Home equity is the difference between the current value of your home and the outstanding balance of your mortgage. In other words, it is the portion of your home that you own outright. As you pay down your mortgage, your equity increases. Equity can be a powerful financial tool that you can use to pay off debt, renovate your home, or make other financially savvy decisions. You can access your home equity through a cash-out refinance, a home equity loan, a HELOC, or a reverse mortgage. It's important to use your home equity in ways that will strengthen your financial profile.

How to use equity for a mortgage

| Characteristics | Values |

|---|---|

| Definition of home equity | The amount of your house that you own outright or the difference between your outstanding mortgage and your home's total value. |

| How to calculate home equity | Subtract your remaining mortgage balance from your home's current market value. |

| How to build equity | Make a down payment, pay off your mortgage, increase your home's value through renovations and improvements, or stay in your home to take advantage of any increase in its value. |

| How to use equity | Pay off debt, renovate your home, make other financially savvy decisions, fund major purchases, or pay for college tuition. |

| Types of equity loans | Cash-out refinance, home equity loan, HELOC (Home Equity Line of Credit), reverse mortgage. |

What You'll Learn

![]()

How to calculate your home equity

Home equity is the difference between your home's value and the amount you still owe on your mortgage. In other words, it is the portion of your home that you own outright.

There are several ways to calculate your home equity. One way is to use a home price estimator, such as Zillow or Redfin, to get an estimate of your home's market value. You can also research similar home sales in your area to estimate your home's value. Once you have your home's value, you can calculate your equity by subtracting what you still owe on your mortgage. This information can be found on your monthly statement or online account.

Another way to calculate your home equity is to use a home equity calculator. You can also get a professional appraisal to determine your home's value, although this can cost hundreds of dollars.

It's important to note that your equity will increase as you pay down your mortgage and as your home's value increases. Making improvements to your home, such as adding an extra bedroom or renovating the kitchen, can also increase its value and boost your equity.

You can access your home equity through a cash-out refinance, a home equity loan, a HELOC (home equity line of credit), or a reverse mortgage. A cash-out refinance allows you to take out a new mortgage at a higher loan amount and receive the difference in cash. A home equity loan, on the other hand, is a second mortgage that requires a separate payment. A HELOC is a line of credit that lets you tap into your home equity, and a reverse mortgage converts your equity into cash, which can be useful for those aged 62 or older.

Viewing Your Wintrust Mortgage Statement: A Step-by-Step Guide

You may want to see also

![]()

How to increase your home equity

Home equity is the difference between your home's value and the amount you still owe on your mortgage. In other words, it is the portion of your home that you own outright. You can calculate your equity by taking your home's current market value and subtracting what you still owe on your mortgage.

- Make a larger down payment: The more money you pay upfront for your home, the more equity you will have from the start. This is because your down payment instantly becomes your equity stake in the home.

- Pay your mortgage: Every time you make a payment on your mortgage, you reduce your principal (the balance of your loan) and build equity. You can build equity faster by making bi-weekly payments instead of monthly payments, or by paying extra each month.

- Increase the value of your home: Renovations and improvements can increase the value of your home and drive up your equity. Reliable ways to increase your home's value include adding an extra bedroom, renovating an outdated kitchen, or adding a bathroom. Investing in landscaping and adding curb appeal can also help.

- Wait for the market value of your home to increase: In a strong housing market, the value of your home may increase on its own, which will also increase your equity.

Once you have built up enough equity, you can access it through various financial products, such as a cash-out refinance, a home equity loan, or a HELOC (Home Equity Line of Credit). These products can be used to access cash or to make financially savvy decisions, such as paying off debt or renovating your home.

Understanding Mortgage Submission Process for Your Homestead

You may want to see also

![]()

Using equity to pay off debt

Home equity is the difference between your home's value and the amount you still owe on your mortgage. In other words, it is the portion of your home that you own outright. You can calculate your equity by taking your home's current market value and subtracting what you still owe on your mortgage.

As you pay down your mortgage, your equity grows, contributing to your overall net worth. You can access your home equity through a cash-out refinance, a home equity loan, a HELOC (home equity line of credit), or a reverse mortgage. A cash-out refinance allows you to take out a new mortgage at a higher loan amount, replacing your current mortgage and giving you the difference in cash. A home equity loan is a second mortgage on your home, with a separate set of terms and its own fixed interest rate. A HELOC works like a credit card, giving you access to a credit line that you can draw from and pay back as needed during a certain time period. It carries a variable interest rate, so your payments may fluctuate. A reverse mortgage converts your equity into cash and is an option for those 62 or older.

Using a home equity loan to pay off debt may be an effective strategy for those with enough equity in their homes and who can secure competitive interest rates. The advantages of using home equity loans to pay off debt include lower interest rates compared to unsecured borrowing options such as credit cards and personal loans, fixed repayment terms that can help with budgeting, and higher borrowing limits. However, it is important to remember that you are simply shifting your debt from one form to another, and if you default on a home equity loan, you could lose your home. Additionally, there is a risk of paying more in overall interest over the life of the loan compared to other forms of debt.

Before using a home equity loan to pay off debt, it is essential to carefully consider the benefits and risks. Compare lenders, research products, and run the numbers on debt consolidation opportunities to ensure that this strategy aligns with your long-term financial goals.

Exploring Options: Strategies to Temporarily Pause Mortgage Payments

You may want to see also

![]()

Using equity to fund expenses

Home equity is a powerful financial tool that can be used to fund expenses. It is the difference between the current value of your home and the outstanding balance of your mortgage—in other words, the portion of your home's value that you own outright. As you make payments on your mortgage, you reduce your principal balance and build equity.

There are several ways to access and use your home equity to fund expenses:

- Home equity loan: This is a second mortgage on your home. It doesn't replace your current mortgage but instead requires a separate payment. You can use the funds from a home equity loan for various expenses, such as debt consolidation, home renovations, or other financially savvy decisions.

- Home Equity Line of Credit (HELOC): A HELOC is a revolving line of credit, similar to a credit card, that comes with a variable rate. You can borrow, repay, and then reuse funds as needed during a set draw period and then pay off your balance during a repayment period. HELOCs can be useful for funding expenses like home improvements, emergency expenses, or retirement income supplementation.

- Cash-out refinance: This option allows you to take out your equity by getting a new mortgage at a higher loan amount. You replace your current mortgage with a bigger one and receive the difference in cash. A cash-out refinance typically takes between 30 and 45 days to complete, and you usually need to leave some equity in the home (around 20%).

- Reverse mortgage: If you're 62 or older and own a home with significant equity, a reverse mortgage can supplement your income and help you stay in your home. It converts your equity into cash, which you can receive as a lump sum, a line of credit, or a series of regular payments. However, financial experts generally recommend against using equity to fund everyday expenses or purchases that won't provide long-term value, such as buying a car or taking a vacation.

It's important to carefully consider your financial situation and goals when deciding whether to use home equity to fund expenses. While it can provide access to cash, it also adds to your overall debt and can extend the time it takes to pay off your mortgage. Additionally, you should have a plan for repaying any loans or lines of credit taken out against your home equity.

Reaffirming Your Mortgage After Chapter 7: What You Need to Know

You may want to see also

![]()

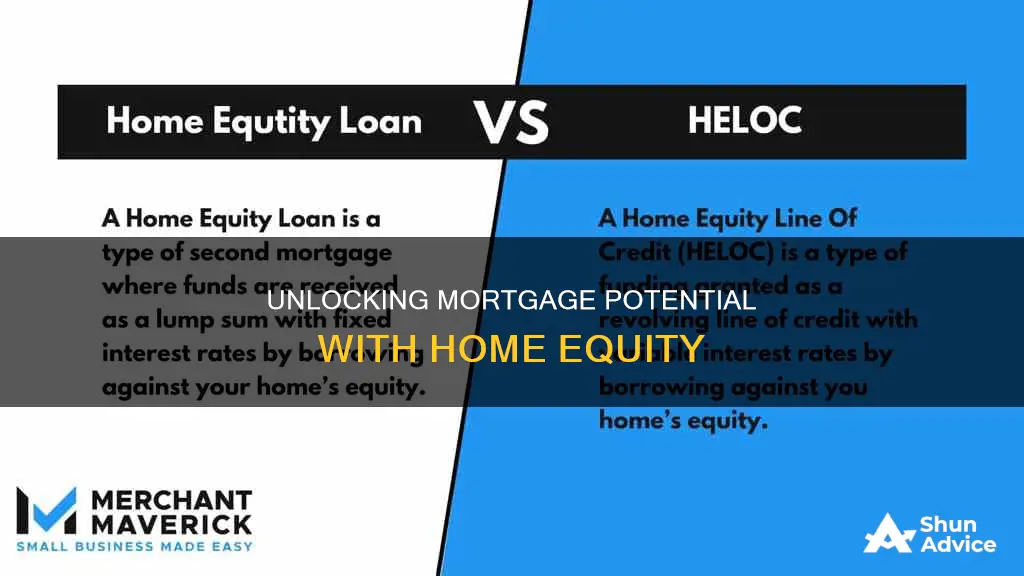

Equity loans and HELOCs

Home equity is the difference between the current value of your home and the outstanding balance of your mortgage. In other words, it is the portion of your home that you own outright. You can calculate your equity by taking your home's current market value and subtracting what you still owe on your mortgage.

Once you have built up enough equity, you can access it through a cash-out refinance, a home equity loan, a HELOC, or a reverse mortgage. A home equity loan is a second mortgage on your home. It does not replace your current mortgage but is a separate payment. A home equity loan provides a lump sum with fixed interest rates and predictable payments. You can use the lump sum for various purposes, such as renovating your house, consolidating debt, covering an emergency expense, or funding a major life event.

A HELOC, or Home Equity Line of Credit, is a revolving line of credit that allows you to borrow money as needed during a draw period before entering a repayment period. It works similarly to a credit card, with variable interest rates and flexible withdrawal options. During the draw period, you can withdraw money, repay it, and then draw again within your available credit. During the repayment period, you can no longer withdraw money and must make principal and interest payments until the loan is paid off. A HELOC can be useful for unpredictable or spread-out costs, such as ongoing home renovations, medical bills, or tuition payments.

Both home equity loans and HELOCs typically have lower interest rates than unsecured debt like credit cards and personal loans. Additionally, if you use the funds for major home improvements, you may qualify for a tax deduction on the interest paid. However, it is important to remember that your home serves as collateral for these loans, and it could be at risk if its value drops or your income is interrupted.

Registering a Mortgage in QLD: What You Need to Know

You may want to see also

Frequently asked questions

Home equity is the amount of your house that you own outright. In other words, it is the difference between your outstanding mortgage and your home's total value.

To calculate your home equity, subtract your remaining mortgage balance from your home's current market value.

You can build your home equity by making mortgage payments, increasing the value of your home through renovations and improvements, and making a large down payment.

You can use your home equity for various expenses, such as home improvements, debt consolidation, education costs, or other large purchases. You can access your home equity through a cash-out refinance, a home equity loan, a HELOC, or a reverse mortgage.

A home equity loan is a lump sum loan with a fixed rate and term, usually used for large expenses or projects. A HELOC is a revolving line of credit with a variable interest rate, allowing you to borrow up to a certain limit over time and make interest-only payments.