The average savings in the United States varies depending on factors such as age, household size, race, education level, and homeownership status. According to the Federal Reserve's 2022 Survey of Consumer Finances, the average American family has $62,410 in savings across various accounts, including savings, checking, money market, and prepaid cards. However, this number does not include investment or retirement accounts. When considering all types of accounts, the average retirement savings for all American families was $333,940 in 2022, with older Americans tending to have higher savings.

What You'll Learn

![]()

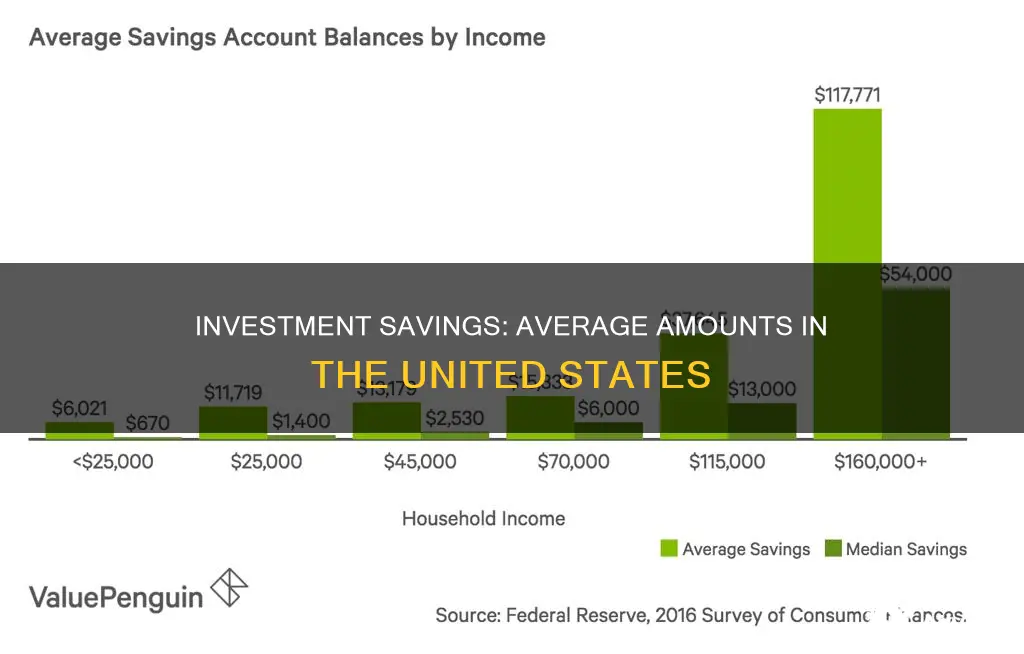

Average savings by age

The amount of money a person should have in savings depends on their financial needs, lifestyle, income, expenses, and specific situation. A popular guideline for emergency savings is to set aside three to six months' worth of essential expenses.

According to the Federal Reserve's most recent Survey of Consumer Finances, the average transaction account balance was $62,410 in 2022. The median balance for transaction accounts, which may be more indicative of the average American, was $8,000.

The Federal Reserve groups data on savings and financial assets for Americans under 35. The average savings for this age group is $20,540, with a median of $5,400. It is common to have modest savings in your 20s due to lower salaries, paying off student loans, or other financial obligations.

Similar to the previous age group, the Federal Reserve includes 30-year-olds in the under-35 category. The average savings remain at $20,540, with a median of $5,400. By this age, individuals may have progressed in their careers, paid off student loans, or moved into higher-paying jobs, allowing them to build their savings.

The Federal Reserve's data for this age group, which includes individuals ages 35 to 44, shows an increase in average savings to $41,540, with a median of $7,500. By their 40s, people often enter their peak earning years and may have more financial flexibility to save and invest.

According to the Federal Reserve Board Survey of Consumer Finances, the median savings balance, excluding retirement funds, for Americans in this age group is $6,400.

The Federal Reserve's data shows that U.S. residents aged 65 to 74 have an average of $609,230 in retirement savings. Those 75 and older have an average of $462,410.

It is important to note that these averages may not be entirely reflective of an individual's specific situation, and saving strategies should be tailored to one's unique financial goals and circumstances.

Investing Young: Better Than Saving?

You may want to see also

![]()

Average savings by household size

Household size and composition play a significant role in determining average savings in the United States. Here is an analysis of average savings by household size:

Single-Person Households

Single-person households, particularly those led by young adults, tend to have lower savings. According to the Federal Reserve's data, the median transaction account balance for individuals under 35 is $5,400. This includes checking, savings, and other accounts. The average savings for this age group are $20,540, with a median of $5,400. It is important to note that many individuals in this age group are still in college or starting their careers, which can impact their savings capacity.

Two-Person Households

As the household size increases, the savings tend to grow. For individuals between the ages of 35 and 44, the median transaction account balance rises to $7,500. This may include couples or roommates sharing finances. The average savings for this age group remain at $20,540, indicating that some individuals in this group may have higher savings to offset the lower savings of others.

Larger Households

For households with three or more members, the savings can vary significantly depending on factors such as income, age, and expenses. However, as a general trend, older Americans tend to have higher savings. For instance, individuals between 45 and 54 have a median transaction account balance of $8,700, while those between 55 and 64 have a median of $8,000.

Households with Children

The presence of children in a household can significantly impact savings. According to a survey by Forbes Advisor, 28% of Americans across generations have savings below $1,000. This includes 32% of Gen Zers, who are often starting their independent lives and may have student loans or other financial commitments.

Racial Disparities

It is important to note that there are racial disparities in savings rates. White, non-Hispanic Americans have a significantly higher median transaction account balance of $12,000, compared to $2,110 for Black, non-Hispanic Americans and $2,100 for Hispanic Americans. These disparities are long-standing, with minimal changes in account balances for Black and Hispanic Americans over the past 30 years.

In summary, average savings in the United States vary by household size, age, income, and race. While younger individuals tend to have lower savings, older Americans, particularly those in their peak earning years, have higher savings capacities. Additionally, racial disparities play a significant role, with White Americans having higher median savings compared to Black and Hispanic Americans.

Savings and Planned Investments: What's the Difference?

You may want to see also

![]()

Average savings by race

These disparities in savings account balances are indicative of broader racial wealth inequalities. White families have a median net worth that is over five times higher than that of Black and Hispanic families. In 2022, the median net worth of white families was $284,310, compared to $62,120 for Hispanic families and $44,100 for Black families.

The racial wealth gap cannot be fully explained by income and demographic factors. Even after controlling for these variables, the wealth gap remains significant. This suggests that factors such as saving behavior, investment choices, and intergenerational wealth transfer may contribute to the disparities.

It is worth noting that the median savings account balance for all families in the U.S. was $8,000 in 2022, which may be insufficient for covering expenses in the event of a financial emergency. Financial experts generally recommend having savings equivalent to three to six months' worth of living expenses.

CDs: Macroeconomics Investment or Savings Strategy?

You may want to see also

![]()

Average savings by education level

The average savings balance varies in the United States depending on several factors, including education level. According to the Federal Reserve's 2022 Survey of Consumer Finances, people with higher education levels tend to have higher average savings balances.

- No high school diploma: $900 median transaction account balance.

- High school diploma: $3,030 median transaction account balance, which is more than double that of those without a high school education.

- Some college but no degree: $5,200 median transaction account balance.

- College degree: $23,370 median transaction account balance, which is about five times greater than that of someone with a high school diploma.

The data suggests that higher levels of education are associated with higher savings balances. Americans with college degrees have significantly higher median transaction account balances compared to those without a college education.

It is important to note that other factors, such as age, income, race, and household size, also influence the average savings balance in the United States. Additionally, the data represents an average of high-income and low-income families and does not include investment balances or equity held in real property.

Graph Savings: A Smart Investment Strategy?

You may want to see also

![]()

Average savings by homeownership status

The average savings balance for Americans varies depending on several factors, including age, household size, race, and education level. According to the Federal Reserve's 2022 Survey of Consumer Finances, the average American family has $62,410 in savings across savings accounts, checking accounts, money market accounts, call deposit accounts, and prepaid cards. This figure does not include investment balances or equity held in real property.

When it comes to average savings by homeownership status, the data suggests that people who own homes tend to save more and have more cash in the bank than those who rent. However, it is important to note that the data on homeownership status may not be directly comparable to the data on savings balances, as the information on savings does not factor in investment or retirement accounts.

Homeownership rates in the United States have fluctuated over time, with a decline from 69% in 2004 to 63.4% in 2016 due to the Great Recession. As of the second quarter of 2024, the homeownership rate in the US was 65.6%. The homeownership rate among young adults (under 35) has declined from 45% in 1990 to 39% in 2022. The typical first-time homebuyer was 35 years old in 2023, and 56% of millennial homeowners have some regrets about purchasing their homes, mainly due to maintenance and hidden costs.

The data also shows that homeowners in the United States tend to have higher incomes. Married couples are the largest group of homeowners, followed by single women. White households have the highest rates of homeownership at 74.3%, while African Americans have the lowest rate at 45.7%. Homeownership rates are also correlated with higher education attainment.

In summary, while the average savings balance for Americans varies based on multiple factors, homeownership status appears to be one factor that influences savings. People who own homes tend to have higher incomes and, therefore, may have more financial resources to allocate towards savings. However, it is important to consider that the data on savings balances may not capture the full financial picture, especially for homeowners, as it excludes investment and retirement accounts.

Invest Your Savings: Safe Strategies for Beginners

You may want to see also

Frequently asked questions

The average savings account balance among Americans varies by numerous factors, like age, household size, race, education level, and homeownership status. The average American family has $62,410 in transaction accounts, according to data from the Federal Reserve's 2022 Survey of Consumer Finances.

According to a 2024 survey, 28% of Americans across all four generations currently have less than $1,000 in personal savings, including emergency funds, non-workplace retirement accounts, and investments.

The average retirement savings for all families was $333,940, according to the Federal Reserve's 2022 Survey of Consumer Finances. However, this amount varies by age, with those aged 55 and above having the most in their accounts.

The average savings by age in the United States varies. For those under 35, the median transaction account balance is $5,400. This rises to $7,500 for those between 35 and 44, $8,700 for those 45 to 54, $8,000 for those 55 to 64, $13,400 for those 65 to 74, and $10,000 for those 75 and older.

In May 2024, the personal savings rate in the United States was 3.9%. This includes general savings and other types of savings, such as retirement.