Investing in a home can be a lucrative strategy for many individuals seeking to build wealth over time. This approach involves purchasing a property, typically a house or apartment, with the intention of generating income through rent or equity appreciation. Homeownership offers several advantages, such as the potential for long-term capital growth, tax benefits, and the ability to create a stable and secure living environment. Understanding the mechanics of this investment is crucial, as it involves various factors like market trends, mortgage financing, and property management. This paragraph will explore the key aspects of how a home can serve as a viable investment option, providing insights into the benefits and considerations for prospective homeowners.

What You'll Learn

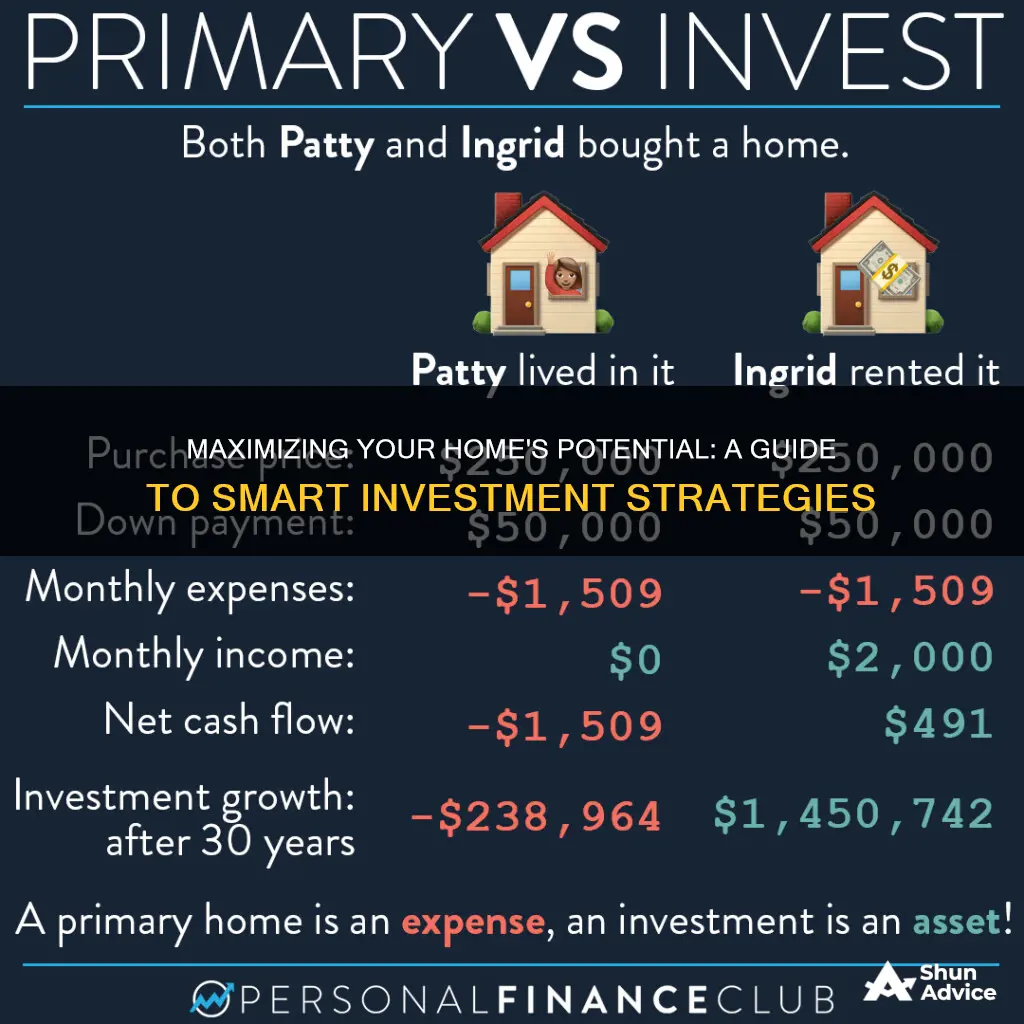

![]()

Return on Investment (ROI): Calculate potential returns over time

When considering a home as an investment, understanding the concept of Return on Investment (ROI) is crucial. ROI is a performance measure used to evaluate the efficiency or profitability of an investment. In the context of real estate, it helps you assess the potential financial gains you can expect from your property over time.

To calculate ROI, you need to determine the potential returns and then compare them to the initial investment. Here's a step-by-step guide:

- Estimate Potential Returns: Start by researching and analyzing the market trends in your desired area. Look at historical data to understand the average annual growth rate of property values in your region. This will give you an idea of how much you might expect your home's value to increase over time. Additionally, consider potential rental income if you plan to rent out the property. Calculate the estimated annual rental yield based on market rates and the expected occupancy.

- Determine Initial Investment: Identify the total amount you invested in purchasing the property. This includes the purchase price, closing costs, and any additional expenses incurred during the buying process. Ensure that you have all the necessary financial records and receipts to accurately calculate this figure.

- Calculate ROI: The formula for ROI is straightforward: ROI = (Net Profit / Initial Investment) * 100. Here, the net profit is the total return on your investment, which includes the increase in property value and any rental income generated. Subtract any expenses related to the investment, such as maintenance costs or property taxes, from the total returns to find the net profit. Then, divide this by the initial investment and multiply by 100 to get the ROI percentage.

For example, if you bought a house for $200,000 and sold it after 5 years for $250,000, with an annual rental income of $10,000, you can calculate the ROI. Assuming no significant expenses during the holding period, the net profit would be $50,000 ($250,000 - $200,000) plus $50,000 in rental income ($10,000 * 5 years), totaling $100,000. With an initial investment of $200,000, the ROI would be (100,000 / 200,000) * 100 = 50%.

Remember, this calculation provides a snapshot of the potential financial gain and should be considered alongside other factors like market conditions, holding period, and personal financial goals. It's essential to conduct thorough research and seek professional advice to make informed decisions regarding real estate investments.

Nokia's Resurgence: Why Investors are Buying

You may want to see also

![]()

Mortgage and Financing: Understand loan options and interest rates

When considering a home as an investment, understanding the mortgage and financing aspects is crucial. This knowledge will empower you to make informed decisions and potentially maximize your returns. Here's a breakdown of the key considerations:

Loan Options:

The first step is to explore the various loan options available. Traditional mortgages are the most common, typically offered by banks or credit unions. These loans can be either fixed-rate or adjustable-rate. Fixed-rate mortgages have consistent interest rates throughout the loan term, providing stability and predictability. Adjustable-rate mortgages (ARMs) start with a lower interest rate but can fluctuate over time, potentially leading to higher monthly payments.

Another option is a government-backed loan, such as an FHA (Federal Housing Administration) loan, which offers more flexible credit requirements and down payment options. VA (Veterans Affairs) loans are available to eligible veterans and active-duty service members, providing 100% financing and no down payment. Understanding the pros and cons of each loan type will help you choose the one that best aligns with your financial situation and investment goals.

Interest Rates:

Interest rates play a significant role in mortgage financing. A lower interest rate means lower monthly payments and less money spent on interest over the life of the loan. When considering investment properties, it's essential to shop around and compare rates from different lenders. Online tools and mortgage calculators can help you estimate monthly payments based on various interest rates and loan terms.

Additionally, consider the impact of market conditions on interest rates. Economic factors like inflation, central bank policies, and market demand can influence rates. Staying informed about these factors can help you anticipate potential changes in interest rates and plan your investment strategy accordingly.

Down Payments and Closing Costs:

The size of your down payment can significantly impact your overall costs and the amount of equity you build in the property. Typically, a larger down payment can lead to better loan terms and lower interest rates. However, it's important to strike a balance between a substantial down payment and having enough cash reserves for other investment opportunities or unexpected expenses.

Closing costs are another essential consideration. These are fees associated with finalizing the mortgage, including appraisal fees, attorney fees, and title insurance. Understanding the average closing costs in your area will help you budget accordingly and potentially negotiate better terms with lenders.

Loan Term and Amortization:

The loan term refers to the length of time you have to repay the mortgage. Common terms include 15, 20, or 30 years. A shorter term generally means higher monthly payments but less interest paid overall. Longer terms provide lower monthly payments but may result in paying more interest over time.

Amortization schedules outline how your monthly payments are applied to both principal and interest. Understanding how your payments are allocated can help you see how much equity you're building each month and when you'll reach your break-even point.

Retirement Planning: Navigating Ragnar's Golden Years

You may want to see also

![]()

Property Maintenance: Regular upkeep to preserve value

Maintaining your property is crucial for preserving its value and ensuring a steady return on your investment. Regular upkeep not only keeps your home in good condition but also helps prevent minor issues from becoming major, costly problems. Here are some key aspects of property maintenance to focus on:

- Routine Inspections: Schedule periodic inspections by professionals to assess the condition of your property. This includes checking for structural integrity, electrical systems, plumbing, roofing, and any potential signs of damage or wear. Regular inspections can identify issues early on, allowing for prompt repairs and preventing further deterioration. For instance, catching a small roof leak early can save you from extensive water damage and costly repairs.

- Preventive Maintenance: Implement a preventive maintenance schedule to address potential issues before they become significant problems. This includes regular cleaning, painting, and sealing to protect against weather damage. For example, pressure washing your exterior walls and trim can prevent mold growth and paint peeling. Additionally, maintaining the landscaping can enhance curb appeal and overall property value.

- Appliance and System Upkeep: Pay attention to the maintenance of essential systems and appliances. Regularly service heating and cooling systems to ensure efficient performance and longevity. Check and replace air filters, clean ducts, and consider annual professional inspections. Similarly, maintain kitchen and bathroom appliances by following manufacturer guidelines for cleaning, maintenance, and timely part replacements. Well-maintained appliances can significantly impact a property's appeal and value.

- Addressing Repairs Promptly: Be responsive to any maintenance requests or issues reported by tenants or homeowners. Promptly address repairs to maintain a positive living environment and preserve property value. Delayed repairs can lead to further damage, increased costs, and potential dissatisfaction among occupants. Keep a record of all maintenance activities and expenses to track the property's overall maintenance history.

- Stay Informed and Adapt: Stay updated with the latest maintenance practices and industry trends. Attend workshops or online courses to learn about new technologies and techniques in property maintenance. Adapting to modern methods and materials can improve the efficiency and effectiveness of your maintenance efforts. For instance, exploring energy-efficient upgrades can not only reduce utility costs but also make your property more attractive to environmentally conscious buyers or tenants.

Investments After Loss: A New Chapter

You may want to see also

![]()

Market Trends: Research local real estate market dynamics

To understand how a home can be a valuable investment, it's crucial to delve into the local real estate market dynamics. This involves a comprehensive analysis of various factors that influence the market's behavior and trends. Here's a breakdown of the key aspects to consider:

Market Research and Analysis: Begin by conducting thorough market research on your specific location. This includes studying historical data on property prices, sales trends, and market performance over different periods. Look for patterns and identify factors that have driven price fluctuations in the past. For instance, economic indicators like interest rates, employment rates, and local population growth can significantly impact the housing market. Analyze these factors to predict potential future trends.

Supply and Demand: Understanding the balance between the supply of available homes and the demand from buyers is essential. A market with limited supply and high demand often experiences upward pressure on prices. Research the number of new constructions, renovations, or developments in your area and compare it to the existing housing stock. Additionally, consider demographic changes, such as an influx of young families or an aging population, which can shift the demand dynamics.

Local Amenities and Infrastructure: The presence of desirable amenities and infrastructure plays a pivotal role in attracting buyers and investors. Evaluate the quality and accessibility of schools, healthcare facilities, transportation networks, and recreational areas. Proximity to employment hubs or thriving business districts can also make a property more attractive. These factors contribute to the long-term value and desirability of a home, making it a sound investment choice.

Economic and Social Factors: Macroeconomic conditions and social trends significantly impact the real estate market. Research local economic growth, employment rates, and industry diversity. A thriving local economy with low unemployment can stimulate housing demand. Moreover, consider social factors like migration patterns, cultural shifts, and the impact of remote work on housing preferences. These factors may influence the types of properties in demand and their price points.

Competitive Analysis: Study the competition in the market by examining nearby properties and their sales history. Identify the strengths and weaknesses of competing listings, and understand the pricing strategies employed by successful sellers. This analysis will help you determine the optimal price range for your investment property and identify any unique selling points that can set it apart.

By delving into these market trends and conducting thorough research, you can make informed decisions about investing in real estate. Understanding the local dynamics allows you to navigate the market with confidence, identifying opportunities for profitable investments while also considering the long-term potential of your home as an asset.

Purchasing Power: Navigating the Investment Trust Landscape

You may want to see also

![]()

Tax Implications: Explore tax benefits and deductions

When considering a home as an investment, understanding the tax implications is crucial for maximizing returns and ensuring compliance with tax laws. Here's an overview of the tax benefits and deductions associated with this strategy:

Capital Gains Tax: One of the primary tax advantages of owning a rental property is the potential for tax savings through capital gains. When you sell a property, you may be subject to capital gains tax on the profit made from the sale. However, certain deductions can reduce this tax burden. For instance, you can claim expenses related to the sale, such as legal fees, commissions, and closing costs. Additionally, if you've owned the property for at least two years, you may qualify for a reduced capital gains tax rate, which can significantly lower your tax liability.

Mortgage Interest Deduction: This is a significant tax benefit for homeowners. You can deduct the interest paid on your mortgage, which can result in substantial savings. The IRS allows you to deduct the interest on loans used to purchase or improve your primary residence and one additional home. This deduction can be particularly advantageous for long-term investors who hold properties for extended periods, as it provides a consistent tax benefit over time.

Rental Expenses: As a landlord, you can deduct various expenses related to your rental property. These include mortgage interest, property taxes, insurance, repairs, maintenance, and property management fees. These deductions can significantly reduce your taxable income, ultimately leading to lower tax payments. It's important to keep detailed records of these expenses to ensure you can claim them accurately when filing your taxes.

Depreciation: Depreciation is an essential concept in real estate investing. You can deduct a portion of the property's value as an expense each year, reflecting its decrease in value over time. This deduction is calculated using the Modified Accelerated Cost Recovery System (MACRS) and can be claimed for both residential and commercial properties. Depreciation allows investors to spread the cost of the property over multiple years, providing a consistent tax benefit and reducing their taxable income.

Tax Credits: In addition to deductions, there are also tax credits available for homeowners and investors. For example, the Residential Energy Efficient Property Credit allows you to claim a credit for expenses related to energy-efficient improvements, such as solar panels or insulation. Another credit is the Work Opportunity Tax Credit, which provides incentives for hiring individuals from targeted groups, including those in the rental property business.

Understanding these tax implications is essential for making informed decisions when investing in real estate. By strategically utilizing these tax benefits and deductions, investors can optimize their financial gains and minimize their tax obligations. It is recommended to consult with a tax professional or accountant to ensure compliance with tax laws and to take full advantage of the available deductions and credits.

The Amazon Effect: Transforming Your World, Your Wallet, and Your Future

You may want to see also

Frequently asked questions

Homeownership can be a powerful investment strategy. You can leverage the equity in your property to generate returns through various methods. One common approach is to rent out your home to tenants, providing a steady income stream. Additionally, you can consider flipping properties, where you buy, renovate, and sell a house for a profit. Another strategy is to use your home as collateral for a loan, allowing you to invest in other assets or ventures.

Investing in real estate via homeownership offers several advantages. Firstly, it provides a tangible asset, which can act as a hedge against inflation and market volatility. Over time, property values tend to appreciate, potentially increasing your net worth. Homeownership also offers tax benefits, such as deductions for mortgage interest and property taxes. Moreover, being a landlord allows you to build a long-term wealth-building strategy by generating rental income and accumulating equity.

While investing in real estate can be lucrative, it also carries certain risks. One significant challenge is the potential for property values to decrease, especially in a downturn. This could result in losses if you need to sell the property. Additionally, being a landlord comes with responsibilities, such as finding and managing tenants, handling maintenance issues, and ensuring compliance with rental regulations. It requires time, effort, and a certain level of expertise to navigate these challenges successfully.