The mortgage business has undergone significant changes since the 2008 financial crisis. In the years leading up to the crisis, loose lending standards and a lack of regulation on subprime mortgage lenders contributed to a housing bubble that eventually burst, leading to the Great Recession. The aftermath of the crisis saw a shift towards tighter lending standards and increased government oversight of the mortgage market. Mortgage rates have fluctuated over the years, with record highs in the early 1980s and a steady decline post-2008, reaching historic lows during the COVID-19 pandemic. The pandemic has also impacted the housing market and the mortgage industry, with soaring home prices and climbing mortgage rates affecting affordability for many homebuyers.

| Characteristics | Values |

|---|---|

| Mortgage rates in 2008 | 6.03% |

| Mortgage rates in 2012 | 3.31% |

| Mortgage rates in 2016 | 3.65% |

| Mortgage rates in 2019 | 4.1% |

| Mortgage rates in 2020-2021 | 3% |

| Mortgage rates in 2022 | 7.08% |

| Mortgage rates in 2024 | Fluctuating |

| Mortgage rates in 2025 | Expected to dip |

| Mortgage business in 2008 | Wild West, loose standards, selling variable-rate mortgages to risky borrowers |

| Post-2008 | Rates declined steadily |

| Post-2008 crisis | Bottleneck due to first-time home buyers staying in their homes for 15+ years |

| Post-2008 crisis | Greater government oversight |

| Post-2008 crisis | More equitable lending |

What You'll Learn

![]()

The 2008 financial crisis

In the years leading up to 2008, the US housing market had been experiencing a boom. This was partly due to the increased availability of mortgages to unqualified borrowers, which caused a housing bubble that peaked in 2006. However, in 2007, housing prices began to decline, and many borrowers were forced to default on their mortgages. This housing crisis is considered the primary cause of the Great Recession, which officially began in December 2007.

The run-up in home prices was unprecedented, and subsequently, home prices fell sharply, declining by over a fifth on average across the US between the first quarter of 2007 and the second quarter of 2011. This decline in home prices further exacerbated the financial crisis as financial market participants faced significant uncertainty regarding losses on mortgage-related assets.

Additionally, lending practices contributed to the crisis. In the early 2000s, credit scores and debt-to-income ratios were not strictly adhered to, and many risky borrowers were sold variable-rate mortgages without a proper understanding of the terms. The rise of mortgage farms targeting these borrowers contributed to a volatile situation.

As the crisis intensified in 2008, the Federal Open Market Committee (FOMC) accelerated interest rate cuts, taking the rate to a target range of 0 to 25 basis points by the end of the year. The Federal Reserve also initiated large-scale asset purchase programs, buying mortgage-backed securities to support the economy and ease credit conditions.

The impact of the 2008 financial crisis was significant, and even a decade later, in 2018, mortgage rates were still lower than they had been before the crisis. The crisis also highlighted the need for fairer lending practices and greater transparency in the mortgage process.

Blend's Mortgage Revolution: Streamlining the Home Loan Process

You may want to see also

![]()

Changes in lending standards

The mortgage business has undergone significant changes since 2008, particularly in terms of lending standards. In the years leading up to the 2008 financial crisis, lending standards were quite lax, with credit scores and debt-to-income ratios being treated more as "friendly suggestions" than hard-and-fast rules. This, combined with the proliferation of mortgage farms selling variable-rate mortgages to high-risk borrowers, set the stage for a financial crisis.

In the aftermath of the 2008 crisis, also known as the Great Recession, lending standards tightened significantly. Credit scores and debt-to-income ratios became crucial factors in evaluating a borrower's fitness. Lenders became more cautious, and the availability of financing decreased. This shift in lending standards contributed to a decline in homeownership rates, despite efforts by the Federal Reserve to improve liquidity and support financial institutions.

The Federal Reserve's response to the Great Recession included cutting interest rates to near zero by the end of 2008 and initiating large-scale asset purchase programs to support the mortgage market and improve financial conditions. These actions helped put downward pressure on long-term interest rates, providing some relief to borrowers.

In recent years, however, the mortgage landscape has been challenging. Surging inflation in 2022 pushed mortgage interest rates to their highest levels in two decades. While the Federal Reserve implemented rate cuts in 2024, the market continues to experience volatility and upward pressure on rates. As of 2025, there is optimism for potential rate reductions, but the market remains uncertain.

While lending standards have become more stringent overall, there is also a greater focus on fairness and equity in mortgage lending. Efforts to address historical discrimination and segregation against borrowers of colour have led to fair housing legislation, such as the Fair Housing Act and the Truth in Lending Act (TILA). These acts protect borrowers from unfair practices and increase transparency in the mortgage process.

My Mortgage Hardly Moved: What Gives?

You may want to see also

![]()

Interest rates

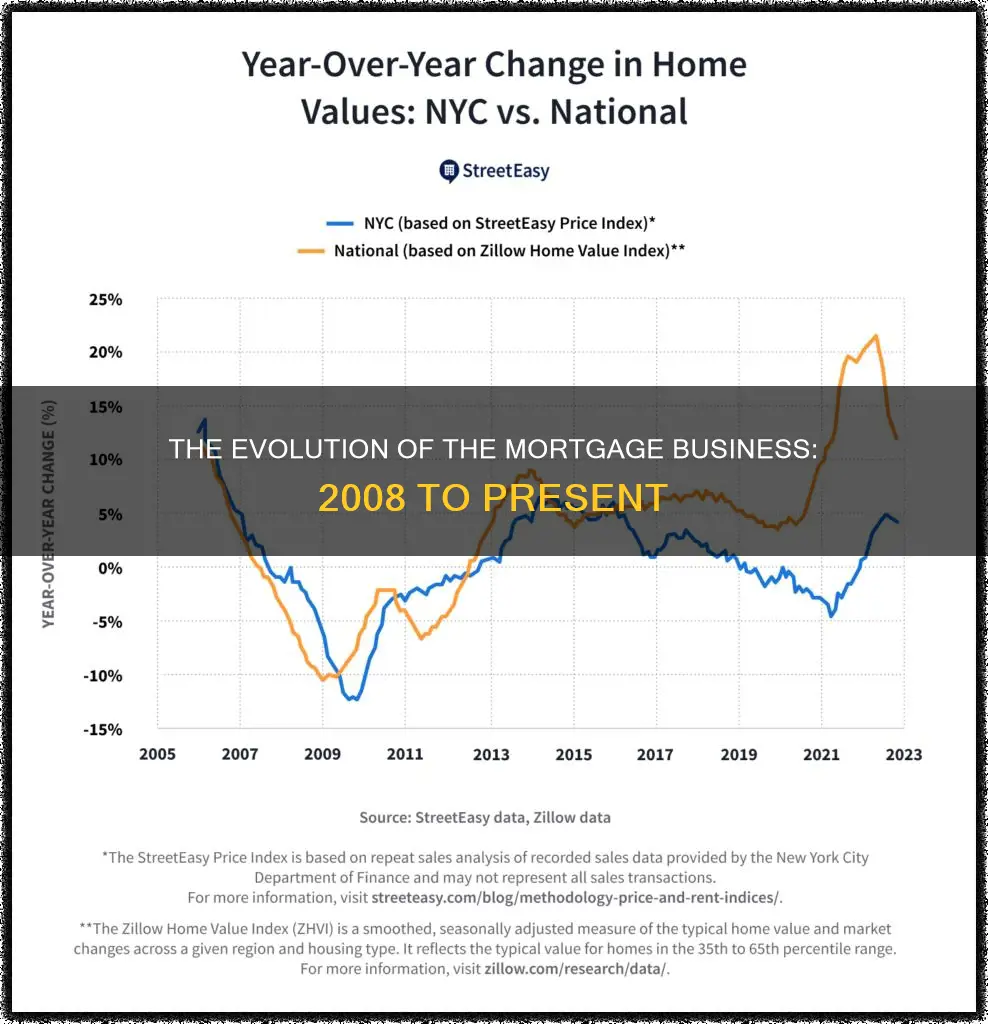

Following the 2008 financial crisis, interest rates declined steadily. In 2016, the average mortgage rate hit a record low of 3.65%. This was partly due to emergency actions by the Federal Reserve during the COVID-19 pandemic, which caused rates to drop even further, falling below 3% in 2020 and 2021.

However, this trend began to reverse in 2022, with inflation pushing mortgage interest rates to their highest levels in two decades. The average 30-year rate climbed from 3.22% in January 2022 to a peak of 7.08% in October, significantly impacting borrowing costs. The challenging landscape persisted into 2023, with economic pressures and global factors keeping rates high.

While the Federal Reserve implemented three rate cuts in 2024, bringing some relief to borrowers, the market remains volatile. As of early 2025, rates have shown fluctuation but have yet to consistently decline. There is optimism that potential rate reductions later in the year could boost buyer and homeowner interest.

Mortgage Business: A Giant Industry Overview

You may want to see also

![]()

Housing prices

The US housing market has experienced significant changes since 2008, with a mix of rising and falling housing prices and interest rates impacting affordability for homebuyers.

2008 and the Great Recession

In 2008, the US housing market was in the midst of a crisis, often referred to as the housing bubble or the subprime mortgage crisis. This was characterised by a rapid increase in house prices, which peaked in 2006, and then began to decline in 2007, with the collapse of the subprime mortgage industry. This decline in housing prices was caused by various factors, including increased foreclosure rates and a lack of regulation on subprime mortgage lenders, which led to many borrowers defaulting on their mortgages. The share prices of government-sponsored enterprises like Fannie Mae and Freddie Mac also plummeted in 2008 as investors worried about insufficient capital to cover loan losses. The crisis in the housing market was a primary cause of the Great Recession, which officially began in December 2007.

Post-2008 to 2016

Following the housing crisis, interest rates declined steadily, with 2016 holding the lowest annual mortgage rate on record since 1971, with an average of 3.65%. This was due to emergency actions by the Federal Reserve.

2022 to 2025

However, by 2022, inflation surged, causing interest rates to climb to their highest levels in two decades. In 2023, the market remained challenging, with persistent economic pressures and global factors keeping upward momentum on rates. While there were some fluctuations and temporary dips, consistent declines did not materialise.

Current State of the Housing Market

Currently, the US housing market is facing a historic shortage of homes, which has led to skyrocketing prices and an affordability crisis, further exacerbated by high mortgage rates. As of March 2025, the 30-year fixed-rate mortgage was at 6.63%, according to Freddie Mac, significantly impacting the purchasing power of aspiring homebuyers.

Future Outlook

While there is optimism for potential rate cuts in the future, experts predict that mortgage rates will continue to hover between 6% and 7% in 2025 and 2026. The supply gap in the housing market is also significant, and it will take several years to resolve, even with increased construction efforts.

What Are the Chances of Assuming a Mortgage?

You may want to see also

![]()

Regulation and legislation

The mortgage business has undergone significant regulatory and legislative changes since 2008, largely in response to the financial crisis and the subsequent Great Recession.

Prior to the 2008 crisis, mortgage lending practices were relatively lax, with credit scores and debt-to-income ratios being treated more as suggestions than hard-and-fast rules. This, combined with the proliferation of mortgage farms selling variable-rate mortgages to high-risk borrowers, set the stage for a financial disaster. In the aftermath of the crisis, it became clear that stricter regulations were needed to prevent a similar event from occurring in the future.

One of the key regulatory responses to the 2008 financial crisis was the introduction of the Term Asset-Backed Securities Loan Facility (TALF) by the Federal Reserve. The TALF was designed to ease credit conditions for households and businesses by extending credit to US holders of high-quality asset-backed securities. This helped to improve liquidity in the market and supported financial institutions and markets. Additionally, the Federal Reserve accelerated interest rate cuts, taking the rate to a target range of 0 to 25 basis points by the end of 2008.

Another important piece of legislation that has shaped the mortgage industry is the Fair Housing Act, which was passed in the late 1960s following the assassination of Dr Martin Luther King Jr. The Act prohibits discrimination against individuals looking to rent or own housing based on their race or national origin. This legislation helped to address historical injustices and inequalities in the mortgage lending process.

Furthermore, the Truth in Lending Act (TILA) brought greater transparency to the mortgage process by requiring lenders to provide borrowers with standardised disclosures detailing loan terms and costs. This empowered borrowers to make more informed decisions and better understand the financial commitments they were undertaking.

More recently, the mortgage industry has been impacted by the COVID-19 pandemic, which caused interest rates to drop to historic lows in 2020 and 2021 due to emergency actions by the Federal Reserve. However, by 2022, inflation had surged, leading to a significant increase in mortgage interest rates. As of 2025, the Federal Reserve has implemented multiple rate cuts, but the market remains challenging, with persistent economic pressures and global factors influencing interest rates.

Ford's Risky Move: Betting All Assets to Stay Afloat

You may want to see also

Frequently asked questions

The financial crisis of 2008, also known as the "Great Recession", was caused by a combination of factors, including loose lending standards, the rise of mortgage farms selling variable-rate mortgages to high-risk borrowers, and the lack of regulation on subprime mortgage lenders.

The Federal Reserve took several actions to address the Great Recession, including providing liquidity and support to financial institutions and markets through various lending programs, such as the Term Asset-Backed Securities Loan Facility (TALF), and initiating large-scale asset purchase programs to support economic activity and improve financial conditions.

The mortgage industry has become more regulated and cautious since the 2008 crisis. Credit scores and debt-to-income ratios are now given more weight in evaluating borrowers. There has also been a shift towards longer-term homeownership, with first-time homebuyers staying in their homes for longer periods, impacting business growth expectations.

During the COVID-19 pandemic, mortgage interest rates dropped to historic lows, falling below 3% in 2020 and 2021 due to emergency actions by the Federal Reserve to support the economy.

While there have been some challenges with soaring home prices and climbing mortgage rates, there is optimism for potential rate cuts in 2025, which could boost buyer and homeowner interest.