If you're earning a $100,000 salary, you're in a good position to buy a home. However, it's essential to determine how much mortgage you can afford based on your income and other factors. Lenders will evaluate your overall debt-to-income ratio, credit score, and history to ensure you can take on a mortgage. To get an accurate estimate, you can use a mortgage affordability calculator, which considers factors like desired mortgage amount, interest rates, loan term, and more. The 28/36 rule is also a common guideline, suggesting that no more than 28% of your gross monthly income should be spent on housing expenses, and no more than 36% on total debt.

| Characteristics | Values |

|---|---|

| Salary | $100,000 per year |

| Average monthly income | $8,333 |

| Maximum monthly mortgage payment | $2,333.33 |

| Maximum mortgage payment as a percentage of income | 28% |

| Maximum total debt payments as a percentage of income | 36% |

| Down payment | 20% |

| Interest rate | 5-6.99% |

| Closing costs | 2-5% of the purchase price |

| Debt-to-income ratio | 40-50% |

| Credit score | 720+ |

What You'll Learn

- Lenders will evaluate your overall debt-to-income ratio

- A higher credit score can make you eligible for lenders' best interest rates

- The bigger your down payment, the lower your monthly payment

- Your monthly mortgage payment should not exceed 28% of your gross monthly income

- Your interest rate will impact your monthly mortgage payment

![]()

Lenders will evaluate your overall debt-to-income ratio

Lenders use the DTI ratio to assess if you can handle the anticipated mortgage payment while keeping up with other monthly payments. They will also use it to determine if you can afford to take on additional debt. A high DTI indicates that a lot of your incoming cash is already committed, and you might struggle to repay a new loan.

A DTI of 43% is usually the highest ratio a borrower can have and still qualify for a mortgage. Lenders generally prefer a DTI of no more than 36%, with no more than 28%-35% of that debt going towards mortgage payments.

To lower your DTI, you can increase your income, pay off existing debt, or consider purchasing a less expensive home. Improving your credit score can also help you qualify for a larger mortgage, as a higher score makes you eligible for lenders' best interest rates.

Mortgage Business: A Giant Industry Overview

You may want to see also

![]()

A higher credit score can make you eligible for lenders' best interest rates

When considering taking out a mortgage, it is important to remember that your income is not the only factor that determines how much you can borrow. Your credit score, for example, can have a significant impact on the interest rates offered by lenders.

A higher credit score can make you eligible for a lender's best interest rates. Credit scores directly impact mortgage interest rates, and a difference of just 100 points could cost or save you thousands over the course of the loan. For example, a borrower with a credit score of 780 taking out a 30-year fixed-rate loan of $240,000 at 4% interest would pay around $1,164 per month. If that score dropped by 100 points, the interest rate might increase to 4.5%, increasing the monthly payment to $1,216, an extra $62 per month or $744 per year. Over the course of the 30-year loan, the borrower with the higher credit score would pay $25,300 less in interest.

Lenders use "risk-based pricing" to determine the interest rates and fees they offer, factoring in your credit score as an estimate of the risk that you will fail to pay back the loan. Each lender will have its own standards for what constitutes an acceptable score, but generally, a score of 740 or higher is considered excellent credit, while a score of 629 or below is considered poor credit.

In addition to your credit score, lenders will also consider other factors such as your employment status, income, and any outstanding debts. It is important to remember that even a small difference in interest rates can have a big impact over time, so it is worth comparing options from multiple lenders to find the best deal.

To get a clearer picture of what you can afford, you can use a mortgage affordability calculator. This will take into account your income, credit score, and other financial factors to estimate how much you could borrow and what your monthly payments might be.

Impac Mortgage's Size and Scope: A Comprehensive Overview

You may want to see also

![]()

The bigger your down payment, the lower your monthly payment

When considering taking out a mortgage, it is important to keep in mind that the bigger your down payment, the lower your monthly payment. This is because a larger down payment reduces the loan-to-value (LTV) ratio, which compares the amount of your mortgage to the property's appraised value. By lowering the LTV, you increase the equity in your home and potentially secure a lower interest rate.

The size of your down payment directly impacts your mortgage interest rate. Lenders consider a larger down payment to be a sign of a motivated buyer and a lower financial risk, which may result in a reduced interest rate. Conversely, a smaller down payment may lead to a higher interest rate. By securing a lower interest rate through a larger down payment, you can save money over the life of the loan by paying less interest.

Additionally, a larger down payment can help you qualify for a better loan type. Certain loans, such as conventional loans, typically require a minimum down payment of 5%, while some lenders may accept a lower down payment of 3%. However, making a 20% down payment can help you avoid paying private mortgage insurance (PMI), which is an additional monthly fee added to your mortgage payment.

It is worth noting that while a larger down payment can provide significant benefits, it is not the only factor considered by lenders. Your credit score, debt-to-income ratio, and other financial considerations also play a role in determining your mortgage eligibility and interest rate. Therefore, it is important to assess your financial situation comprehensively before deciding on the size of your down payment.

To estimate your monthly mortgage payments, you can utilise a mortgage affordability calculator, which takes into account various factors, including income, credit score, and debt obligations, to provide you with a more accurate understanding of your potential payments.

Guild Mortgage: A Giant in the Industry

You may want to see also

![]()

Your monthly mortgage payment should not exceed 28% of your gross monthly income

When considering taking on a mortgage, it is important to keep in mind that your monthly payments should not exceed 28% of your gross monthly income. This is a general rule of thumb, known as the 28% rule, which helps borrowers avoid overextending their finances and acts as a safeguard to ensure they have enough money in their budget for emergencies and other expenses.

For example, if your gross monthly income is $5,000, you shouldn’t spend more than $1,400 on your monthly mortgage payment ($5,000 x 0.28 = $1,400). This rule is a popular guideline for homeowners as it allows them to balance buying the home they desire while also keeping a healthy budget.

It is also important to note that your income is not the only factor that determines how much of a mortgage you can take on. Lenders will also consider your credit score, debt-to-income ratio, and other financial considerations. For example, if you have a large monthly car payment, you may want to consider swapping it for something less expensive to free up your budget.

Additionally, the interest rate and down payment will impact your monthly mortgage payment. A larger down payment will result in a lower monthly mortgage payment, and securing a lower interest rate can also lower your payments. It is recommended to compare multiple lenders and loan options to find the best deal.

In summary, while the 28% rule is a helpful guideline, it is important to consider all factors when determining how much of a mortgage you can afford. By keeping your monthly mortgage payment below 28% of your gross monthly income and considering other financial factors, you can ensure you are not overextending your finances and setting yourself up for success in the home-buying process.

Mr Cooper's Mortgage: How Big Is It Really?

You may want to see also

![]()

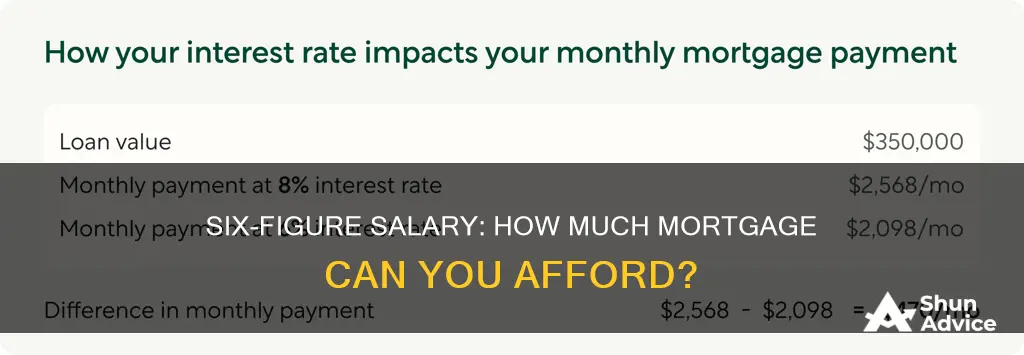

Your interest rate will impact your monthly mortgage payment

When considering a mortgage, it's important to remember that interest rates play a significant role in determining your monthly payments. A higher interest rate leads to higher monthly mortgage payments, while a lower interest rate allows you to borrow more. Even a small difference in interest rates can significantly impact your finances over time. For example, a $100,000 mortgage with a 6% interest rate results in a monthly payment of $599.55, while the same loan with a 9% interest rate increases the monthly payment to $804.62.

To secure a lower interest rate, you can improve your credit score and pay off credit card balances and other debts, which will enhance your debt-to-income ratio. A higher credit score makes you eligible for lenders' best interest rates. Additionally, consider making a down payment of at least 20% to avoid paying private mortgage insurance, which increases your monthly payments.

Market fluctuations can cause interest rates to rise or fall, affecting your purchasing power. Rising interest rates increase the cost of borrowing money for a house, while decreasing demand. Strong economic growth tends to raise mortgage rates, whereas weak economic cycles can lower them. Inflation is a key factor that influences economic growth and interest rates.

The type of mortgage you choose also determines how interest rates will impact your monthly payments. Fixed-rate mortgages lock in a set interest rate, while adjustable-rate mortgages can have changing interest rates after an initial period. When calculating your monthly payments, consider the principal and interest payments, as well as property taxes and insurance.

Lastly, the term of your mortgage loan, whether 15 or 30 years, will also influence your monthly payments. Generally, a longer-term loan results in lower monthly payments, making 30-year mortgages more popular.

United Wholesale Mortgage: A Giant in the Industry

You may want to see also

Frequently asked questions

This depends on several factors, including your credit score, debt-to-income ratio, down payment, and interest rate. A common guideline is that your mortgage payment should not exceed 28% of your gross monthly income, which would be $2,333 for a $100,000 salary. You can use a mortgage affordability calculator to get a more accurate estimate.

The debt-to-income ratio (DTI) is a percentage that represents the portion of your gross monthly income that goes towards repaying debts, such as mortgage payments, credit card balances, and other loans. Lenders use this ratio to assess your ability to comfortably make monthly mortgage payments, with a preferred front-end DTI ratio of no more than 28%.

A higher credit score can make you eligible for lenders' best interest rates and may also impact the required down payment. Lenders view a good credit history as a demonstration of financial responsibility, which is crucial when seeking a mortgage.

In addition to the mortgage itself, you need to consider property taxes, homeowners insurance, and maintenance costs. Closing costs and lender credits can also add to your upfront expenses when purchasing a property.