Retirement investments are a popular way to save for the future, but what is the typical interest rate? The answer depends on your individual investment portfolio and your risk tolerance. For example, a 60/40 portfolio (60% stocks, 40% bonds) has a 30-year average annual return of 8.28%, or 5.42% adjusted for inflation. However, some experts suggest that a 12% annual rate of return is possible, while others recommend a more conservative estimate of 5%. It's important to consider your own financial situation and goals when deciding how much to invest and what interest rate to expect.

| Characteristics | Values |

|---|---|

| Typical interest rate for retirement investments | 6.5% (before inflation) |

| Typical interest rate for a 60/40 portfolio | 8.28% (30-year average annual return) or 5.42% (adjusted for inflation) |

| Conservative estimate | 5% |

| Aggressive investor estimate | 10% |

| Unrealistic estimate | 12% |

What You'll Learn

![]()

A 60/40 portfolio

The typical interest rate for retirement investments depends on your risk tolerance and investment strategy. For example, if you're an aggressive investor with a portfolio that's 90% to 100% stocks, a 10% estimated rate of return makes sense.

However, it's important to note that the 60/40 portfolio has fallen out of favour recently due to the poor performance of bonds in the current high-interest-rate environment. When choosing an investment strategy, it's crucial to consider your individual circumstances and goals, as well as the potential risks and rewards of different investment options.

While a 12% annual rate of return has been suggested as a possibility, experts caution that this may not always be achievable. They recommend anticipating a more conservative return to account for life's unexpected events. For example, Fidelity provides a balance projection for a NetBenefits account holder's next milestone age that anticipates a 3.5% return.

When planning for retirement, it's essential to consider various factors, including your expected expenses, the average annual inflation rate, and your Social Security income. It's also crucial to regularly review and adjust your investment strategy as needed to ensure you're on track to meet your retirement goals.

Understanding Investment Interest Charges: Strategies for Success

You may want to see also

![]()

A 70/30 portfolio

The typical interest rate for retirement investments depends on the individual's risk tolerance and investment strategy. For example, if you are an aggressive investor with a portfolio that is 90% to 100% stocks, a 10% estimated rate of return makes sense.

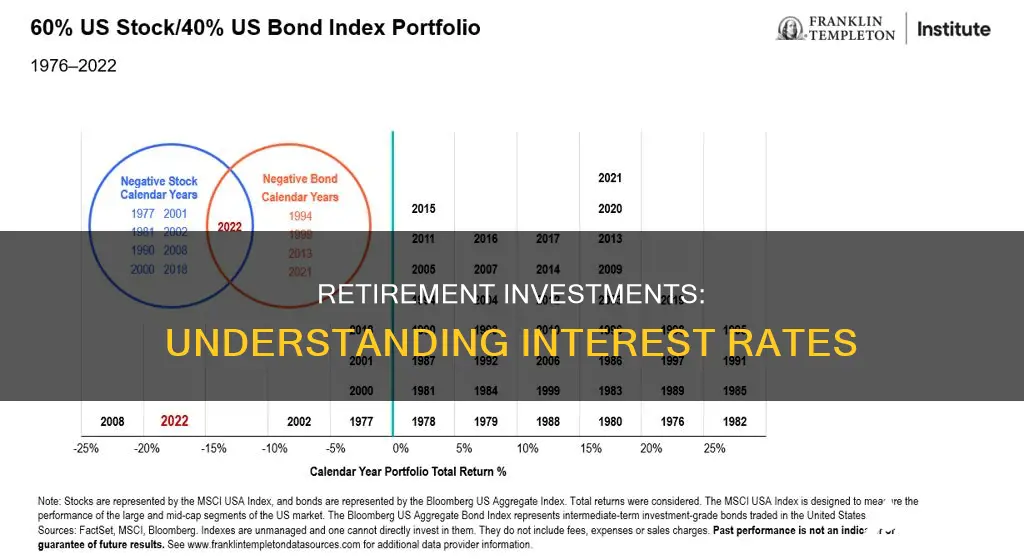

A more typical example of how many people invest for retirement is a 60/40 portfolio, which balances the high risk and higher rewards of stock investing with lower-risk but lower-return bonds. As of April 30, 2024, the 30-year average annual return of a 60/40 portfolio stands at 8.28%, or 5.42% adjusted for inflation.

It is important to be mindful of how anticipated rates of return are determined. For example, Fidelity provides a balance projection for a NetBenefits accountholder's next milestone age that anticipates a 3.5% return. Experts suggest that a 12% annual rate of return is not always achievable and that a more conservative return should be anticipated to account for life's inevitable curveballs.

The Magic of Compound Interest for Long-Term Investments

You may want to see also

![]()

A 15/75/10 portfolio

The typical interest rate for retirement investments depends on the individual's risk tolerance and investment strategy. For example, if you are an aggressive investor with a portfolio that is 90% to 100% stocks, a 10% estimated rate of return makes sense. On the other hand, if you have a more conservative portfolio, such as a 60/40 split between stocks and bonds, you can expect a lower rate of return, around 5.42% adjusted for inflation.

The interest rate for a 15/75/10 portfolio will likely fall within the range of 3.5% to 5%, which is considered a conservative estimate by experts. This rate takes into account the current high-interest-rate environment, which has caused bonds to perform poorly.

It's important to note that the actual rate of return for this portfolio may vary depending on various factors, such as the specific investments chosen, the economic conditions, and the time horizon of the investment. Additionally, it's crucial to regularly review and rebalance your portfolio to ensure it aligns with your retirement goals and risk tolerance.

When considering retirement investments, it's always recommended to seek professional financial advice and thoroughly assess your personal circumstances, including your risk tolerance and financial goals.

Understanding Investment Interest and Dividends: What's the Difference?

You may want to see also

![]()

A 12% annual rate of return

While a 12% annual rate of return has been suggested as a possible retirement investment, it is not always achievable. Experts have called this assumption 'absolutely nuts'.

The annual rate of return is defined as the percentage change in an investment's value. It is an estimate of the gains you may earn over time. The two different returns Orman cites serve different purposes. The first example, with a 12% average rate of return, is to illustrate the power of compounding. The second is a lesson to anticipate a conservative return, "because you never know what can happen in life". Orman's conservative estimate is in line with Blanchett's 5%.

The biggest individual factor in the estimated rate of return is your risk tolerance and investment strategy. If you are an aggressive investor and plan to stay invested in 90% to 100% stocks, a 10% estimated rate of return makes sense. If you are more conservative, a 60/40 portfolio of stocks and bonds is popular. As of April 30, 2024, the 30-year average annual return of a 60/40 portfolio stands at 8.28%, or 5.42% adjusted for inflation.

It is important to be mindful of how those anticipated rates of return are determined. For example, Fidelity provides a balance projection for a NetBenefits accountholder's next milestone age that anticipates a 3.5% return, among other assumptions. When calculating how much money you need to save for retirement, you must also estimate how much you think you'll spend, the average annual inflation rate, and how much money you expect to get from Social Security.

Investing During a Fed Interest Rate Cut: A Guide

You may want to see also

![]()

A 5.42% rate of return

It's important to note that the estimated rate of return for retirement investments can vary depending on individual factors such as risk tolerance and investment strategy. For example, an aggressive investor with a portfolio that is 90% to 100% stocks may expect a 10% rate of return, while a more conservative investor may anticipate a 3.5% to 5% return.

When planning for retirement, it's crucial to consider factors such as how much you think you'll spend, the average annual inflation rate, and how much money you expect to receive from Social Security. Using an estimated rate of return that is higher than reality can lead to insufficient savings and financial difficulties in retirement.

While a 12% annual rate of return has been suggested as a possibility, experts caution that this may not always be achievable and recommend anticipating a more conservative return to account for life's unexpected events.

No-Risk Investments: 5% Interest Payouts?

You may want to see also

Frequently asked questions

The typical interest rate for retirement investments depends on the type of portfolio you choose. A 60/40 portfolio, which is 60% diversified stocks and 40% bonds, is a popular choice as it balances high risk with higher rewards. As of April 30, 2024, the 30-year average annual return of a 60/40 portfolio was 8.28%, or 5.42% adjusted for inflation.

A conservative estimate for the interest rate on retirement investments is around 6%. This is based on historic stock market returns, which average 10%.

An aggressive estimate for the interest rate on retirement investments is around 12%. However, this may not always be achievable and it is important to consider the risks involved.

When choosing the right interest rate for your retirement investments, it is important to consider your risk tolerance and investment horizon. If you have a long time horizon, you may be able to take on more risk within your portfolio. Additionally, you should estimate how much you think you will spend in retirement, the average annual inflation rate, and your expected income from Social Security.