The UK government's position on the VAT treatment of investment management fees has been a subject of debate in recent years, with some organisations treating them as a general overhead, which would allow a proportion of the VAT to be recovered. This issue has been the subject of litigation, with HMRC denying VAT recovery in many cases, arguing that these costs are directly related to VAT-exempt or non-business investment activity. The outcome of these disputes has significant implications for investment managers and their clients, as well as the competitiveness of the UK as a hub for the investment management industry.

What You'll Learn

![]()

Portfolio management services and VAT exemption

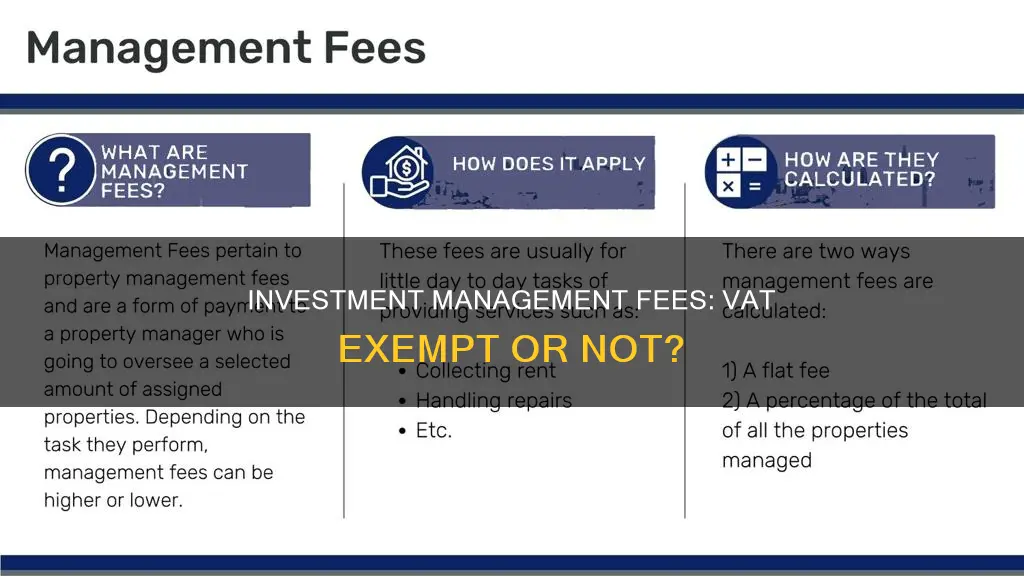

Portfolio management services that do not fall into the exemption for the management of special investment funds (SIFs) are subject to VAT. This means that VAT is due on the services of managers (sometimes referred to as 'wealth' or 'private client' managers) who manage the investment portfolios of individual clients.

Portfolio management services involve an ongoing commitment to monitor and manage an individual client's investment portfolio to formulate investment decisions or recommendations. This is what distinguishes them from advised sales services. They should also be distinguished from investment fund management services, where VAT exemption depends on the nature of the fund being managed.

Portfolio management can be provided on either a discretionary or advisory basis. If a manager contracts to act on a discretionary basis, the client authorises the manager to invest funds on their behalf as the manager sees fit, within pre-agreed parameters relating to risk exposure and the nature of the products invested in. When contracted on an advisory basis, the manager must refer back to the client before any investment transactions are undertaken.

In both instances, charges made by the manager for their management services to the client carry VAT at the standard rate. These include any charges described as annual management charges or performance charges. However, dealing fees/commissions that are charged strictly on a transaction-by-transaction basis are VAT exempt, provided they are specifically for the services of executing trades in exempt securities and are separately identified in any VAT invoice.

The European Court of Justice (ECJ) has issued rulings relevant to the VAT treatment of portfolio management services. For example, in the German Deutsche Bank case, the ECJ decided that a single annual portfolio management fee, which included a separately identified charge for buying and selling securities, was subject to VAT at the standard rate as a single taxable supply of services.

In another case, BlackRock Investment Management v HMRC, the Court of Justice of the European Union (CJEU) found that fees paid for the use of the Aladdin portfolio management platform were subject to VAT in their entirety, even when the platform was used to manage both SIFs and other types of funds. The CJEU rejected BlackRock's argument that VAT should be apportioned based on the proportion of non-SIF usage.

In addition, national courts and tax authorities, such as the Portuguese Tax Authorities (PTA), have issued rulings on the scope of VAT exemption for portfolio management services. The PTA has ruled that services such as ongoing management of investment fund assets, accounting, legal, and consulting services may be considered within the scope of VAT exemption if they are specific administrative services essential for the management of funds.

Rajiv Gandhi Equity Savings Scheme: A Smart Investment Move

You may want to see also

![]()

VAT on investment management fees and recoverability

The UK government has been reviewing the VAT treatment of fund management fees as part of a wider look at the UK funds regime. The review aims to "gather evidence and explore the attractiveness of the UK" as a base for asset management. Under the current system, VAT on investment management fees cannot be recovered.

Annual management charges levied by fund houses are currently free of VAT, but the fees paid by clients of discretionary fund management firms are subject to the tax. This is because portfolio management services that do not fall under the exemption for the management of special investment funds (SIFs) are considered taxable supplies.

The European Court of Justice (ECJ) confirmed in the German Deutsche Bank case that charges for the combined activities of managing a client's portfolio and executing exempt trades are liable to VAT at the standard rate. This applies even when the transaction charges are separately identified to the customer.

However, dealing fees/commissions charged strictly on a transaction-by-transaction basis specifically for the services of executing trades in exempt securities are VAT exempt, provided that they are directly linked to the sale and purchase of an investment product and are separately identified on any VAT invoice.

There has been uncertainty over the entitlement to recover VAT on investment management fees, with HMRC denying VAT recovery in many cases, arguing that these costs are directly related to VAT-exempt or non-business activities. Nevertheless, some organisations have sought to treat them as a general overhead, which would allow a portion of the VAT to be recovered.

The issue of VAT recoverability on investment management fees is currently the subject of litigation involving the University of Cambridge, a registered charity that undertakes both VAT-exempt and VAT-liable activities. The University argued that investment costs were incurred for the benefit of its business activities in general and not just to support an investment activity. The First-tier Tax Tribunal and Upper Tribunal ruled in favour of the University, meaning there is scope for charities to claim VAT on investment management costs according to their normal VAT recovery entitlement.

While there is no one-size-fits-all advice due to the inconsistency in the treatment of such expenditure by charities, organisations should review how they treat investment management costs to maximise available VAT recovery.

Savings and Investments: Economy's Growth Engine

You may want to see also

![]()

VAT treatment of fund management fees

The VAT treatment of fund management fees has been a subject of discussion between HMRC and several industry bodies. The current stance of HMRC is that the provision of research is a standard-rated supply. However, this stance has been challenged by Macfarlanes, which is advising on a case against HMRC.

In the Spring Statement, the Chancellor announced a review of the VAT treatment of fund management fees as part of a wider review of the UK funds regime. The review will cover direct and indirect tax, as well as relevant areas of regulation, with a view to considering policy changes. The government aims to make the UK a more attractive location for fund companies and help them compete post-Brexit.

Portfolio management services that do not fall under the exemption for the management of special investment funds (SIFs) are taxable supplies. VAT is due on the services of managers who manage the investment portfolios of individual clients. These managers are sometimes referred to as 'wealth' or 'private client' managers. Portfolio management services involve a continuous commitment to monitor and manage a client's investment portfolio to formulate investment decisions or recommendations. Charges made by the manager for management services, including annual management and performance charges, carry VAT at the standard rate.

Dealing fees/commissions charged strictly on a transaction-by-transaction basis for executing trades in exempt securities are VAT exempt, provided they are directly linked to the sale and purchase of an investment product and are separately identified on any VAT invoice. When a manager does not supply trade execution services on this basis and charges for the combined activities of managing a client's portfolio and executing exempt trades, those charges are liable to VAT at the standard rate.

In recent years, there has been uncertainty over the entitlement to recover VAT on investment management fees. HMRC has often denied VAT recovery, arguing that these costs are directly related to VAT-exempt or non-business investment activity. However, some organisations have treated them as a general overhead, allowing a proportion of the VAT to be recovered.

Crafting an Investment Offer: A Guide to Writing Portfolio Proposals

You may want to see also

![]()

VAT on fund fees and the UK's attractiveness as a base for asset management

The UK government has launched a review of the VAT treatment of fund management fees, as part of a wider review of the UK funds regime. The review will cover direct and indirect tax, as well as relevant areas of regulation, with a view to considering any necessary policy changes.

The government's stated intention is to make the UK a more attractive location for the establishment of funds and asset-holding vehicles. The review will begin with a consultation on tax liabilities, with the aim of making the UK a more appealing location for fund companies and helping them to compete post-Brexit.

The government has also set up a broader industry working group to review how financial services are treated for VAT purposes. This group will examine the financial services VAT exemptions more generally.

The current system does not allow for VAT on investment management fees to be recoverable. Charges made by the manager for their management services to the client carry VAT at the standard rate. This includes any charges described as annual management charges or performance charges.

However, dealing fees/commissions that are charged strictly on a transaction-by-transaction basis are VAT exempt, as long as they are directly linked to the sale and purchase of an investment product and are separately identified as such on any VAT invoice.

The government has stressed that it is not prepared to sacrifice its existing tax principles by taking significant sums of existing taxable income out of the scope of taxation. It will only make changes that offer clear benefits.

The funds trade body, the Investment Association (IA), has welcomed the initiative and looks forward to working with the government on the project. Chris Cummings, CEO of the IA, emphasised the importance of remaining competitive, stating that the UK is already a leading hub for the investment management industry.

Saving and Investment: Understanding the Fundamentals

You may want to see also

![]()

VAT on investment management fees for charities

Charities and other not-for-profit organisations currently treat investment management fees as a general overhead for VAT purposes, recovering the VAT paid using their annual recovery rate. However, there has been uncertainty over the entitlement to recover VAT on investment management fees. In many cases, HMRC has denied VAT recovery, arguing that these costs are directly related to the VAT-exempt or non-business activity of investment.

The issue of VAT on investment management fees for charities is currently the subject of litigation involving the University of Cambridge. The University, a registered charity, argued that it makes VAT-exempt supplies of education alongside commercial activities, such as research, publishing and consultancy, which are subject to VAT. Therefore, the University claimed it was entitled to recover a proportion of the VAT incurred on general overheads, including VAT on investment management fees. Both the First-tier Tax Tribunal and the Upper Tribunal ruled in favour of the University, deciding that the investment costs were incurred for the benefit of the University’s business activities in general, and not just to support an investment activity.

Subject to any successful appeal by HMRC, this means there is scope for charities to claim VAT on investment management costs, according to their normal entitlement to recover VAT under their business, non-business and partial exemption methods. However, it is important to note that the treatment of such expenditure by charities has been inconsistent, and each case should be reviewed individually. Charities should review how they treat investment management costs and take positive action to maximise available VAT recovery.

Understanding Cash in Your Investment Portfolio

You may want to see also

Frequently asked questions

Yes, VAT is due on the services of managers (sometimes referred to as 'wealth' or 'private client' managers') who manage the investment portfolios of individual clients.

Dealing fees/commissions that are charged strictly on a transaction-by-transaction basis (i.e. per purchase or sale of investments) specifically for the services of executing trades in exempt securities are VAT exempt.

In many cases, HMRC has denied VAT recovery, arguing that these costs are directly related to VAT-exempt or non-business activities. However, some organisations have sought to treat them as a general overhead, which would allow a proportion of the VAT to be recovered.