Loans are a common way to fund higher education, but they can also be confusing. Student loans are a form of financial aid that must be repaid, usually with interest. Understanding the details of repayment can save you time and money, and it's important to know your responsibilities as a borrower. While student loans can be a helpful tool, they are not the only option for funding your education. Scholarships, grants, and work-study programs can also provide valuable financial assistance and do not need to be repaid. It's also important to consider your ability to repay your loan, as broader economic conditions or personal financial challenges can impact your ability to keep up with payments.

| Characteristics | Values |

|---|---|

| Nature of a loan | A loan is a form of debt incurred by an individual or other entity. |

| Lender | Usually a corporation, financial institution, or government. |

| Borrower | An individual or other entity. |

| Repayment | The borrower agrees to repay the loan value amount with interest. |

| Interest | Charged based on an agreed-upon rate and payment schedule from when a loan is disbursed to when it's settled. |

| Collateral | May be required by the lender to secure the loan and ensure repayment. |

| Loan agreement | Outlines the expectations for repaying the debt, including the contracted interest rate. |

| Consequences of non-repayment | Involuntary bankruptcy, late payment charges, and a damaging blow to the credit rating. |

| Types of loans | Student loans, mortgages, revolving loans, term loans, bonds, and certificates of deposit (CDs). |

| Student loan repayment options | Graduated payment plans, deferment options, and loan forgiveness. |

| Mortgage repayment options | Refinancing, reinstatement, forbearance, and loan modifications. |

What You'll Learn

![]()

Student loans

Federal student loans are a common funding option, and they offer benefits that private loans may not. For instance, federal loans provide access to temporary loan payment relief through approved periods (deferment or forbearance) due to financial hardship, continuing education, or military service. Additionally, subsidized federal loans do not accumulate interest during periods when payments are deferred. It is important to note that refinancing a federal loan into a private loan may result in losing these benefits, so careful consideration is necessary before making any changes to the loan type.

The repayment process for student loans typically begins after graduation, dropping below half-time enrolment, or leaving school. Most federal student loans offer a grace period before regular payments are required. Direct Subsidized Loans, Direct Unsubsidized Loans, and Federal Family Education Loans have a six-month grace period, while Perkins Loans offer a nine-month grace period. PLUS loans, on the other hand, generally do not have a grace period, and repayment begins as soon as the loan is fully disbursed. However, graduate and professional student PLUS borrowers receive an automatic six-month deferment after graduation or leaving school.

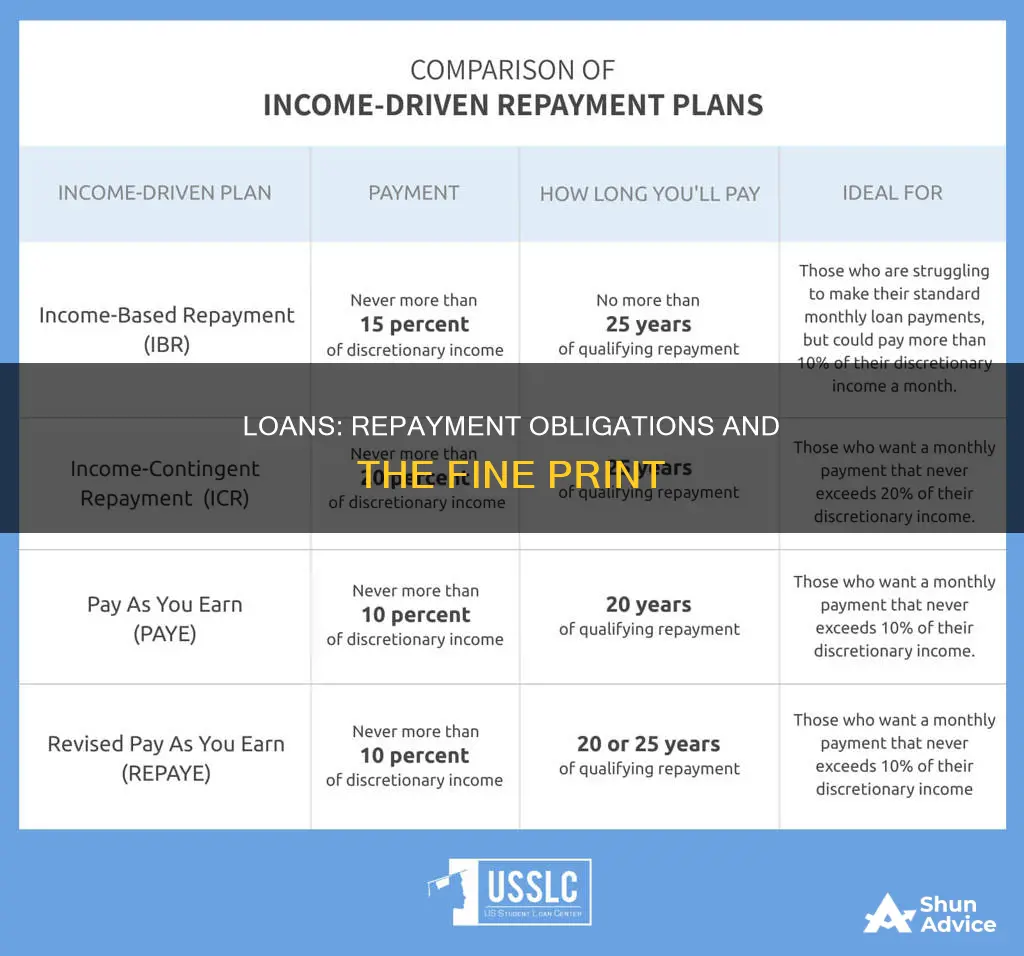

To manage student loan repayment effectively, it is advisable to stay in touch with the loan servicer, especially if there are difficulties in making payments. Servicers can provide information on repayment options, such as income-driven repayment plans, forbearance, or deferment. Additionally, consolidating multiple federal student loans into a single loan with a lower interest rate is an option to consider for better manageability.

Some students may be eligible for forgiveness of their student loan debt. The Public Service Loan Forgiveness program is a common avenue for loan forgiveness, and it applies to those working in specific fields or certain situations. It is important to have a repayment plan in place before the payments begin to ensure timely repayment and manage costs effectively.

LoanMe: Understanding the Reasons for Loan Denial

You may want to see also

![]()

Loan refinancing

Generally, loans have to be repaid, and you'll usually be charged interest on top of the amount borrowed. However, refinancing a loan can help you secure a lower interest rate, reducing the overall cost of the loan. Refinancing involves replacing an existing loan with a new one that has more favourable terms. This can include a lower interest rate, a longer duration, or a higher loan amount.

There are several types of refinancing options. The most common type is rate-and-term refinancing, where the new loan agreement comes with a lower interest rate. Cash-outs are another option, where individuals can withdraw the increased value or equity in an underlying asset that collateralises the loan. This provides immediate access to cash while maintaining ownership of the asset. However, this option often results in a higher loan amount and interest rate.

When refinancing a loan, borrowers can approach their existing lender or a new one to complete a new loan application. The lender will then re-evaluate the borrower's income, credit history, and financial situation. Common motivations for refinancing include taking advantage of lower interest rates, improving credit scores, or consolidating existing debts into a single, more manageable loan.

Several institutions offer refinancing services for personal loans. For instance, BHG Financial allows refinancing of up to $200,000 with a credit score of at least 660, while Upstart caters to individuals with lower credit scores, including students with no credit history. PenFed offers small personal loans with low rates, although membership is required to borrow from federal credit unions. Best Egg is another option, particularly for debt consolidation, as it provides an online dashboard to track funds across multiple accounts.

Loandepot's Loan Sales: What You Need to Know

You may want to see also

![]()

Loan forgiveness

Generally, any loan taken out will need to be repaid, often with interest. However, there are some exceptions to this rule, and certain loans can be forgiven. Loan forgiveness is when you are no longer legally required to make payments on your loan. This can occur in several ways, and there are various programs and eligibility criteria to consider.

One example is student loan forgiveness. Federal student loans are the primary form of financial aid that must be repaid, usually with interest. However, if you are eligible for student loan forgiveness, you may no longer be required to make these payments. It is important to note that FAFSA (Free Application for Federal Student Aid) itself does not provide direct financial aid in the form of grants or loans, but it is the application you fill out to be considered for financial aid. The type of financial aid received through FAFSA that does not need to be repaid includes grants, scholarships, and work-study programs.

There are different types of student loans, and their eligibility for forgiveness varies. Direct subsidized loans, for example, are awarded based on financial need, and the federal government pays the interest while the student is in school and during any grace period. On the other hand, interest on direct unsubsidized loans begins to accrue immediately, and the federal government does not cover the interest. While these loans are not inherently eligible for forgiveness, there are still ways to have them forgiven under specific programs.

To be eligible for student loan forgiveness, there are usually specific requirements and conditions that must be met. These can include factors such as the borrower's income, the type of repayment plan, and the nature of the borrower's job or volunteer work. For instance, those working in public service, education, or non-profit organizations may be eligible for loan forgiveness after a certain period of consistent payments. Additionally, there are loan forgiveness programs tailored to specific professions, such as teachers, nurses, or lawyers working in public interest fields.

It is important to note that loan forgiveness programs can change over time, and new programs may be introduced or existing ones modified. Therefore, it is advisable to stay informed about the latest updates and consult official sources or seek professional advice to understand the specific requirements and eligibility criteria for loan forgiveness.

Collateral Appraisal: Does Loan-to-Value Matter?

You may want to see also

![]()

Loan repayment terms

There are two common types of loan repayment schedules: even principal payments and even total payments. With even principal payments, the borrower makes the same principal payment for every instalment, and the interest decreases with each payment as the unpaid balance reduces. This results in a lower total payment over time. On the other hand, with even total payments, the size of the unpaid balance declines slowly during the early term of the loan and more rapidly towards the end. This leads to a higher total interest cost compared to even principal payments.

Some loans include a balloon payment structure, where the borrower makes smaller annual payments initially and then pays off the remaining balance in a lump sum later in the repayment period. This option may be suitable for businesses with limited repayment capacity in the early years, allowing them to repay or refinance the loan after several years.

When considering loan repayment terms, it is essential to review the loan agreement closely. Factors such as interest rates, fees, and prepayment penalties can significantly impact the total cost of the loan. Prepayment penalties, for instance, are designed to protect lenders from losing interest income if borrowers pay off their loans early. By understanding these terms and comparing different lenders, borrowers can make informed choices and minimise additional costs.

Loan Star Title Loans: Buyout Options and Opportunities

You may want to see also

![]()

Collateral and defaulting

Collateral is an asset that a lender accepts as security for extending a loan. In other words, it is an item of value pledged to secure a loan. Collateral minimises the risk for lenders by ensuring that the borrower keeps up with their financial obligations. The borrower has a compelling reason to repay the loan on time because if they default, they stand to lose their collateral. Mortgages and car loans are two types of collateralised loans. Other personal assets, such as a savings or investment account, can also be used to secure a collateralised personal loan.

Defaulting on a loan means that you have stopped making payments and have failed to follow through on the terms of your loan agreement. If you default on a secured loan, the lender may seize the collateral and sell it, applying the money it gets to the unpaid portion of the loan. For example, if you default on a mortgage loan, your lender may repossess your home through foreclosure. Similarly, if you default on an auto loan, your lender may repossess your vehicle. If there is a remaining balance on the loan after the collateral is sold, the lender can choose to pursue legal action against the borrower to recoup the remaining balance. This may include wage garnishment, bank account levies, or property liens.

It is important to note that defaulting on a loan can have severe consequences beyond the loss of collateral. It can negatively impact your credit score, making it more difficult to obtain new credit or loans in the future. It can also affect your job prospects, housing options, and insurance premiums. Therefore, it is essential to carefully consider your ability to repay a loan before taking one out and to proactively communicate with your lender if you are experiencing financial difficulties.

Loans and Currency: What's the Connection?

You may want to see also

Frequently asked questions

Yes, any loan taken out will have to be repaid, usually with interest.

Common types of loans include student loans, mortgages, credit cards, and bonds.

Some alternatives to taking out a loan are grants, scholarships, and work-study programs.