Paying off your mortgage early can save you a lot of money, but it's not always straightforward. The amount you'll save depends on a few factors, such as the interest rate on your loan, the remaining balance, and how much extra you can afford to pay each month. You can use a mortgage payoff calculator to help you estimate how much you can save and how much time you can cut off your repayment term. These calculators can be found on websites like NerdWallet, MortgageCalculator.org, and Bankrate.

| Characteristics | Values |

|---|---|

| Mortgage payoff calculator | Ramsey, NerdWallet, Bankrate, Mortgage Calculator, MortgageLoan, Calculator.net |

| Mortgage payment | Principal and interest payment |

| Extra payments | Help to save money on interest and pay off the loan faster |

| Prepayment penalty | A fee that can be charged if the mortgage is paid off early |

| Amortization | The process of paying off debt with a planned, incremental repayment schedule |

| Mortgage refinancing | Another strategy to shorten the term and obtain lower interest rates |

What You'll Learn

![]()

Extra payments

If you can afford to make extra payments, you could save on interest and pay off your mortgage sooner. However, if your savings are depleted after making your down payment and paying closing costs, you should prioritise building an emergency savings fund first.

There are several ways to make extra payments. You can pay a little extra each month, make a one-time lump-sum payment, or refinance to a shorter-term loan. If you can refinance with a lower interest rate, for a shorter term, you will pay higher monthly payments and closing costs, but your overall interest expense will be significantly lower.

Before making extra payments, ask your mortgage servicer for instructions. You may have to specify that the extra payment should go towards the principal balance, not interest or future payments. Each servicer will have its own process.

You can use a mortgage payoff calculator to help you evaluate how extra payments can save you money on interest and shorten your mortgage term.

Understanding Mortgage Calculations in Connecticut

You may want to see also

![]()

Prepayment penalties

It's important to note that prepayment penalties are not always charged. Many mortgage loans do not include them, and they are prohibited for most residential mortgage loans under the Consumer Financial Protection Bureau (CFPB) rules. However, they may be included in the mortgage contract, so it's crucial to read the fine print carefully before agreeing to the loan. If you're unsure, ask your lender about the possibility of a prepayment penalty and request a quote for a similar loan without one to make an informed decision.

The two main types of prepayment penalties are soft and hard. Soft prepayment penalties apply if you refinance or pay off the loan early but not if you sell your home. On the other hand, hard prepayment penalties are stricter and apply when you refinance, pay off the loan, or sell your property.

To avoid unexpected charges, it's essential to understand the specifics of your lender's prepayment penalty policy. These penalties can significantly impact the cost of refinancing a mortgage or selling a home. Additionally, consider using budgeting tools to plan for extra payments and consult a financial advisor to ensure you're making the best decision for your situation.

Requesting a Mortgage Settlement Conference: What You Need to Know

You may want to see also

![]()

Amortization schedules

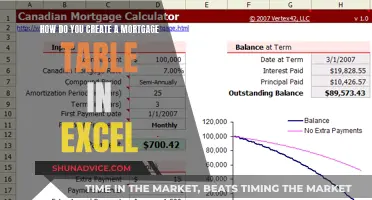

Amortization is the process of paying off debt with a planned, incremental repayment schedule. An amortization schedule can help you estimate how long you will be paying off your mortgage, how much you will pay in principal, and how much you will pay in interest. It is a table that lists each monthly payment from the time you start repaying the loan until the loan matures or is paid off.

The amortization schedule details how much will go toward each component of your mortgage payment—principal or interest—at various times throughout the loan term. Each payment will cover the interest first, with the remaining portion allocated to the principal. When you pay extra on your principal balance, you reduce the amount of your loan and save money on interest.

You can use an amortization calculator to evaluate how adding extra payments or bi-weekly payments can save you interest and shorten your mortgage term. For instance, NerdWallet's early mortgage payoff calculator can help you figure out how much more to pay each month to pay off your mortgage early.

Making changes to how large or frequent your payments are can alter the amount of time you are in debt. If you can comfortably make extra payments, you could save on interest and pay off your mortgage sooner. However, if your savings are depleted after making your down payment and paying closing costs, you should prioritize building up an emergency savings cushion first.

Add Your Mortgage Account: A Guide for Wells Fargo Customers

You may want to see also

![]()

Monthly payments

The interest charge, typically a percentage of the outstanding principal, can be reduced by allocating more funds to the principal. This strategy is particularly effective in the initial years of a loan, when a larger proportion of the payments go towards interest. By prioritising principal repayment, you can decrease the outstanding balance faster, leading to reduced interest charges over time.

To optimise your monthly payments, consider using an early mortgage payoff calculator. These tools can help you determine how much extra you should pay each month to meet your desired payoff timeline. For instance, NerdWallet's calculator allows you to input your mortgage amount, desired payoff timeline, and outstanding balance to estimate your monthly payments and overall interest savings.

Additionally, amortisation schedules can provide valuable insights into your repayment journey. These schedules outline how long you'll be paying off your mortgage, the principal and interest portions, and the impact of payment frequency and size on your debt duration. Understanding amortisation can help you make informed decisions about increasing your monthly payments or making extra payments.

It's important to remember that your monthly mortgage payment may also include other costs, such as homeowners' insurance, property taxes, and private mortgage insurance (PMI). Ensure that you're comfortable with your overall payment, including these additional expenses. Before making extra payments, be sure to check with your lender about any prepayment penalties, as some loans may charge a fee for early repayment.

Adding a Co-Borrower: Adjusting Your Mortgage Agreement

You may want to see also

![]()

Mortgage refinancing

One way to pay off your mortgage early is by making larger monthly payments. You can use an early mortgage payoff calculator to figure out how much more you need to pay each month to pay off your mortgage early. You can also use a mortgage payoff calculator to estimate how much you still owe.

There are several reasons why you may want to refinance your mortgage. Refinancing can help you leverage your home as an investment by allowing you to get cash from your home, lower your payments, and shorten your loan term. It can also be used to add or remove someone from your mortgage. Additionally, refinancing can help you make use of your home's equity, get a better interest rate, and lower your monthly payments.

There are several types of refinancing options:

- Rate and term refinance: This option allows you to change the interest rate and loan terms of your current mortgage.

- Cash-in refinance: This option involves the borrower contributing a lump sum toward their mortgage to increase equity and decrease the amount owed. This can result in a lower monthly payment and interest rate.

- No-closing-cost refinance: With this option, the borrower rolls the closing costs into the principal of the new loan instead of paying them in cash upfront. This results in a higher monthly payment but reduces the cash required to close the loan.

- Cash-out refinance: This option allows you to use your home equity to withdraw cash, increasing your mortgage debt but giving you money to invest or fund projects.

When considering refinancing, it is important to understand the process and ensure it aligns with your financial goals. There may be upfront costs associated with refinancing, so calculating your break-even point is essential. Additionally, the refinancing process includes many of the same steps as the home-buying process, such as a credit check, financial documentation, and an appraisal to determine the home's value.

Understanding Mortgage Co-Signing: What You Need to Know

You may want to see also

Frequently asked questions

A mortgage payoff calculator helps you evaluate how much extra you need to pay to pay off your mortgage early. It calculates the remaining time to pay off your mortgage, the difference in payoff time, and interest savings for different payoff options.

To use a mortgage payoff calculator, you need to input the required information, such as the term length of the remaining loan, the original loan amount, the interest rate, and the monthly payment values. The calculator will then provide you with the remaining balance and the time needed to pay it off.

To pay off your mortgage early, you can make extra payments towards your principal balance. This will help you save money on interest and pay off your loan faster. You can also consider mortgage refinancing, which can help you obtain a lower interest rate and shorten your term.

Paying off your mortgage early can save you thousands of dollars in interest over the life of the loan. It can also help you start your retirement with a fully paid-off home, giving you more financial stability.

Amortization is the process of paying off debt with a planned, incremental repayment schedule. An amortization schedule can help you estimate how long you will be paying off your mortgage, how much you will pay in principal, and how much you will pay in interest. This information can help you understand how to pay off your mortgage early.