Non-traditional lending entities such as debt funds and other institutional lenders |

What You'll Learn

![]()

Unitranche loans combine senior and subordinated debt

Unitranche loans are a hybrid model that combines senior and subordinated debt into a single loan. This allows borrowers to access funds from multiple parties, including banks and alternative capital investors, and potentially close deals faster. The interest rate for the borrower sits between the highest and lowest rates of the individual loans.

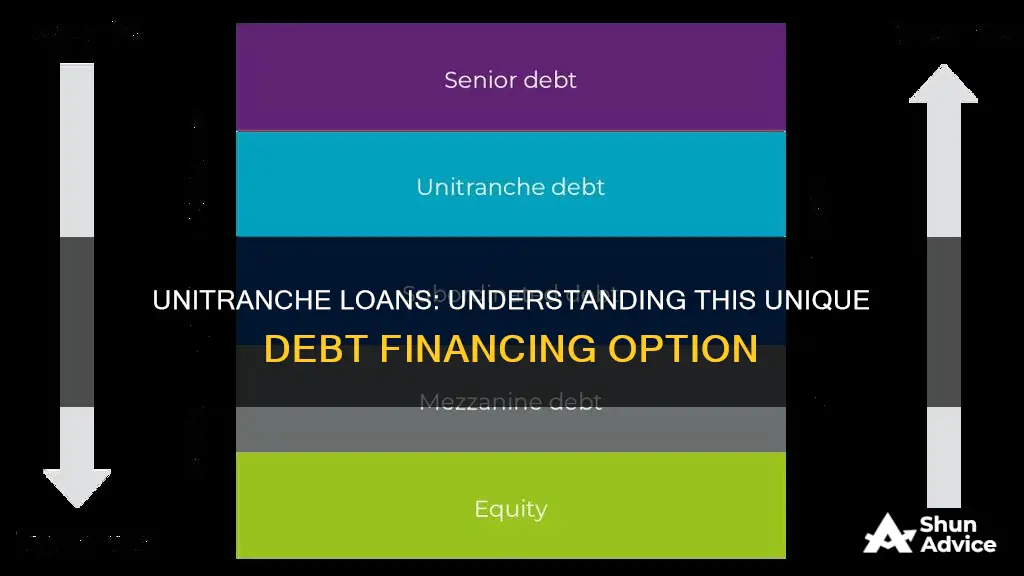

The primary focus of unitranche debt is on priority repayment levels for the borrowers. Levels of risk can vary in a structured unitranche debt deal, with borrowers agreeing to various priority levels for repayment in case of default. Underwriters structure the tranches by seniority, with the lowest-risk tranches having the highest seniority for repayment in the event of default. These tranches are known as "secured tranches".

Unitranche financing usually requires a one-time lump-sum repayment of the entire loan at maturity. One of the benefits of unitranche financing is its simplicity compared to traditional credit facilities. Borrowers go through a single approval process and prepare one set of documents for the lenders. This reduces the number of legal reports the borrower needs to prepare. Due to this simplicity, borrowers are often willing to pay a premium fee above what they would have paid to a traditional financial institution.

Unitranche loans are typically attractive to middle-market borrowers with annual sales of less than $100 million and an EBITDA of less than $50 million. The average size of a unitranche loan is $100 million, and it is often used to finance leveraged buyouts, private equity acquisitions, and dividend recapitalizations.

Becoming a Loan Signing Agent: Florida's Requirements

You may want to see also

![]()

They are used by mid-sized companies

Unitranche loans are a hybrid model that combines different loans into one, with a blended interest rate for the borrower that sits between the highest and lowest rate on the individual loans. They are often used by mid-sized companies to help fund acquisitions or ownership transitions. This form of financing is particularly attractive to middle-market borrowers with annual sales of less than $100 million and an EBITDA of less than $50 million.

Unitranche financing simplifies the complex structures of traditional acquisition financing, which involves multiple loans from various lenders, including both senior and subordinate debt, each with its own credit agreement, security and covenants. With unitranche financing, all of these elements are blended together into a single loan from a single financial institution. This means borrowers only go through a single process of approval and prepare one set of documents for the lenders. This simplicity means borrowers are often willing to pay a premium fee for unitranche financing.

The flexibility of unitranche financing means it can be adapted to a business's unique cash flow profile. It also provides certainty of closure when working with tight timelines, which is particularly valuable in an acquisition scenario where exclusivity periods often create time pressures. Unitranche financing can also be set up within relatively tight time frames, which is another reason for its popularity among mid-sized companies.

Unitranche financing first appeared in the first decade of the 21st century and gained popularity after the 2007-2008 financial crisis, when troubled companies were unable to access loan facilities from traditional lenders. The main providers of unitranche financing are non-traditional lending entities such as debt funds and other institutional lenders.

![]()

They are a flexible form of financing

Unitranche financing is a flexible form of financing. It is a hybrid model that combines different loans into one, with a blended interest rate that sits between the highest and lowest rates of the individual loans. This form of financing is particularly attractive to middle-market borrowers with annual sales of less than $100 million and an EBITDA of less than $50 million. The average size of a unitranche loan is $100 million, and it is often used to finance leveraged buyouts and acquisitions.

The main goal of unitranche financing is to make debt financing terms flexible and increase access to capital for companies. It simplifies complex structures by blending everything into a single loan from a single financial institution. This means that borrowers only go through a single approval process and prepare one set of documents for the lenders, reducing the number of legal reports required. The repayment structure can also be adapted to the unique cash flow profile of the business.

Unitranche financing can be particularly valuable in acquisition scenarios with tight timelines, as it provides certainty of closure. It is also a good option for companies that may have difficulty securing a traditional bank loan or are looking for accelerated funding. Many banks will participate directly in a unitranche loan, especially when it involves companies in industries where the bank has extensive experience. They can also provide traditional banking services in addition to these loans.

The unitranche market has grown in popularity, and more borrowers are using these loans to secure growth capital. This form of lending was especially popular during the financial crisis and the ensuing credit crunch when troubled companies were unable to access loan facilities from mainstream lenders.

![]()

Unitranche loans are a type of hybrid loan

Unitranche financing involves a single credit agreement and a single set of collateral documents, reducing the amount of paperwork for borrowers compared to traditional leveraged financing. It also simplifies complex structures by blending different types of secured and unsecured debt into one loan with a predictable repayment schedule, giving businesses maximum flexibility. This form of financing is particularly attractive to middle-market borrowers with annual sales of less than $100 million and an EBITDA of less than $50 million.

The average size of a unitranche loan is $100 million, and it is commonly used to finance leveraged buyouts, private equity acquisitions, and ownership transitions. Unitranche loans can be set up within tight time frames and are often used when funding needs are time-sensitive. They provide certainty of closure, which is valuable in acquisition scenarios with exclusive periods and tight timelines.

While unitranche financing offers benefits such as simplicity and flexibility, it may not be suitable for every company or scenario. Companies considering unitranche financing should carefully evaluate its impact on their capital structure and funding sources.

![]()

They are an alternative to syndicated loans

Unitranche loans are an alternative to syndicated loans. They are a hybrid model that combines different loans into one, with a blended interest rate for the borrower that sits between the highest and lowest rate on the individual loans. This blended rate is typically higher than traditional loan terms. Unitranche loans are usually provided by non-traditional lending entities such as debt funds and other institutional lenders, and they are mainly used in institutional funding deals.

The unitranche structure combines senior debt and subordinated debt into a single, flexible loan. This allows banks to compete better against private debt funds. The borrower only has to go through a single approval process and prepare one set of documents for the lenders, which can result in a quicker deal closure. The unitranche model also allows the borrower to access the funds of multiple parties, which can result in decreased costs from multiple issuances.

Unitranche loans are often used to finance leveraged buyouts such as management buyouts and private equity acquisitions. They are targeted at companies that lack access to traditional financial institutions, with the average loan size being around $100 million. These companies often have sales of less than $100 million and an EBITDA of less than $50 million. Unitranche loans are particularly attractive to borrowers with time-sensitive transactions who are willing to pay a premium for a single approval process.

Compared to syndicated loans, unitranche loans are more complex in their structuring. The primary focus of unitranche debt is on priority repayment levels for the borrowers, with varying levels of risk. In the case of default, borrowers agree to various priority levels for repayment. Structured unitranche debt is divided into tranches, each with its own class designation.

Frequently asked questions

A unitranche loan is a hybrid loan structure that combines senior and subordinated debt into a single loan with a blended interest rate.

The average size of a unitranche loan is $100 million, with loans typically ranging from $100 to $200 million.

Unitranche loans are attractive to middle-market borrowers who may have difficulty securing a traditional bank loan. They offer a streamlined solution with a single approval process, reduced paperwork, and flexible debt-financing terms.

Unitranche loans may not be suitable for every company and scenario. They can be complex, with varying levels of risk and priority repayment levels in case of default.

Unitranche loans are typically provided by non-traditional lending entities such as debt funds and institutional lenders. These lenders focus on acquisition finance and middle-market lending.