In the UK, a 5% deposit mortgage is a type of mortgage where you pay 5% of the total value of the property as a deposit. This scheme was launched by the UK government in April 2021 to encourage lenders to offer 95% LTV mortgages. To qualify for a 5% deposit mortgage, you must meet certain criteria, such as being a British citizen or having UK residency status, and purchasing a property under £600,000 as your main residence. Before applying for a mortgage, it is important to check your credit score and ensure that you have all the necessary documents, such as proof of deposit and income. While there is no guarantee of acceptance, improving your credit score, demonstrating financial management skills, and having a steady income can increase your chances of approval.

5-times salary mortgage characteristics and values

| Characteristics | Values |

|---|---|

| Credit score | The higher the score, the more likely the approval. Scores in the range of 720-850 are considered "excellent". Scores in the 300-629 range are "bad". |

| Down payment | Ideally, 20% of the home's sale price to avoid additional monthly fees. If the down payment is less than 20%, you will likely need to purchase Private Mortgage Insurance (PMI). |

| Debt-to-income ratio | The lower the ratio, the better the mortgage terms. |

| Spending habits and outgoings | The more prudent and stable you are, the stronger your application will be. |

| Profession and earnings | Some lenders base the criteria on profession and salary. For example, Teachers Building Society requires a minimum salary of £200,000 for more than 5x multiple incomes. |

| Deposit amount | 5x salary mortgages will demand at least a 15% deposit. |

| Lender | NatWest, Together Mortgages, and Nationwide (through the Helping Hand scheme) offer 5x salary mortgages. |

| Affordability | You will need to prove you can afford the monthly payments to qualify for the mortgage. |

| Eligibility | To qualify for a 5.5x mortgage, you must earn at least £37,000 as a solo applicant. If you are buying with another person, the collective income must be £55,000 or more. |

What You'll Learn

![]()

Understand the application process and what is expected of you

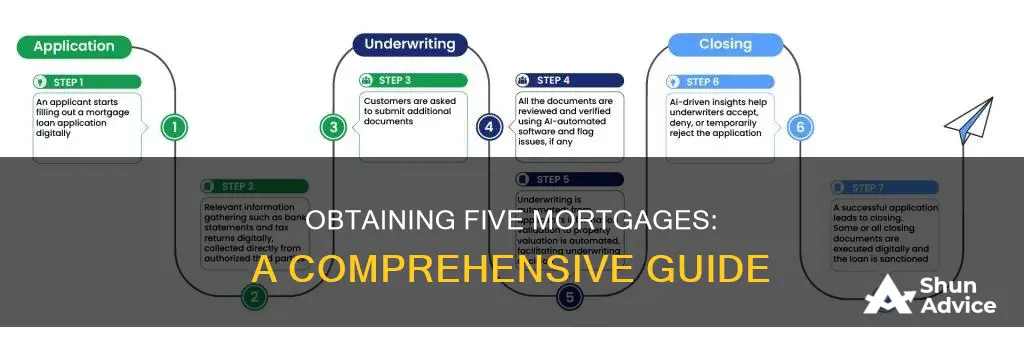

Understanding the application process and what is expected of you is crucial when applying for a mortgage. The process is complex and can be lengthy, so it is important to be prepared and organised. Here is a step-by-step guide to help you navigate the mortgage application process:

Step 1: Preparation

Before applying for a mortgage, you need to ensure your finances are in order. Lenders will scrutinise your credit score, assets, income, debts, and debt-to-income ratio to determine your eligibility and mortgage rate. It is recommended to review your credit report from the three major credit bureaus: Experian, Equifax, and TransUnion. You can access free weekly reports from AnnualCreditReport.com. Make sure your financial history for the previous 6-12 months is clean, without late bill payments or high debt. Additionally, consider the type of home you want and your budget for the down payment.

Step 2: Pre-qualification (optional)

Pre-qualification is an optional step where you provide lenders with a basic summary of your financial situation. They will then give you an "unofficial" estimate of how much you can borrow. This step can give you a quick idea of your eligibility but is not as strong as pre-approval.

Step 3: Pre-approval

Pre-approval is a crucial step before you start house shopping. It involves providing the lender with detailed financial information, including income, credit score, debts, assets, and employment history. The lender will then officially approve the amount you can borrow. Pre-approval gives you a clear budget for your home search and makes your offers more competitive. It is valid for a limited time, usually 30 to 90 days, so be mindful of the timing.

Step 4: House shopping

With your pre-approval in hand, you can now start searching for your dream home. Consider your needs and preferences, such as the type of home (single-family, condo, etc.), location, and your long-term plans. Remember, the pre-approval amount is the maximum you can borrow, so ensure you stay within your budget.

Step 5: Making an offer

Once you've found the perfect home and your offer is accepted, inform your lender that you want to move forward with their loan offer. Submit a letter of intent to lock in your rate and terms, and the lender will initiate the underwriting process.

Step 6: Underwriting

The underwriting stage is when mortgage underwriters, the key decision-makers, carefully examine all the information about you and the property. They will order an appraisal of the property to ensure it is worth the amount being lent. The underwriter's assessment will result in either accepting, rejecting, or conditionally approving the loan.

Step 7: Closing

The closing stage is the final step in the mortgage process. You will receive a Closing Disclosure detailing your loan terms, including monthly payments, down payment, interest rate, and closing costs. Compare this to your Loan Estimate to ensure consistency. Attend a closing meeting to ask any last-minute questions and bring the required documents, such as a valid photo ID, down payment, and closing costs. Once you sign the loan, you officially become a homeowner!

Employment Verification: A Crucial Step in Mortgage Approval

You may want to see also

![]()

Research and compare lenders to find the best rates

Researching and comparing lenders is an important step in finding the best rates for your 5% mortgage. Here are some detailed tips to help you through this process:

Understand the Different Types of Lenders:

Firstly, familiarize yourself with the different types of mortgage lenders available. These include national or regional banks, credit unions, mortgage brokers, and online-only lenders. Each type has its own unique characteristics and offerings. For example, banks are the most common type of mortgage lender and typically offer a wide range of loan options. Credit unions, being non-profits, often charge lower fees and offer competitive loan terms. Online-only lenders may offer low-interest rates and many loan options but may lack personalized services.

Decide on Fixed or Adjustable Rates:

Before reaching out to lenders, decide whether you prefer a fixed-rate or adjustable-rate mortgage. Fixed-rate mortgages have the same interest rate for the entire loan term, providing stability and predictability. Adjustable-rate mortgages have fluctuating interest rates, which may result in lower initial payments but can increase over time.

Compare Interest Rates and Fees:

Interest rates can significantly impact your overall loan cost. Compare the annual percentage rate (APR), which reflects the total cost of the mortgage, including both the interest and any associated fees. Additionally, consider the loan term, as shorter terms often result in higher monthly payments, while longer terms may provide more affordable payments. Don't forget to ask lenders for detailed breakdowns of their fees to ensure you understand the total cost of the mortgage.

Shop Around:

Don't settle for the first lender you find. Compare at least three to five lenders to increase your chances of finding the best deal. You can use online comparison sites to efficiently obtain multiple quotes, ensuring that your quotes are for the same loan type and are provided on the same day.

Understand Your Credit Score:

Your credit score plays a crucial role in determining the interest rate you'll be offered. Lenders typically review scores from three major credit bureaus (Equifax, Experian, and TransUnion) and use the middle score. A higher credit score can lead to a lower interest rate, so understanding your credit score can help you negotiate better terms.

Seek Recommendations:

Ask your friends and family for referrals and recommendations. They can share their experiences with different lenders and provide valuable insights. Additionally, consider working with a mortgage broker who, for a fee, can help you find and compare different lenders to fit your specific needs.

Remember, taking the time to research and compare lenders can save you a significant amount of money in the long run. Don't rush the process, and don't be afraid to negotiate to get the best possible deal for your 5% mortgage.

Strategies for Affording a Mortgage: Financial Planning Tips

You may want to see also

![]()

Get pre-approved for a loan to save time later

Getting pre-approved for a loan can save you time later on in the mortgage application process. Pre-approval differs from pre-qualification in that it involves a more rigorous process, including a hard credit check, and results in a commitment from the lender to provide you with a specified loan amount. Pre-approval is generally valid for 60 to 90 days.

To get pre-approved, you will need to submit an application to your lender of choice. This application will require documentation to verify your employment history, creditworthiness, and overall financial situation. The specific documents required may vary depending on your circumstances and the type of mortgage you are applying for, but typically include identifying documents (such as a driver's license or passport), pay stubs, tax returns, bank account statements, and investment account statements.

It is important to note that pre-approval does not obligate you to formally apply for a loan with that lender. You can still shop around and apply with multiple lenders to compare offers and find the lowest rate. Many lenders have online application portals, allowing you to apply for pre-approval entirely online.

By getting pre-approved, you can save time later in the process when you are ready to make an offer on a house. The lender will already have most of the information they need to move forward with the loan, and you will have a strong sense of how much money you can borrow to buy a home.

Profiting from Real Estate Mortgages: A Beginner's Guide

You may want to see also

![]()

Know what documentation you need to provide

When applying for a mortgage, you'll need to prove your identity, income, and deposit. Here is a list of documents you may need to provide:

Proof of Identity

A passport or driving license are the most commonly used documents for proof of ID. However, other forms of ID may be accepted if you don't have these. Ensure that your chosen form of ID is in date.

Proof of Income

You will need to provide evidence of your income, such as your latest payslip. If you are paid in a foreign currency or your source of income is outside the UK, you will need your latest three months' worth of payslips. If you are self-employed, you will need to provide additional documents, such as tax returns and bank statements. Lenders will also consider your outgoings, including household bills, credit card debts, and other loans, to assess whether you can afford the monthly mortgage repayments.

Proof of Deposit

You will need to provide proof of your deposit, such as savings statements or a completed form from someone who has gifted you the money. If your deposit is from your savings, you may need to provide evidence via bank statements, and any large payments will need to be explained.

Other Documents

Other documents that may be required include council tax bills, utility bills, and bank statements dated within the last three months. Foreign nationals will need to provide additional documentation to prove their residency in the UK. If you are a foreign national who has lived in the UK for less than 12 months, you will need to provide a credit report from your previous country of residence and the latest three months of bank statements for all non-resident accounts.

Single Homeowners: Strategies for Affording a Mortgage

You may want to see also

![]()

Understand the costs and terms of the loan

Understanding the costs and terms of a mortgage loan is crucial before making any commitments. Here are some key points to consider:

Loan Terms

The loan term refers to the length of time you have to repay the loan. Typically, mortgage loans have terms of 10, 15, 20, or 30 years. The longer the term, the lower your monthly payments, but the more interest you'll pay over the life of the loan. Shorter-term loans generally save you money overall but result in higher monthly payments.

Interest Rates

Interest rates can be fixed or adjustable. Fixed-rate mortgages maintain the same interest rate for the entire term, making budgeting easier with predictable payments. On the other hand, adjustable-rate mortgages (ARMs) offer lower initial interest rates that can increase or decrease based on market changes. ARMs may be listed as "3-1," "5-1," or "7-1," indicating the number of years the initial rate is locked in before adjustments.

Principal and Interest

The principal is the amount of money you borrow from the lender. Your monthly payments consist of repaying this principal and the interest charged on it. In the early stages of the mortgage, a larger portion of your payment goes towards interest, with the balance shifting towards the principal in later years.

Taxes and Insurance

Some mortgage payments include property taxes and insurance. Property insurance covers the home and its contents from fire, theft, and other disasters. Additionally, if your down payment is less than 20%, you may be required to pay private mortgage insurance (PMI) to protect the lender in case you default on the loan.

Closing Costs

Closing costs, or "settlement costs," are upfront charges associated with obtaining the loan and transferring ownership of the property. These costs are paid at closing and may include fees such as the appraisal fee, attorney fees, and title insurance, among others. Ensure you have sufficient funds to cover these costs, as they can be substantial.

Prepayment Penalties and Other Fees

Some loans may include prepayment penalties, balloon payments, or negative amortization. A prepayment penalty is a fee charged if you pay off your loan early. A balloon payment is a large, lump-sum payment that may be required at specific intervals or at the end of the loan term. Negative amortization occurs when the monthly payment is less than the interest charged, causing the loan balance to increase over time.

Loan Estimates

Obtain Loan Estimates from multiple lenders to compare costs and terms. A Loan Estimate details important information about your mortgage, including the loan term, interest rate, estimated monthly payments, closing costs, and more. Review these estimates carefully and ask questions if you notice any discrepancies or unexpected charges.

Add Your Mortgage Account: A Guide for Wells Fargo Customers

You may want to see also

Frequently asked questions

The first step is to research lenders and compare interest rates and fees. Once you have found a lender and mortgage that suits your needs, you can get pre-approved for the loan.

Lenders typically ask for identification documents (e.g. driver's license, passport), pay stubs, tax returns, bank account statements, and investment account statements. You may also need to provide additional documents, such as proof of the source of your down payment funds.

To get pre-approved, you will need to provide the lender with documentation to verify your employment history, creditworthiness, and overall financial situation. The lender will also check your credit history by obtaining a credit report.

A rate lock guarantees that the interest rate and discount points are fixed until the lock's expiration date. If you want to protect yourself against rising interest rates, you may want to lock in your rate. However, if you believe that interest rates will decrease in the near future, you may choose to wait.

The entire process, from application to closing, can take anywhere from two weeks to two months.