Foreclosure is a scary word for any homeowner, but it doesn't have to be inevitable. If you're struggling to make your mortgage payments, a loan modification may be an option to help you keep your home. Loan modifications are changes to the original terms of your mortgage, agreed upon between you and your lender, to make your payments more affordable. This could include reducing your interest rate, extending the term of your loan, or integrating missed payments into your remaining balance. However, it's important to remember that loan modifications can have disadvantages, such as potentially increasing the total amount you owe, and they may not be suitable for everyone. To determine if a loan modification is right for you, it's best to consult with a foreclosure defense attorney or a housing counselor approved by the Department of Housing and Urban Development (HUD). They can help you explore your options and protect your rights during this stressful time.

| Characteristics | Values |

|---|---|

| Can a loan modification stop foreclosure? | Yes, but the application must be submitted at least 45 days before the scheduled foreclosure sale of the home. |

| Who can a borrower talk to? | A mortgage law and foreclosure defense attorney is the best person to talk to when having problems paying a mortgage. |

| Who should a borrower avoid discussing loan modification with? | Anyone other than the mortgage lender. |

| What are the potential benefits of a loan modification? | Allowing the borrower to prevent foreclosure, staying in their home indefinitely, settling any payment delinquencies, reducing monthly payments, and affecting the borrower's credit rating less than a foreclosure would. |

| What are the disadvantages of a loan modification? | The possibility of the borrower ending up paying more over time to repay the loan. The total owed may even be more than the house is worth in some cases. The borrower may also pay extra fees to modify a loan or incur tax liability. The borrower's credit score may be impacted if the lender reports the modification as a debt settlement. |

| What are the eligibility requirements for a mortgage loan modification? | The home on the mortgage is the borrower's primary residence, and the borrower has enough income to afford payments under the modified terms of the loan. |

| What is the process of modifying a mortgage loan? | Reach out to the lender and explain the situation. Ask if the terms of the contract can be changed and provide proposed adjustments. Submit a completed loss mitigation application. |

| What documentation is required for a loan modification application? | Income and expenses information, bank statements, pay stubs, and tax returns. |

| What is Regulation X? | A federal law that prohibits mortgage lenders from conducting a foreclosure while a mortgage modification application is under consideration. |

What You'll Learn

![]()

Foreclosure alternatives

Foreclosure can be a stressful and overwhelming process, but there are alternatives to consider. Here are some options to explore:

Loan Modification

Loan modification is a common alternative to foreclosure, allowing you to stay in your home indefinitely. It involves negotiating with your lender to change the original terms of your loan, often resulting in reduced monthly payments. This can be achieved by lowering the interest rate, reducing the principal amount, or switching from an adjustable to a fixed-rate mortgage. It is important to note that loan modification may increase the total amount you owe over time and could impact your credit score. Therefore, it is recommended to consult a loan modification lawyer or a foreclosure defense attorney to review your options and assist with the application process.

Federal and State Programs

The Federal Housing Administration (FHA), part of the Department of Housing and Urban Development (HUD), offers loss mitigation programs and resources to help homeowners facing financial hardship or unemployment. Additionally, certain states like California, Colorado, Nevada, and Minnesota have passed laws that provide additional protections and incentives for mortgage servicers to work with homeowners to avoid foreclosure.

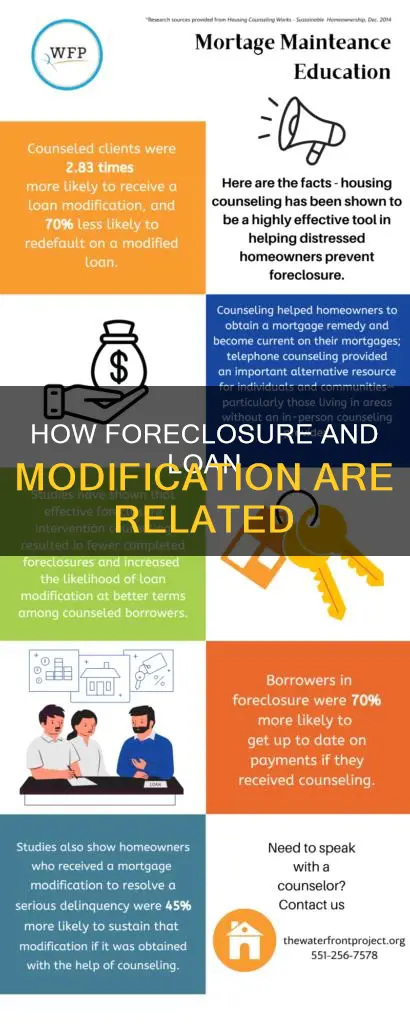

Housing Counselling Services

Housing counsellors, such as those provided by 995Hope, can assist you in exploring your options and developing a financial health profile. They can also help you communicate with your mortgage servicer to resolve your situation and may offer long-term and immediate assistance plans. HUD also recommends contacting a housing counsellor approved by their department for guidance on loan modification and other alternatives.

Deed-in-Lieu of Foreclosure

If all other options have been exhausted, you may consider a deed-in-lieu of foreclosure. This involves voluntarily transferring the property title to your mortgage company in exchange for cancelling your mortgage debt. While this option allows you to avoid foreclosure, it also means giving up ownership of your home. Your loan servicer may offer incentives to help you transition to more affordable housing.

Remember, it is important to be proactive and seek assistance as early as possible. Reach out to your lender, loan servicer, or a qualified legal professional to discuss your specific circumstances and determine the best course of action to avoid foreclosure.

How Forbearance Impacts Your Loan: What You Need to Know

You may want to see also

![]()

Application timing

The timing of your application for a loan modification is crucial if you want to stop foreclosure. Federal law prohibits mortgage lenders from conducting a foreclosure while a mortgage modification application is under consideration. However, there are specific timelines that must be adhered to.

Firstly, you must submit your application to the lender at least 45 days before the scheduled foreclosure sale of your home. If you miss this deadline, there is still protection under what is known as Regulation X. According to this regulation, if a loan modification application is made more than 37 days before the foreclosure sale, the lender cannot conduct the sale until they have issued a decision on the application. Furthermore, no foreclosure can be instituted until 120 days have passed from the first delinquency. If a complete loan modification application is submitted within this 120-day period, no foreclosure can be initiated.

It is important to note that the process of obtaining a loan modification can be complicated, and it varies for each lender. Some lenders require a "borrower response package" or a "loss mitigation application", while others automatically evaluate you for a mortgage modification if you are behind by a certain number of payments. It is recommended that you consult a loan modification lawyer or a foreclosure defense attorney to help you determine the best options for your circumstances and guide you through the application process. They can also assist in negotiating with your mortgage company to ensure you get the best possible loan modification terms.

![]()

Eligibility criteria

- The home on your mortgage is your primary residence.

- You have enough income to afford payments under the modified terms of the loan.

- You are facing a financial hardship but will be able to keep up with reduced payments.

Some common types of loan modification options offered by banks include:

- Interest rate reduction: Depending on the conditions of the loan modification, an interest rate reduction can be temporary or permanent. Lowering the interest rate can help reduce the monthly payment amount.

- Term extension: Extending the loan term can spread the remaining balance over a more extended period, making monthly payments more manageable.

- Principal forbearance: The lender agrees to put the loan's principal balance in forbearance for a specified period, reducing the payment amount. However, the forbearance amount must be repaid eventually.

It is important to note that not all borrowers will be eligible for a loan modification. It is recommended to consult with an experienced mortgage law and foreclosure defense attorney to explore all available options and determine the best course of action.

![]()

Legal protection

If you are facing foreclosure on your home, it is important to seek legal advice from a foreclosure defence attorney. They can help you understand your options and protect your rights. The loan modification process can be complicated, and a lawyer can help ensure your application is correct and that you do not leave out any necessary documentation.

Federal laws regulate loan services and foreclosure procedures. Specifically, 12 C.F.R. § 1024.41 states that a servicer cannot initiate foreclosure unless the borrower is over 120 days past due on their mortgage payments. Before the foreclosure, your bank or lender must send you a breach letter, informing you that your loan has gone into default and providing information on how to resolve the issue, including options for modifying your mortgage.

In response to issues during the mortgage crisis in the early 2010s, the federal government implemented mortgage servicing regulations that provide additional protections for homeowners. Certain states, including California, Colorado, Nevada, and Minnesota, passed parallel laws to complement the federal laws. These rules give mortgage servicers more incentives to work out alternatives to foreclosure with homeowners and have adjusted the process of loan modification to reduce the risk of errors. An important consequence of the new rules is that a homeowner can work with a single representative of the mortgage servicer throughout the process, a concept known as continuity of contact.

If you are considering a loan modification, you must submit your application to the lender at least 45 days before the scheduled foreclosure sale of your home. The lender must approve the new terms of the contract, and you cannot miss additional payments. You may be eligible for a lower interest rate if you have enough equity in your home, or you could reduce the remaining principal on your mortgage. You can also switch from adjustable to fixed rates.

![]()

Pros and cons

Pros

Foreclosed homes are usually sold at a lower price.

Cons

- The process of foreclosure is lengthy and unpredictable.

- It is risky and requires flexibility and patience.

- You may not be able to conduct a home inspection before the sale.

- You may have to cover more costs, such as closing costs, and there may be potential title issues.

Pros

- Loan modifications can help you prevent foreclosure and stay in your home.

- They can reduce your monthly payments and affect your credit rating less than a foreclosure.

- Loan modifications can benefit both the lender and the borrower by enabling the borrower to afford the payments and the lender to recover at least some of the money loaned.

- Loan modifications can give you more time to pay off your loan and may allow you to settle any payment delinquencies.

- You may be able to reduce your interest rate, principal amount, or switch from an adjustable to a fixed-rate loan.

Cons

- Loan modifications can be complicated to handle alone, and you may need to seek legal assistance.

- You may end up paying more over time to repay the loan, including extra fees or tax liabilities.

- Your credit score may be impacted if your lender reports the modification as a debt settlement.

- The lender may deny your request for a loan modification, so it should not be your only option.

Frequently asked questions

Yes, but only if a complete loan modification application has been submitted to the servicer by the 120-day point from the first delinquency. If the borrower misses this deadline, a loan modification application made more than 37 days before the foreclosure sale will still protect you from foreclosure until a decision is made on the application.

A loan modification is a change in the terms of your mortgage through an agreement with your lender. It is a common type of loss mitigation that can help you avoid foreclosure.

You can apply for a loan modification by reaching out to your lender and explaining your situation. You will need to submit a completed loss mitigation application and provide supporting documentation such as income statements, monthly expenses, and a hardship letter.

A loan modification can help you prevent foreclosure and stay in your home. It can also reduce your monthly payments, lower your interest rate, and integrate missed payments into the remaining balance.

A loan modification may result in you paying more over time to repay the loan. It can also impact your credit score and incur extra fees or tax liability.