Mortgage-backed securities (MBS) are bonds created from residential mortgages, providing income to investors. They are a type of fixed-income instrument that pools individual mortgages into a single security. MBS investors essentially lend money to home buyers and in return, receive the rights to the value of the mortgage, including interest and principal payments made by the borrower. MBS are generally considered safe investments that provide higher yields than US government bonds, making them attractive to investors seeking low-risk investments or steady income streams. However, they also played a significant role in the 2008 financial crisis due to high-interest rates, low housing prices, and risky lending practices.

| Characteristics | Values |

|---|---|

| Type of security | Mortgage-backed security (MBS) |

| What it's like | A bond created out of residential mortgages |

| Who it's for | Investors |

| Income | Interest and principal payments made by the borrower |

| Risk | Relatively safe investment with higher yields than US government bonds |

| Pros | Steady income stream, federal government backing, monthly income, fixed-rate interest |

| Cons | Limited potential for price growth, uncertain term, may not increase in value like other bonds |

| Causes of 2008 financial crisis | High interest rates, low housing prices, risky lending practices, fully funding home loans, removal of lending restrictions |

| Other fees | Origination fees, processing fees, application fees, underwriting fee |

What You'll Learn

![]()

Mortgage-backed securities (MBS)

The process of creating an MBS begins with the origination of mortgages by a financial institution, such as a bank, which are then secured by the properties being bought. These mortgages are then pooled together with other mortgages with similar characteristics, such as interest rates and maturity dates. The pooled mortgages are then sold to a trust, a government-sponsored enterprise (GSE) like Fannie Mae, Freddie Mac, a government agency like Ginnie Mae, or a private financial institution. The trust then structures these loans into MBS and sells them to investors.

The investors who buy MBS are essentially lending money to the home buyers in the pool. In return, they receive periodic payments, including interest and principal repayments from the underlying mortgages. The interest payments to investors come from the monthly repayments made by the mortgage holders. MBS can thus be seen as a way of providing income to investors.

MBS offer benefits to the players in the mortgage market, including banks, investors and mortgage borrowers. However, they also come with risks. MBSs were a major factor in the 2008 financial crisis, as high-interest rates, low housing prices and risky lending practices led to continued defaults on loans, causing a domino effect of collapsing MBSs that wiped out trillions of dollars from the US economy.

Purchasing Mortgage Leads: A Guide for Beginners

You may want to see also

![]()

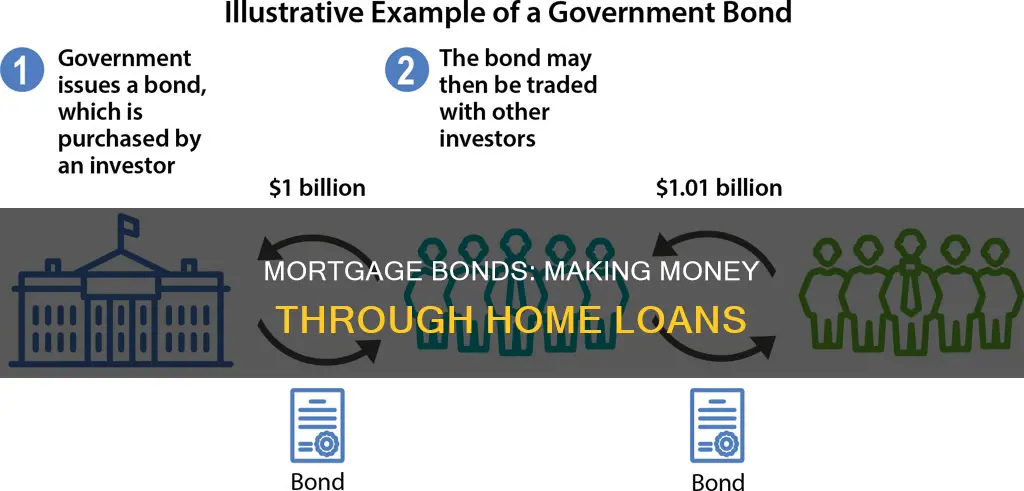

MBS vs. traditional bonds

Mortgage-backed securities (MBS) are investments similar to bonds. Each MBS consists of a bundle of home loans and other real estate debt bought from the banks that issued them. MBSs are national and international in scope and are regionally diversified. They help move interest rates out of the banking sector and facilitate greater specialisation among financial institutions.

Traditional bonds, on the other hand, are essentially borrowing money from investors (the people buying the bond). As with any loan, interest payments are made, and then the principal is paid back at maturity.

MBSs are considered relatively low-risk investments, given the government backing for most of them. They also pay a fixed interest rate that is usually higher than US government bonds. They typically offer monthly payouts, while bonds offer a single lump-sum payout at maturity.

However, MBSs may have "led inexorably to the rise of the subprime industry" and "created hidden, systemic risks". They also "undid the connection between borrowers and lenders". Historically, "less than 2% of people lost their homes to foreclosure", but with securitisation, "once a lender sold a mortgage, it no longer had a stake in whether the borrower could make their payments."

The decision to invest in MBSs or not ultimately depends on your financial goals, circumstances, and risk tolerance. MBSs are generally seen as relatively safe investments and often provide higher yields than US government bonds. However, they offer limited potential for price growth, so if you are seeking larger returns and can tolerate higher risk, MBSs may not be ideal.

Resetting Your Mortgage: A Guide to Starting Over

You may want to see also

![]()

MBS and the 2008 financial crisis

Mortgage-backed securities (MBS) are like bonds created out of residential mortgages, providing income to investors. They are fixed-income instruments that pool individual mortgages into a single security. MBS offer federal government backing, monthly income, and a fixed rate of interest.

MBS played a key role in the 2008 financial crisis. Securitization of mortgage debt in bond-like investments such as MBS and collateralized debt obligations (CDOs) was a significant cause of the crisis. Securitization of home mortgages encouraged excessive risk-taking throughout the financial sector, from mortgage originators to Wall Street banks.

The process of securitization involves packaging multiple mortgages into bond-like investments for investors to purchase and gain exposure to the mortgage market, which would otherwise be difficult. This process led to the subprime meltdown as poorly reviewed mortgages began to default, impacting the income streams on these securitized products.

In the mid-2000s, banks issued an unusually large number of mortgages, many of which were subprime and given to low-quality borrowers. The banks then sold these mortgages to bigger banks, which packaged them into MBS and CDOs. By March 2007, the value of subprime mortgages had reached around $1.3 trillion. However, many borrowers could not afford their payments, and the housing market went into a free fall. As a result, the value of MBS plummeted, and financial institutions holding these securities scrambled to get rid of them, triggering the financial crisis.

The crisis was further exacerbated by the interconnectedness of financial institutions within and across countries, with foreign claims by banks from the five major advanced economies increasing from $6.3 trillion in 2000 to $22 trillion by June 2008.

Solo Mortgage Applications: A Comprehensive Guide

You may want to see also

![]()

MBS investors

Mortgage-backed securities (MBS) are investments similar to bonds. Each MBS is a share in a bundle of home loans and other real estate debt purchased from banks or government entities. MBS investors receive periodic payments, like bond coupon payments, which typically offer monthly payouts. MBS investors benefit from the mortgage business without needing to buy or sell home loans themselves.

Making Woolwich Mortgage Overpayments: A Step-by-Step Guide

You may want to see also

![]()

MBS and interest rates

Mortgage-backed securities (MBS) are fixed-income instruments that pool individual mortgages into a single security. They are like bonds created out of residential mortgages, providing income to investors. MBS investors essentially lend money to home buyers and in return, get the rights to the value of the mortgage, including interest and principal payments made by the borrower.

The interest payments to investors come from the thousands of mortgages underlying the bond—specifically, the repayments in interest and principal the mortgage holders make each month. During the accrual period, interest is not paid to investors; instead, the principal increases at a compound rate. After prior tranches are paid off, Z-tranche holders will receive coupon payments based on the bond's higher principal balance. MBS can also be stripped, where investors are paid the principal only (PO) or interest only (IO).

The price of MBS moves in direct proportion to the prices of the mortgages from which they are derived. When demand for a bond is low, sellers may lower the price to encourage investors to buy. As a result, the yield goes up because the same money from the investor buys more shares. MBS prices are also influenced by the macroeconomic climate, such as inflation rates. High inflation, for example, makes investors seek higher yields.

MBS are generally considered relatively safe investments and often provide higher yields than US government bonds. However, they offer limited potential for price growth. MBS were a key factor in the 2008 financial crisis, where high interest rates, low housing prices, and risky lending practices led to continued defaults on loans.

Generate Mortgage Leads: Strategies for Success

You may want to see also

Frequently asked questions

MBS are like bonds created out of residential mortgages, providing income to investors. They are fixed-income instruments that pool individual mortgages into a single security.

Investors make money from MBS by receiving interest and principal payments from the underlying mortgages. The interest credited during the accrual period is taxable, even though investors don't actually receive it. MBS can also be sold to other investors.

MBS have been blamed for causing economic turmoil, most notably in 2008. This was due to high interest rates, low housing prices, and risky lending practices, which led to many borrowers defaulting on their loans. MBS may also offer limited potential for price growth compared to other investments.