Financial leverage is a strategic endeavour that involves borrowing money to invest in assets. The goal is to generate a return on those assets that exceeds the cost of borrowing the funds. Financial leverage can be a powerful tool for investors and businesses, providing opportunities for growth and increased returns. However, it also comes with risks, as it amplifies losses in downturns and increases debt obligations. In real estate, positive leverage occurs when the equity yield or cash-on-cash return on a property investment is greater than the cost of debt. This implies that the rental income generated is sufficient to offset the borrowing costs. Positive leverage can also be calculated using the formula: Positive Leverage = Equity Yield (%) - Loan Constant (%). If the output is positive, there is positive leverage, indicating a profitable investment.

| Characteristics | Values |

|---|---|

| Definition of positive leverage | When the equity yield earned on a property investment is greater than the cost of debt |

| Example of positive leverage | If the equity cap rate is 6.25% while the loan constant is 6.0%, there is positive leverage |

| Definition of financial leverage | Borrowing money to invest in assets |

| Risks of financial leverage | High debt-to-equity ratio, volatile earnings, increased chance of default or bankruptcy, credit downgrades |

| Benefits of financial leverage | Enhanced earnings, access to expensive investment options, fuel for growth |

| Leveraged loans | Issued to companies or individuals with a considerable amount of debt or a low credit rating |

| Leveraged loan interest rates | Higher than average |

| Leveraged loan administration | Arranged by financial institutions and then sold to investors |

What You'll Learn

![]()

Positive leverage in real estate

The funding structure of most purchases in the real estate market, on both the residential and commercial sides, is financed using debt or borrowed capital from lenders. The debt capital provided by the lender usually comes at a price in the form of periodic interest payments and principal amortization.

Positive leverage can be calculated using the formula: Positive Leverage = Equity Yield (%) − Loan Constant (%). If the output is a positive figure, there is positive leverage.

Positive leverage is the target outcome on a property investment since the operating cap rate is higher than the interest rate or cost of borrowing. It is important to note that the concept of analyzing positive and negative leverage is only applicable for fixed-rate loans.

While financial leverage may result in enhanced earnings, it may also result in disproportionate losses. It is important to carefully consider the advantages and disadvantages of financial leverage and determine whether it aligns with one's financial circumstances and goals.

Loan Counseling: Does It Really Make a Difference?

You may want to see also

![]()

The impact of leverage on investment cash flow

In real estate, positive leverage occurs when the equity yield earned on a property investment is greater than the cost of debt. This means that the rental income generated by the property is sufficient to offset the borrowing costs. The cash-on-cash return, or equity yield, can be perceived as the "equity cap rate", while the loan constant can be seen as the "lender cap rate". If the annual cash yield increases year-over-year, the return on equity rises as the "spread" between the cash flow generated by the property and the cost of servicing the debt becomes greater.

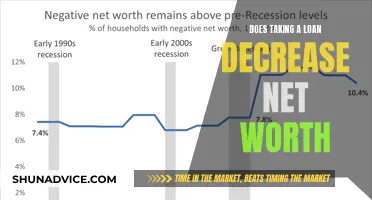

On the other hand, negative leverage occurs when the cash-on-cash return on a levered basis is less than the cost of debt, causing a decline in the return on the equity investment. The lower the "spread" between the cap rate and interest rate, the closer to negative leverage the investment becomes.

Leverage can also impact a company's financial health and its return on equity. The leverage effect occurs when a company increases its return on equity by taking on debt (borrowed capital) as long as the return on the capital employed is higher than the cost of the borrowed capital. The greater the difference between the return on invested capital and the cost of debt capital, the greater the positive effect on the return on equity.

Leverage ratios are used to measure financial leverage and assess a company's financial strength. The most common leverage ratio is the debt-to-equity ratio, which shows the proportion of debt to a company's equity and helps stakeholders understand the level of risk in the company's capital structure. Other common leverage ratios include the equity multiplier, debt-to-capitalization ratio, degree of financial leverage, and consumer leverage ratio.

In summary, the impact of leverage on investment cash flow can be positive when the returns on the investment exceed the cost of borrowing, leading to increased cash flow and higher returns for investors. However, it can also be negative if the investment does not generate sufficient returns to cover the borrowing costs, resulting in decreased cash flow and potential losses for investors.

FAFSA: Determining Loan Eligibility and Your Financial Future

You may want to see also

![]()

The risks of financial leverage

Financial leverage is a strategic endeavour that involves borrowing money to invest in assets. The goal is to have the return on those assets exceed the cost of borrowing the funds. While financial leverage can create opportunities for investors and businesses, it also comes with several risks.

Firstly, financial leverage amplifies losses in downturns. If the investment does not perform as expected, the use of leverage can result in much higher downside risk, sometimes leading to losses greater than the initial capital investment. This is because leverage increases the potential downside risk along with the potential returns from a project.

Secondly, financial leverage can lead to a high debt-to-equity ratio, indicating that a company has more debt than equity. A high debt-to-equity ratio can increase the risk of default or bankruptcy, especially if the company's variable costs are higher than its fixed costs. It can also make it difficult for consumers to secure loans, as lenders often set debt-to-income limitations when evaluating loan applications.

Thirdly, financial leverage can be complex and require additional attention to one's portfolio. Investors must be aware of their financial position and the risks they inherit when using leverage. They may need to contribute additional capital if their trading account does not have sufficient funding to meet their broker's requirements.

Lastly, financial leverage can result in large swings in company profits, causing the stock price to rise and fall more frequently. This volatility can hinder the proper accounting of stock options owned by the company's employees.

In summary, while financial leverage can provide access to capital and enhance earnings, it also carries significant risks, including amplified losses, increased debt-to-equity ratios, complexity, and volatility in company profits. It is important for investors and businesses to carefully consider these risks before taking on financial leverage.

IRS Student Loan Returns: What You Need to Know

You may want to see also

![]()

The types of leveraged loans

Leveraged loans are loans made by banks or other financial institutions that are then sold to investors. They are also known as floating-rate loans or bank loans. Companies that take out these loans typically have high levels of debt or poor credit ratings.

There are several types of leveraged loans:

- Speculative-grade loans: These are also known as leveraged loans and are issued to speculative-grade companies. They are often used to raise debt capital for leveraged buyouts (LBOs), mergers and acquisitions (M&A), debt refinancing, and recapitalizations.

- Term loans: These are issued privately by banks and institutional investors. They are typically used for debt refinancing or to fund large projects or expansions.

- Revolvers: Similar to term loans, revolvers are issued privately by banks and institutional investors. They differ in that they are typically used for working capital or general corporate purposes, rather than for specific projects or investments.

- Covenant-lite loans: These are a more recent type of leveraged loan that has looser lending standards and fewer maintenance covenants than traditional leveraged loans. They are still usually secured with first liens but have more flexible credit ratios, making them a popular option for borrowers.

- Leveraged buyouts (LBOs): This is a specific type of leveraged loan where a company or private equity firm uses debt to purchase a public entity and take it private. LBOs often involve a significant amount of debt and fall under the leveraged finance umbrella.

- Mergers and Acquisitions (M&A): Acquirers often take out leveraged loans to finance acquisitions, especially when a large amount of debt is needed.

- Recapitalizations: Companies may use leveraged loans to borrow money to pay dividends or buy back shares.

Government Control Over College Loans: Examining the Facts

You may want to see also

![]()

How to calculate financial leverage

Financial leverage is the strategic borrowing of money to invest in assets. The goal is to have the return on those assets exceed the cost of borrowing the funds. Financial leverage can be beneficial for investors and businesses as it creates opportunities for them. However, it also comes with high risk as it amplifies losses in downturns.

There are several ratios that can be used to calculate financial leverage. Here are some of the most common ones:

Debt-to-Equity Ratio

The debt-to-equity ratio is the most commonly used leverage ratio. It is calculated by dividing a company's total debt by its shareholders' equity. The debt-to-equity ratio helps stakeholders understand the level of risk in the company's capital structure and the likelihood of the company facing difficulties in meeting its debt obligations.

Degree of Financial Leverage (DFL)

The degree of financial leverage is a ratio that measures the sensitivity of a company's net income to fluctuations in its capital structure. It is calculated by dividing the percent change in a company's net income by the percent change in its earnings before interest and taxes (EBIT). The DFL helps businesses understand their financial health and how much debt they can safely assume.

Equity Yield Minus Loan Constant

In real estate, positive financial leverage exists when the equity yield earned on a property investment is greater than the cost of debt. The equity yield is the annual cash yield earned on an investment property. The loan constant, also known as the mortgage constant, is the annual debt service (interest plus principal amortization) expressed as a percentage of the original principal on a fixed-rate loan. Positive leverage exists when the equity yield is greater than the loan constant.

Other Leverage Ratios

Other leverage ratios used to calculate financial leverage include the equity multiplier, debt-to-capitalization ratio, consumer leverage ratio, debt-to-EBITDA leverage ratio, interest coverage ratio, and fixed-charge coverage ratio. These ratios assess a company's ability to meet its financial obligations and evaluate its mix of operating expenses and debt.

When calculating financial leverage, it is important to consider the industry, the age of the company, and other factors. Comparing financial ratios with competitors or similar companies can provide valuable insights into the financial health and risk level of a business.

Loans and Unemployment: Impact and Influence Explored

You may want to see also

Frequently asked questions

Positive financial leverage occurs when the return on equity is increased by borrowing. In other words, when the return on an asset exceeds the loan interest rate, borrowing results in a higher return on equity.

In real estate, positive financial leverage occurs when the equity yield earned on a property investment is greater than the cost of debt. For example, if the rental income generated by a property can sufficiently offset the borrowing costs, there is positive leverage.

Positive financial leverage can be calculated using the following formula: Positive Leverage = Equity Yield (%) - Loan Constant (%). If the output is a positive figure, there is positive leverage.

Financial leverage can be risky because it amplifies losses in downturns and creates more debt that can be challenging to pay off if business slows down in subsequent years. Additionally, uncontrolled debt levels can lead to credit downgrades or bankruptcy. It's important to carefully consider the risks and compare them to the advantages before using financial leverage.