Amortizing a loan is a way to gradually pay it off through a series of fixed payments over time. The most common way to do this is to make a single fixed payment every period, which includes both interest and principal. There are several ways to amortize a loan, including paying the interest each period plus a fixed amount of the principal, paying principal and interest every period in a fixed payment, and paying only interest every period and paying off the principal at maturity. Amortization schedules typically only work for fixed-rate loans and not adjustable-rate mortgages, variable-rate loans, or lines of credit.

| Characteristics | Values |

|---|---|

| Type of loan | Amortized loan |

| Repayment method | Scheduled, periodic payments |

| Payment allocation | Interest and principal |

| Payment frequency | Monthly |

| Payment amount | Fixed |

| Payment structure | Interest and principal in one lump sum or interest each period plus a fixed amount of the principal |

| Early repayment | Possible, but check for early payoff penalty fees |

What You'll Learn

![]()

Pay interest and a fixed amount of principal

Paying a fixed amount of interest and principal is a classic example of amortizing a loan. This method involves making regular payments that cover both the interest and a portion of the principal, allowing the loan to be paid off completely by the end of its term. Each payment includes both interest and a portion of the principal, gradually reducing the loan balance over time.

In this scenario, the borrower makes periodic payments that are applied to both the loan's principal amount and the interest accrued. The payment first covers the interest expense for the period, and the remainder is then put toward reducing the principal amount. As the interest portion of the payments decreases, the principal portion increases, creating an inverse relationship within the payments over the life of the loan.

The amortization schedule for a loan with fixed payments of interest and principal can be calculated using a series of steps. First, the current balance of the loan is multiplied by the interest rate for the current period to determine the interest due. Next, this interest amount is subtracted from the total monthly payment to find the dollar amount of principal paid for that period. This amount is then subtracted from the outstanding balance of the loan to arrive at the new balance.

By following this amortization schedule, borrowers can gradually pay off their loans through a series of fixed payments over time. The interest portion of the payment is initially larger due to the higher loan balance, but it decreases over time as the principal portion increases. This allows borrowers to chip away at the principal, paying less towards interest and more towards reducing the principal with each payment until the loan is fully repaid.

Is Lavish Green Legit? A Comprehensive Review

You may want to see also

![]()

Pay principal and interest in fixed payments

Paying the principal and interest in fixed payments is a classic example of amortizing a loan. This method involves making regular payments that cover both the interest and a portion of the principal, allowing the loan to be paid off completely by the end of its term. The interest on an amortized loan is calculated based on the most recent ending balance of the loan, with the interest amount owed decreasing as payments are made.

When a borrower makes a loan payment, the payment is first applied to any outstanding interest charges. Once the interest charges are paid, the remaining amount is applied to the principal balance. This means that the principal balance decreases with each payment, which in turn reduces the amount of interest that accrues on the loan. By making additional principal payments, borrowers can reduce the overall cost of the loan and shorten the repayment period.

Amortization schedules are commonly used to outline how much of each payment goes towards the principal and interest. Initially, more of the payment may go towards interest, but as the loan approaches the end of its term, a larger portion of the payment will be applied to the principal. Borrowers can use amortization calculators to determine the breakdown of their loan payments and to make informed decisions about their loans.

Fixed-rate loans, which are commonly amortized, have a set interest rate throughout the life of the loan, meaning that the principal and interest payments remain the same. This provides borrowers with a predictable repayment plan and helps them budget their finances accordingly. However, it is important to note that factors such as property taxes or homeowners insurance premiums can cause the overall payment to change, even with a fixed-rate loan.

Grants vs Loans: Understanding the Key Differences

You may want to see also

![]()

Pay interest only and principal at maturity

Paying only the interest and the principal at maturity is one of the ways to amortize a loan. This method is different from the standard amortization process, where the principal amount is reduced over the life of the loan through periodic payments. In this case, the borrower pays only the interest every period and the principal amount remains the same. The principal is then paid off in full at the end of the loan's term, also known as the maturity date.

The maturity date for loans and other debt instruments is the agreed-upon date when the investment ends and the loan is repaid. This date can change if the borrower renews the loan, defaults, or repays the total debt early. At maturity, the borrower is required to repay the full amount of the outstanding principal, plus any applicable interest. Non-payment at maturity can lead to default, negatively impacting the borrower's credit rating and ability to secure funds in the future.

The interest-only repayment method has some advantages and disadvantages. One benefit is that interest-only repayments are lower during the interest-only period, providing some flexibility for the borrower. However, over the life of the loan, the borrower will end up paying more interest overall. There is also the risk of the asset that the loan is financing, such as a home or investment property, declining in value during the interest-only period. This could result in the borrower owing more than the asset is worth and ending up with no equity.

It is important to note that this method of repayment may not be considered true amortization, as the principal is not being paid down during the loan term. Amortization is a debt repayment strategy where consistent principal and interest payments are made over time, with the goal of paying off the loan in full by the maturity date. In the case of paying only interest and the principal at maturity, the principal is not reduced through periodic payments, which is a key characteristic of amortized loans.

Motive Loan: Safe or Risky Option?

You may want to see also

![]()

Pay off early with frequent payments

Paying off an amortized loan early can be achieved by making more frequent payments. This can be done by paying half of the monthly payment every two weeks, which equates to 13 monthly payments per year instead of 12. This method can significantly reduce the total loan term and the amount of interest paid. For example, if you have a 30-year fixed-rate mortgage of $200,000 with an interest rate of 4% and a monthly payment of $955, paying an extra $100 towards the principal every month can reduce the loan term by over 4.5 years and the interest paid by more than $26,500. Increasing the extra payment to $200 per month can cut the loan term by more than 8 years and the interest paid by over $44,000.

Making more frequent payments can be an effective strategy to pay off an amortized loan early. This is because amortized loans are structured so that the interest portion of the payments decreases over time, while the principal portion increases. By making extra payments, you can reduce the principal amount on which interest is charged, thereby lowering the overall interest that accrues on the loan. This strategy can be particularly beneficial for loans with a long duration, such as 15- or 30-year fixed-rate loans, as it can help you save a significant amount of money in the long run.

It is important to note that not all lenders allow early payoff without penalties. Before making extra payments towards your loan, it is advisable to review your loan agreement to check for any early payoff penalty fees. Additionally, it is crucial to ensure that your budget can accommodate the increased payment frequency. While making more frequent payments can help you pay off your loan faster, it is important to balance this strategy with your other financial goals and obligations.

Overall, paying off an amortized loan early by making more frequent payments can be a powerful way to reduce the total cost of the loan and shorten the loan term. By understanding the structure of amortized loans and the impact of extra payments, borrowers can make informed decisions about their loan repayment strategy and achieve their financial goals more quickly.

Understanding Per Diem Interest on Loan Payoffs

You may want to see also

![]()

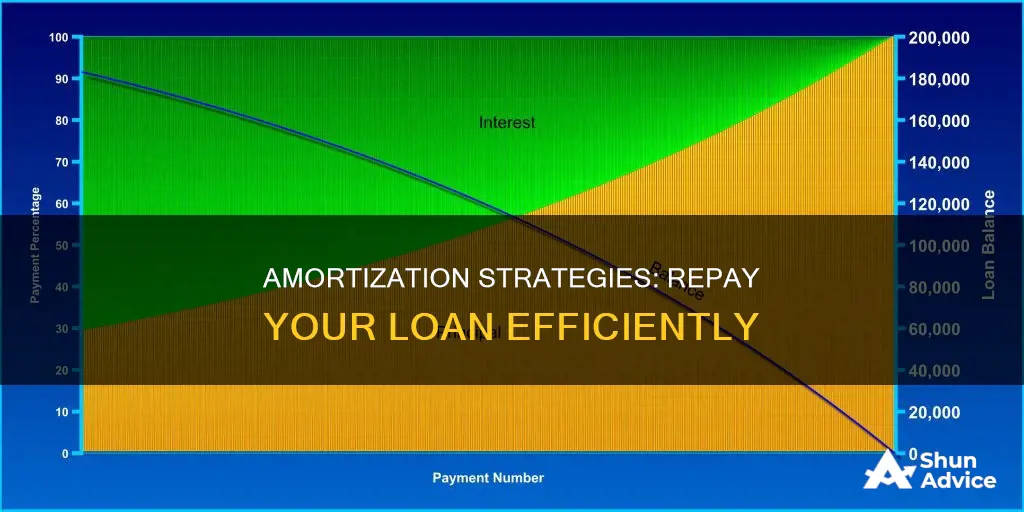

Amortization schedules for fixed-rate loans

Amortization schedules are an essential tool for managing fixed-rate loans, providing a clear roadmap for borrowers to understand their repayment strategy. These schedules are structured as tables, detailing the periodic payments required to chip away at the loan's balance over time. They are generally used for fixed-rate loans and not for adjustable-rate mortgages, variable-rate loans, or lines of credit.

To create an amortization schedule for a fixed-rate loan, you need the loan's term, interest rate, and dollar amount. With this information, a comprehensive schedule of payments can be calculated. This process is quite straightforward for fixed-rate mortgages, as the loan's total term is usually known from the outset, often being set at 30 years.

The amortization schedule will outline the periodic interest charges and the portion of each payment that goes towards the principal amount. As the loan is repaid, the composition of each payment changes, with the interest portion decreasing and the principal portion increasing. This inverse relationship ensures that the loan is paid off completely by the end of its term.

Borrowers can use these schedules to their advantage by making extra payments towards their loans, even though basic amortization schedules may not account for this. By paying more frequently or making principal-only payments, borrowers can reduce the amount that accrues interest, helping them save money in the long run. However, it is essential to check the loan agreement beforehand to avoid any early payoff penalty fees.

Understanding Loan-to-Cost Ratios: A Crucial Financial Concept

You may want to see also

Frequently asked questions

An amortized loan is a type of loan with scheduled, periodic payments that are applied to both the loan's principal amount and the interest accrued.

The ways to amortize a loan include paying the interest each period plus a fixed amount of the principal and paying principal and interest every period in a fixed payment.

Yes, you can pay off an amortized loan early by making payments more frequently or making principal-only payments.

Common amortized loans include auto loans, home loans, and personal loans from a bank for small projects or debt consolidation.

An amortization schedule is a table that lists relevant balances and dollar amounts for each period. It includes the payment date, principal portion of the payment, interest portion of the payment, total interest paid to date, and ending outstanding balance.