Fees are an important consideration when it comes to retirement investments. While they are necessary to ensure your investments are managed effectively, they can also significantly impact your wealth and returns over time. Even small fees, such as a 1% investment fee, can compound over the years and result in a substantial reduction in your overall portfolio value. Therefore, it is crucial to understand the different types of fees associated with retirement plans, such as 401(k) plans, and to carefully evaluate their potential impact on your long-term savings. By proactively managing and minimising fees, you can maximise your retirement savings and take a significant step towards achieving your financial goals.

| Characteristics | Values |

|---|---|

| Impact of fees | Even small fees can have a huge impact on your wealth over time. |

| High fees and returns | Studies show that higher fees do not generate better returns. |

| Types of fees | Ongoing fees, trading fees, loads, management fees, advisory fees, broker fees, transaction fees, purchase fees, account fees, etc. |

| Average fees | 401(k) fees can range from 0.5% to 2% or higher, with an average of 1%. |

| Hidden fees | Fees might be hidden or overlooked, but they are disclosed in the prospectus. |

| Fee reduction | Actively managed mutual funds charge higher fees than passively managed funds or ETFs. |

What You'll Learn

![]()

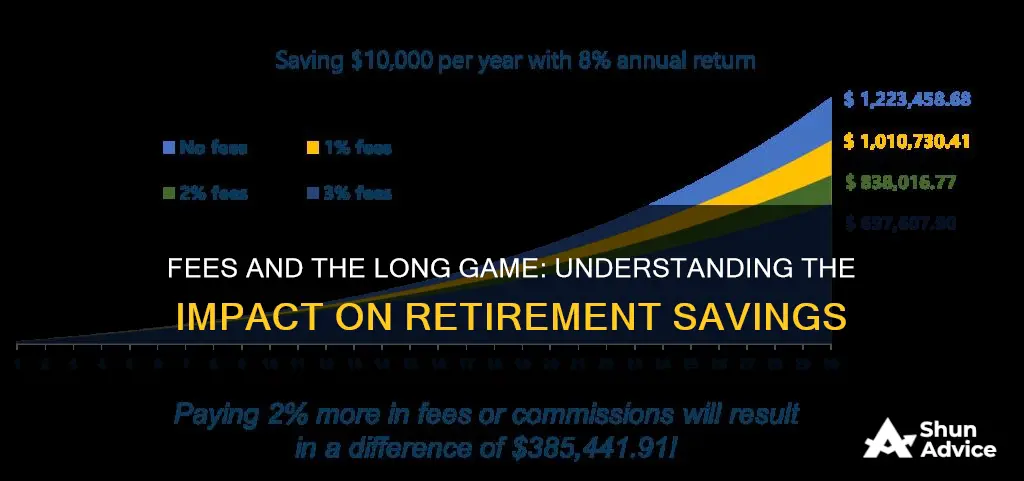

Even small fees can significantly reduce your retirement portfolio

Investment fees cover important costs to ensure your investments are managed well, but they can also have a big impact on your investment performance over the long run. Even a 1% fee, over a lifetime of investing, can significantly reduce the value of a portfolio.

For example, let's say you invest $1,000 a month over a 40-year career. Without any fees, this portfolio could grow to about $5.8 million. Now, let's assume you pay an advisor 1% of your investments for their services, a standard fee in the industry. This reduces your returns from 9.7% to 8.7%, resulting in a portfolio of just $4.3 million. That 1% fee cost you about $1.5 million, or 25% of your wealth.

If your advisor invests your money in mutual funds that also charge a 1% expense ratio, your wealth would further decrease to around $3.2 million. So, while paying a small investment fee here and there might not seem like a big deal, over time, they can significantly impact your investment performance.

Additionally, 401(k) plans often come with various fees that aren't always evident to the investor but can significantly impact returns over time. These fees can range from 0.5% to 2% or even higher, and they can add up quickly, especially for higher-income workers. For example, paying just 1% in fees over 40 years of saving can cost someone more than $590,000 in sacrificed returns.

Therefore, it's crucial to understand the fees associated with your investments and how they can affect your long-term returns. By being proactive and choosing low-cost funds, you can protect yourself from high fees and maximize your retirement savings.

Investing: Separating Fact from Fiction

You may want to see also

![]()

Fees can impact your wealth, but high fees don't generate better returns

Fees are an important consideration when it comes to retirement investments. While they are necessary to ensure your investments are well-managed, they can significantly impact your wealth over time.

Let's explore the impact of fees on your wealth and why higher fees don't necessarily translate to better returns.

The Impact of Fees on Your Wealth

Investment fees, although often small and easily overlooked, can have a substantial impact on your investment portfolio over the long term. These fees, which may include expense ratios, advisory fees, management fees, and transaction fees, can eat into your returns and reduce the overall value of your portfolio.

For example, consider an investment portfolio with an annual return of 10% and a fee of 1%. Over 40 years, this 1% fee would result in a loss of about $1.5 million compared to an investment with no fees. The impact of fees is so significant that even a 0.5% fee would reduce the final portfolio value by several hundred thousand dollars.

High Fees Don't Guarantee Better Returns

It's a common misconception that paying higher fees will lead to better investment returns. However, studies have shown that this is often not the case. Actively managed funds, which typically charge higher fees, have been found to underperform their respective indexes over the long term.

A study by S&P Global found that for a 10-year period, the majority of large-cap funds underperformed the S&P 500. Similar results were observed for mid-cap and small-cap funds, with a significant percentage underperforming their benchmarks over a 10-year period.

Additionally, Morningstar's research revealed that there is a relationship between low fees and higher investor returns. Their data showed that in the most expensive equity funds, investor returns lagged total returns by a larger margin compared to the least expensive funds.

Minimizing Fees

When it comes to investment fees, it's essential to remember that you don't always get what you pay for. Instead, focus on finding investments with low fees and strong track records of performance. Index funds, for example, tend to have lower fees than actively managed funds and can provide diverse investment options.

By minimizing investment fees, you keep more of your money working for you, allowing it to compound and grow over time. This can have a significant impact on your wealth, especially when investing for retirement.

In summary, while fees are an essential aspect of investing, they can impact your wealth significantly. Higher fees do not guarantee better returns, and it's crucial to make informed decisions about the fees you pay. By choosing investments with lower fees and strong performance, you can maximize your returns and work towards a more secure retirement.

Retired and Investing for Your Children: A Guide to Long-Term Planning

You may want to see also

![]()

How to determine the investment fees you're currently paying

Fees are an important consideration when it comes to retirement investments. Even small fees can compound over time and significantly eat into your returns. Therefore, it's crucial to understand the fees you're currently paying to make informed decisions about your investments. Here are some steps to determine the investment fees you're paying:

Advisory Fees:

Start by checking the fees charged by your financial advisor, if you have one. These fees should be disclosed in your investment statements, either in percentage terms or dollar amounts. If you're having trouble finding them, check your online account or search for public filings published with the Securities and Exchange Commission (SEC). Form ADV Part 2A will contain information about the fees charged by your advisor. Advisory fees typically range from 0.3% to 3% of total "assets under management".

Expense Ratios:

The next layer of fees to consider is related to your actual investments. These are often referred to as "expense ratios" and are charged by fund managers for their services. To find these fees, you can use a platform like Morningstar.com. Copy the ticker symbols of the funds within your portfolio and paste them into the search bar on Morningstar to find the expense ratios. Expense ratios can range from as low as 0.08% for an index fund to 2% for a mutual fund.

Trading/Transaction Fees:

Trading or transaction fees are charged when you buy or sell an investment, such as stocks, mutual funds, or ETFs. These fees can range from $5 to $50 or more per trade and can add up if you trade frequently. Some investment firms have eliminated trading fees, but be sure to check before opening an account.

Brokerage Fees:

Brokerage fees are incurred when you use a custodian or broker-dealer to facilitate investment activity or trades. These fees include trading fees, custody fees (for holding your investments), and service fees for account maintenance, transfers, wiring funds, etc. Custody fees can range from $20 to over $100 per year per account, while service fees can be anywhere from $5 to over $100 per transaction.

Financial Advisor Fees:

Financial advisor fees are usually based on the amount you invest and can range from 0.30% to over 1%. These are recurring fees that increase as your investments grow. You can find these fees in the account agreement you receive when establishing an account or in disclosure documents provided before purchasing an investment.

Management Fees:

Management fees are charged by professional money managers for selecting the stocks and bonds that make up mutual funds or ETFs. These fees are often referred to as "expense ratios" because they are expressed as a percentage of your investment. They won't show up on your account statement but can be found on the websites of the respective funds or ETFs.

Sales Loads and Commissions:

Sales loads and commissions are upfront fees charged when you purchase an investment product, typically an annuity or a mutual fund. Annuity commissions can range from 1% to 7%, while mutual fund sales charges can be as high as 5.75%.

Taxes:

While not technically a fee, taxes can impact your investment returns. Turnover, or the percentage of an investment that is replaced or sold in a given year, can trigger taxable events. Higher turnover can lead to higher taxes, reducing your overall returns.

By understanding and calculating these various fees, you can gain a clearer picture of the costs associated with your investments. This knowledge will enable you to make more informed decisions and potentially reduce the impact of fees on your retirement savings.

Investing: Wealth and Security

You may want to see also

![]()

How fees impact your investment and long-term value

Fees are an important consideration when investing for retirement. While they are necessary to ensure your investments are well-managed, they can also significantly impact your investment performance and long-term value. Even small fees can add up over time, reducing your overall returns and wealth.

There are various types of investment fees, including loads or sales commissions, management fees, advisory fees, broker fees, and trading fees. These fees can be structured as one-time charges or recurring fees that are charged as a percentage of the funds in your account. For example, a 1% fee charged by an advisor is standard in the industry, but it can reduce your portfolio value by tens of thousands of dollars over a lifetime of investing.

To illustrate the impact of fees, consider the following example: assume you invest $1,000 a month over a 40-year career, with an average annual rate of return of 9.7%. Without any fees, your portfolio would grow to about $5.8 million. However, if you pay a 1% advisor fee, your returns drop to 8.7%, resulting in a portfolio of $4.3 million. That 1% fee cost you $1.5 million, or 25% of your wealth.

Additionally, there are fees associated with the specific funds you invest in, such as mutual funds, which also charge expense ratios or management fees. These fees further eat into your returns. For instance, if the mutual funds in the above example also charged a 1% expense ratio, your wealth would further decrease to about $3.2 million.

When deciding on investments, it's crucial to consider the long-term impact of fees. While a 1% difference in fees might seem insignificant, it can make a substantial difference in the long run. As fees compound over time, they can significantly reduce your retirement savings, potentially forcing you to delay retirement. Therefore, it's essential to understand the fees associated with your investments and make informed decisions to protect your long-term value.

Life Annuities: Retirement Investment or Security Blanket?

You may want to see also

![]()

How to find hidden fees

Fees are an important consideration when it comes to retirement investments. Even small fees can have a significant impact on your wealth over time. While some fees are easily identifiable, others may be hidden or difficult to spot. Here are some ways to find hidden fees associated with retirement investments:

- Prospectus and Account Statements: The U.S. Department of Labor requires 401(k) providers to disclose all fees in a prospectus given to new investors when they enrol in a plan. This prospectus is updated annually and includes details such as Total Asset-Based Fees, Total Operating Expenses as a percentage, and Expense Ratios. Reviewing these documents carefully can help you identify various fees associated with your retirement plan.

- Expense Ratios: The expense ratio of a fund represents the percentage of assets deducted annually for fund management expenses. While this may be included in the prospectus, it is worth noting separately as it can have a significant impact on your returns. Expense ratios can range from 0.5% to 2% or higher, and choosing funds with lower expense ratios can help maximise your returns.

- 12b-1 Fees: Named after a section of the Investment Company Act of 1940, 12b-1 fees are charged by mutual funds or exchange-traded funds (ETFs) within your 401(k) plan. These fees are intended for marketing and distribution expenses and are capped at 0.75% of assets. Some funds also impose a 0.25% shareholder services fee.

- Transaction Fees: These fees are incurred when buying, selling, or exchanging shares of a stock or ETF. They can vary widely between companies and can quickly add up if you trade frequently. It is important to consider these fees when making investment decisions.

- Administrative Fees: Retirement accounts such as 401(k)s and IRAs often charge administrative fees to cover record-keeping, account maintenance, and customer service costs. These fees may be flat rates or based on a percentage of assets under management. While they may be disclosed in account statements, they can sometimes be overlooked.

- Advisory Fees: Financial advisors may charge fees based on a percentage of assets under management, an hourly rate, or a flat fee. These fees can be significant, especially for retirees who work with financial advisors or wealth management firms. It is important to understand the services provided and the value you are receiving for these fees.

- Annuity Fees: Annuities can come with various hidden fees, such as high commissions, surrender charges, insurance fees, investment management fees, and insurance rider fees. It is important to carefully review the terms and conditions of any annuity contract to identify potential hidden fees.

- Early Withdrawal Penalties: While not technically a hidden fee, it is important to be aware that withdrawing money from qualified retirement plans before the age of 59 1/2 will typically incur a 10% tax penalty on the taxable portion of the distribution.

- Utilise Tools: There are tools available, such as the Personal Capital Retirement Fee Analyzer, that can help you evaluate your investment costs. By connecting your investment accounts, these tools can determine the expense ratios of your investments and provide a weighted average expense ratio for your portfolio.

Unraveling the Mystery of Fidelity Investments' Payer Federal ID Number

You may want to see also

Frequently asked questions

Fees are important in relation to a retirement investment because they can have a huge impact on your wealth. Even a small percentage fee can significantly reduce the value of your portfolio over time.

There are two types of fees associated with retirement investments: ongoing fees and transaction fees. Ongoing fees are recurring charges that are usually calculated as a percentage of the funds in your account. Transaction fees are one-time charges that are typically a flat fee.

Retirement investment fees should be disclosed to you by the plan's administrator, who is often your employer. These disclosures are typically provided in a prospectus or other informational materials when you enrol in the plan. You can also find fee information on the administrator's website or in your quarterly statements.