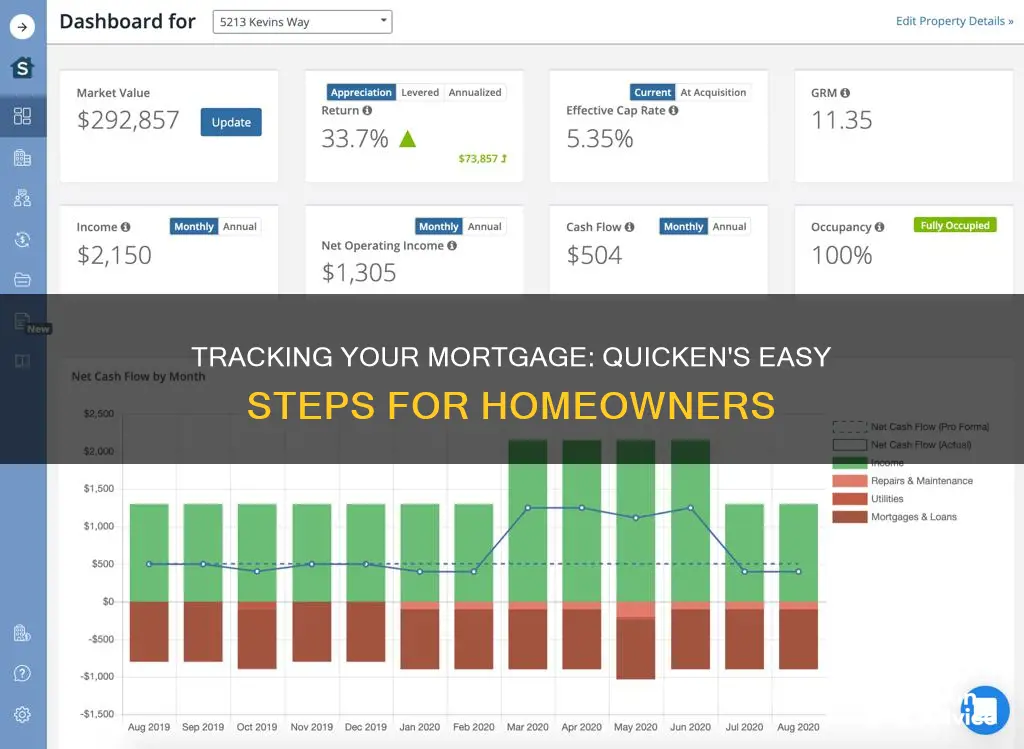

Quicken is a useful tool for tracking your mortgage payments and principal balance. It offers a convenient built-in mortgage tracker that can help you keep track of interest rates, loan amortization, and monthly mortgage payments. It also provides payment reminders and helps you categorize, budget, and track the details of your loan and its payments. Quicken allows you to track each individual line item in your mortgage, such as mortgage interest, insurance, property taxes, and any other expenses. You can also use Quicken's loan calculator to understand how much time and interest you could save by increasing your monthly payments or making a lump-sum payment. If you own a property with someone else, you can set up a joint account in Quicken to record and track both your payments. Additionally, it is recommended to create a home asset account to complement your mortgage tracking and provide a more accurate picture of your net worth.

| Characteristics | Values |

|---|---|

| Track mortgage payments | Track monthly mortgage payments automatically |

| Track principal balance | Yes |

| Track interest rates | Yes |

| Track loan amortization | Yes |

| Track individual line items in mortgage | Yes |

| Track jointly held mortgage | Yes |

| Track corresponding home value | Yes |

| Track home equity | Yes |

| Track tax basis | Yes |

| Track historical record of escrow | Yes |

| Track changes in escrow | Yes |

| Track improvements to home | Yes |

| Track monthly payment breakdown | Yes |

| Track payment reminders | Yes |

| Track budgeting | Yes |

What You'll Learn

![]()

Setting up a new mortgage account

Step 1: Choose the Right Account Type

Firstly, ensure that you select the correct account type when setting up your mortgage account. Your mortgage should be set up as a "Liability/debt/Loan" type of account. This is important because transferring money from an asset account (such as your checking account) to another asset account would incorrectly increase the balance in the second account.

Step 2: Set Up the Mortgage Account

Go to the “Tools” menu, then “Account List”, and click “Edit” adjacent to your mortgage account. Here, you can verify and edit the account type to ensure it is set up correctly. You can also adjust payment reminders and payments in this section.

Step 3: Deactivate Auto-Sync (Optional)

If you prefer to manually track your mortgage, go to your "Mortgage Account" settings and deactivate auto-sync. Then, go to "Account Details" and "Display Options" to uncheck the box "Hide in transaction entry lists". This will give you more control over your mortgage tracking and allow you to make manual adjustments.

Step 4: Create an Asset Account (Recommended)

While optional, creating an asset account to go along with your mortgage loan is highly recommended. This will give you a more accurate picture of your net worth. After setting up your mortgage account, Quicken may prompt you to create this asset account. Name the account (e.g., "House") and update the balance to reflect the current market value of your home.

Step 5: Track Your Payments

Quicken offers a built-in mortgage tracker that allows you to track your payments, principal balance, interest rates, loan amortization, and monthly mortgage payments. You can also use the loan calculator to explore different payment scenarios and understand how they impact your payoff plan.

By following these steps, you'll be well on your way to effectively setting up and managing your new mortgage account in Quicken. Remember to refer to Quicken's help resources and community forums for additional guidance and to address any specific questions or issues that may arise.

Selling Your Owner-Financed Mortgage: Exploring Your Options

You may want to see also

![]()

Tracking monthly payments

It is also recommended that you create a home asset account to get a full picture of your net worth. This can be done by clicking 'Add linked asset account' and then 'House'. You can then update the balance of this account to reflect the current market value of your home.

If you want to track each individual line item in your mortgage, you can add all your payment details, and Quicken will keep up with your statement breakdown every month. This will allow you to see exactly how much you are paying for mortgage interest, insurance, property taxes, and any other line items you wish to track.

For those with jointly-held mortgages, it is recommended that you only record one-half of the mortgage and property in your Quicken data file. When you receive a check from the other owner, you should enter the deposit in Quicken in the category field as "Due to/from [Name]". When you pay the full amount of the mortgage payment, you should split the entry, entering one-half to "Due to/from [Name]" and the remaining half being split between "Loan Payment - Interest" and "Loan Payment - Principal".

Maximizing Mortgage Savings: Strategies for Financial Freedom

You may want to see also

![]()

Reducing loan balance

To track your mortgage in Quicken, it is recommended that you set up your mortgage account as a "manual" account. This will allow you to have more control over your transactions and ensure that your payments are correctly categorised.

Set up your mortgage account as a "manual" account

When setting up your mortgage account in Quicken, choose the ""offline (manual)" option. This will give you more flexibility in managing your transactions and categorisations.

Categorise your expenses correctly

Ensure that your mortgage expenses are correctly categorised. Create categories such as "House Interest" and "House Principal" to reflect the different components of your mortgage payments. This will help you track your expenses accurately.

Make manual adjustments

If your auto loan payments are not reducing your loan balance automatically, you may need to make manual adjustments each month. This can be done by creating a transaction in your checking account and then transferring the same amount to the loan principal in your loan account.

Deactivate auto-sync

If your mortgage account is synced with your bank, consider deactivating auto-sync. This will give you more control over categorising your transactions and reducing your loan balance. Go to your "Mortgage Account", "Edit Account", and deactivate auto-sync. Then, go to "Account Details" and uncheck the box "Hide in transaction entry lists".

Update the loan balance

If your Quicken loan balance does not match your bank's loan balance, you can update the balance in Quicken. Look for the gear icon in the upper right corner of the loan account, click on "Update Balance", and enter the actual loan balance.

Review the loan register

If your connected loan balance is not reflecting the lender's balance, try deactivating the loan account temporarily. Review the loan register to identify any discrepancies or errors.

By following these steps and staying on top of your transactions and categorisations, you can effectively reduce your loan balance and keep track of your mortgage in Quicken.

Proving Your Mortgage Payment: Documenting Your Final Payment

You may want to see also

![]()

Tracking jointly held mortgages

Tracking a jointly held mortgage in Quicken requires a few extra steps, but it can be done. Here is a step-by-step guide on how to do it:

Firstly, it is recommended that you only record one-half of the mortgage and one-half of the property in your Quicken data file. This reflects that you only own and owe half of the property and mortgage. You can then set up a new asset account in Quicken, preferably an offline savings account type.

Secondly, when you receive a deposit from the joint owner for their share of the mortgage, enter that deposit in Quicken in the category field as " [Due to/from Joe]" (or the name of the joint owner). When you make the full mortgage payment, split the entry in Quicken. Allocate half of the payment to " [Due to/from Joe]" and split the remaining half (your portion) between "Loan Payment - Interest" and "Loan Payment - Principal".

Additionally, you can set up a phantom checking account and two phantom "partner's equity" or "liability" accounts in the "partnership" file. This approach keeps the property and mortgage amounts intact and reduces potential confusion, especially if other costs are incurred, such as property tax, insurance, or improvements.

Finally, it is important to note that you should manually track your mortgage in Quicken. Go to your mortgage account, deactivate auto-sync, then go to account details, display options, and uncheck the box "hide in transaction entry lists". By manually tracking your mortgage, you can ensure that you can select the loan account in the transfer list.

Topping Up Your Mortgage: What You Need to Know

You may want to see also

![]()

Using the loan calculator

Quicken's built-in loan calculator can be used to see how much time and interest you could save on your mortgage by adding an extra amount to your payment every month or by making an extra lump-sum payment to pay your balance down sooner. This can be done by experimenting with different payment amounts.

To use the loan calculator, you will need to add your loan information. You can find the details you need in your mortgage statement or on your mortgage account website. You can also add your home value in Quicken as an asset account so you can see your equity and include it in your automatic net worth calculation.

To monitor the equity in your home, click the Property & Debt tab, and then click the Property button. You can then view the current value, mortgage balance, and equity. You can also use the What-If tools to choose an earlier payoff date and Quicken will show you how to make it happen.

The loan calculator can also be used to see how much you've paid in principal and interest so far by checking the running totals. To do this, click the Property & Debt tab, then click the Debt button. Click Loan and Debt Options > Loan Details. In the View Loans dialogue, click Choose Loan and select a loan. Click the Payment Schedule tab. The Principal column tells you how much of each payment goes toward the loan principal, and the Interest column tells you how much goes toward the loan interest.

Unlocking Cash: Withdrawing from Your Mortgage

You may want to see also

Frequently asked questions

Set up your mortgage account as an "offline (manual)" account in Quicken. You can also add an asset account to record any improvements you make to your home over the years, thereby reducing your tax liability when you sell.

Quicken's built-in mortgage tracking features allow you to track your payments and principal balance. You can also use Quicken's loan calculator to see how much time and interest you could save by adding an extra amount to your monthly payments.

The cleanest way to set up a jointly held mortgage in Quicken is to record one-half of the mortgage and one-half of the property in your Quicken data file. When you deposit their check, enter that deposit in Quicken in the category field as [Due to/from Joe]. When you pay the mortgage payment for the full amount, split the entry by entering one-half of the payment to [Due to/from Joe] and the remaining half being split between the "Loan Payment - Interest" and "Loan Payment - Principal".

It is not recommended to sync your mortgage in Quicken with your bank as this will prevent you from selecting the loan account in the transfer list. It's better to manually track your mortgage in Quicken.