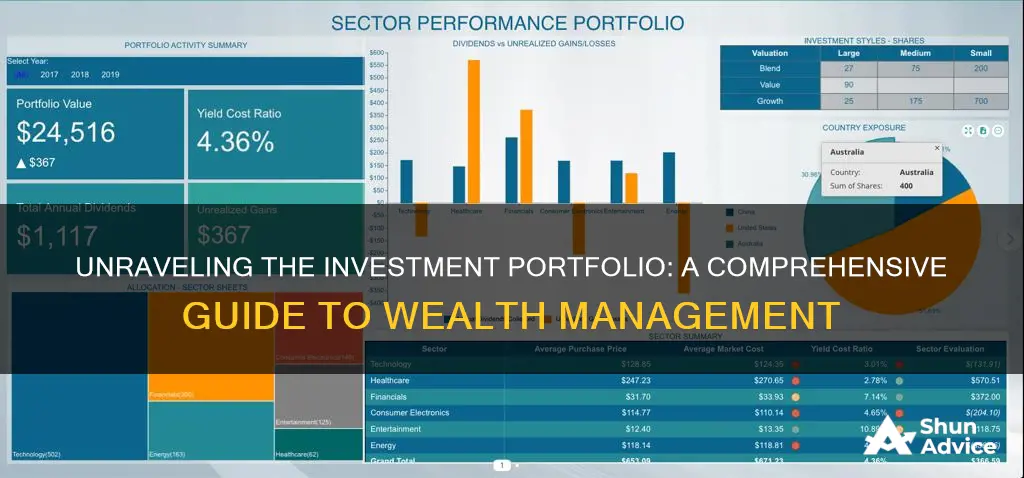

An investment portfolio is a powerful tool for individuals seeking to grow their wealth over time. It involves carefully selecting and combining various financial assets, such as stocks, bonds, real estate, and commodities, to create a diversified and balanced investment strategy. By allocating capital across different asset classes, investors can potentially reduce risk and increase the chances of achieving their financial goals. Understanding how an investment portfolio works is essential for anyone looking to navigate the complex world of investing and make informed decisions about their financial future.

What You'll Learn

- Asset Allocation: Diversifying investments across different asset classes

- Risk Management: Strategies to minimize potential losses

- Performance Measurement: Tracking returns and comparing against benchmarks

- Rebalancing: Adjusting portfolio to maintain desired risk level

- Tax Efficiency: Optimizing tax implications of investment decisions

![]()

Asset Allocation: Diversifying investments across different asset classes

Asset allocation is a fundamental concept in investment management, and it involves distributing your investment portfolio across various asset classes to achieve a balanced and diversified approach. The primary goal is to optimize risk and return by carefully selecting and combining different assets, such as stocks, bonds, cash, and alternative investments. Diversification is a key strategy here, as it aims to reduce the overall risk of the portfolio by not putting all your eggs in one basket.

When allocating assets, investors consider their financial goals, risk tolerance, and time horizon. For instance, a young investor with a long-term investment horizon might allocate a larger portion of their portfolio to stocks, which historically offer higher returns over extended periods. In contrast, a more conservative investor with a shorter time frame might prefer a higher allocation to bonds and fixed-income securities, which are generally less volatile. The idea is to create a portfolio that aligns with the investor's risk profile and objectives.

Asset allocation can be done in various ways. One common method is to use a target allocation strategy, where an investor sets a specific percentage or weight for each asset class. For example, a 60/40 portfolio might allocate 60% of the funds to stocks and 40% to bonds. This approach provides a clear framework for diversification. Another strategy is to use a risk-based allocation, where investments are chosen based on their historical correlation with the overall market. This method aims to create a portfolio that moves in tandem with the market but with reduced volatility.

Diversification across different asset classes is essential because it helps manage risk. Different asset classes have varying levels of risk and return potential. For instance, stocks are generally more volatile and offer higher returns over the long term, while bonds are considered less risky but provide lower returns. By allocating investments across these classes, investors can smooth out the impact of market fluctuations. If one asset class underperforms, others may perform well, thus reducing the overall risk of the portfolio.

In summary, asset allocation is a critical process in investment portfolio management, allowing investors to build a diversified and well-balanced investment strategy. It involves a careful selection of asset classes, taking into account individual risk tolerance and financial goals. Effective asset allocation can lead to improved risk-adjusted returns and provide investors with a sense of security, knowing that their portfolio is not overly exposed to any single market or asset type.

Retirement Investing: Understanding the True Cost of Fees

You may want to see also

![]()

Risk Management: Strategies to minimize potential losses

Understanding and managing risk is a critical aspect of investment portfolio management. Here are some strategies to minimize potential losses and protect your investments:

Diversification: One of the most fundamental principles of risk management is diversification. This involves spreading your investments across various asset classes, sectors, and geographic regions. By diversifying, you reduce the impact of any single investment's performance on your overall portfolio. For example, if you invest in a mix of stocks, bonds, real estate, and commodities, a decline in the stock market might be offset by gains in other asset classes. Diversification helps to smooth out the volatility of your portfolio, making it less susceptible to significant losses.

Asset Allocation: This strategy involves dividing your portfolio into different asset classes based on your risk tolerance, investment goals, and time horizon. A common approach is to allocate a portion of your portfolio to more aggressive investments like stocks, which offer higher potential returns but come with greater risk, and a larger portion to more conservative investments like bonds or cash equivalents, which provide stability and lower risk. Regularly reviewing and rebalancing your asset allocation ensures that your portfolio remains aligned with your investment strategy and risk profile.

Risk Assessment and Monitoring: Conducting a thorough risk assessment of your investments is essential. This includes identifying potential risks such as market risk, credit risk, liquidity risk, and operational risk. You can use various tools and metrics to quantify these risks, such as volatility measures, credit ratings, and liquidity assessments. Regularly monitoring these risks allows you to make informed decisions and take proactive measures to mitigate potential losses. For instance, if a particular stock is showing signs of financial distress, you might consider reducing your position or selling it altogether.

Stop-Loss Orders and Limits: Implementing stop-loss orders can be an effective way to limit potential losses. A stop-loss order is an instruction to sell an asset when it reaches a certain price. This strategy helps to lock in losses and prevent them from escalating. You can set a stop-loss price based on your risk tolerance and the potential downside risk of an investment. Additionally, using price limits can ensure that you don't purchase an asset at an unfavorable price, thus minimizing the risk of immediate losses.

Regular Review and Rebalancing: Investment portfolios should be regularly reviewed and rebalanced to maintain the desired risk exposure. Market conditions and individual investment performance can shift over time, impacting your portfolio's overall risk profile. By periodically assessing your investments, you can identify any deviations from your initial strategy and make necessary adjustments. Rebalancing involves buying or selling assets to restore the original asset allocation, ensuring that your portfolio remains diversified and aligned with your risk tolerance.

Homes: The Ultimate Investment?

You may want to see also

![]()

Performance Measurement: Tracking returns and comparing against benchmarks

Performance measurement is a critical aspect of managing an investment portfolio, as it provides a quantitative way to assess the success of investment strategies and compare them against relevant benchmarks. The primary goal is to evaluate the actual returns generated by the portfolio and determine how they stack up against a predefined standard or reference point. This process is essential for investors and fund managers to gauge the effectiveness of their investment decisions and make informed adjustments.

When measuring performance, the first step is to calculate the total return of the investment portfolio. This includes both the capital gains (or losses) from selling investments and the income generated from dividends, interest, or other sources. Total return is a comprehensive metric that reflects the overall growth or decline in the value of the portfolio over a specific period. It is calculated by adding the sum of capital gains and the total income received during the investment period.

After determining the total return, the next step is to compare it against a benchmark, which serves as a reference point for performance evaluation. A benchmark is typically a well-known investment index or a carefully selected group of securities that represents a specific market segment or investment style. For example, the S&P 500 index is a common benchmark for large-cap U.S. stocks, while the Barclays Capital Aggregate Bond Index is often used for fixed-income investments. By comparing the portfolio's returns to the benchmark, investors can assess whether their portfolio has outperformed or underperformed the market or a specific segment of it.

There are several ways to compare portfolio returns to benchmarks. One common method is to calculate the excess return, which is the difference between the portfolio's return and the benchmark's return. Excess return provides insight into the portfolio's performance relative to the chosen benchmark. If the excess return is positive, it indicates that the portfolio has outperformed the benchmark, while a negative excess return suggests underperformance. This analysis helps investors understand the value added by their investment decisions.

Additionally, performance measurement involves tracking and analyzing various other metrics, such as risk-adjusted returns (e.g., Sharpe ratio), maximum drawdown, and cumulative returns over different time periods. These metrics provide a more comprehensive understanding of the portfolio's performance and risk characteristics. For instance, the Sharpe ratio measures the excess return per unit of volatility, offering insight into the risk-adjusted performance of the investment.

In summary, performance measurement is a vital process in portfolio management, enabling investors to assess the effectiveness of their investment strategies. By calculating total returns and comparing them against carefully selected benchmarks, investors can make data-driven decisions to optimize their portfolios. This process also involves monitoring various performance metrics to gain a holistic view of the portfolio's success and risk exposure.

SPACs: The New Investment Craze

You may want to see also

![]()

Rebalancing: Adjusting portfolio to maintain desired risk level

Rebalancing is a crucial strategy in managing an investment portfolio, especially when aiming to maintain a desired risk level. It involves periodically reviewing and adjusting the allocation of assets within the portfolio to ensure it aligns with the investor's risk tolerance and financial goals. This process is essential as markets fluctuate, and asset prices can change over time, potentially impacting the overall risk exposure of the portfolio.

The primary goal of rebalancing is to restore the original asset allocation, often referred to as the 'target allocation'. This target allocation is determined by the investor's risk profile, which considers their investment horizon, financial goals, and ability to withstand market volatility. For instance, a conservative investor might aim for a higher percentage of fixed-income securities to minimize risk, while a more aggressive investor may opt for a larger portion of equity investments.

Over time, market movements can cause the actual asset allocation to deviate from the target allocation. For example, if the stock market experiences a significant surge, the proportion of equity investments in the portfolio may increase, potentially increasing the overall risk. Conversely, if the bond market performs well, the allocation to fixed-income securities might decrease. To address this, investors should regularly assess their portfolios and make necessary adjustments.

Rebalancing can be done in several ways. One common approach is to buy or sell assets to return the portfolio to its target allocation. For instance, if the stock portion of the portfolio has grown disproportionately large, investors might sell some stocks and buy additional bonds or other asset classes to rebalance. This process ensures that the portfolio remains diversified and that the risk is distributed across various asset classes according to the investor's preferences.

It's important to note that rebalancing should be a disciplined and regular practice. Market volatility is inevitable, and without rebalancing, the portfolio's risk exposure may become too high or too low, potentially leading to suboptimal performance. By regularly reviewing and rebalancing the portfolio, investors can stay on track to meet their financial objectives while managing risk effectively. This proactive approach allows investors to benefit from market movements while minimizing the impact of potential downturns.

Alpha Investments MTG: Navigating the Purchase Process

You may want to see also

![]()

Tax Efficiency: Optimizing tax implications of investment decisions

Understanding the tax implications of your investment decisions is crucial for building a tax-efficient portfolio. Here's a breakdown of how to optimize your tax strategy:

Tax-Advantaged Accounts:

- Retirement Accounts: Contributions to traditional 401(k)s and IRAs are often tax-deductible, reducing your taxable income for the year. Investments within these accounts grow tax-free until withdrawal, typically in retirement when you're in a lower tax bracket.

- Health Savings Accounts (HSAs): Contributions to HSAs are tax-deductible, and qualified medical expenses can be paid with tax-free funds. This triple tax advantage (tax-deductible contribution, tax-free growth, tax-free withdrawal for qualified expenses) makes HSAs a powerful tool for saving for healthcare costs.

Tax-Efficient Investing:

- Capital Gains: When you sell investments that have appreciated in value, you incur a capital gain. Long-term capital gains (held for over a year) are generally taxed at a lower rate than ordinary income. Strategically holding investments for the long term can minimize these taxes.

- Dividends: Dividends are typically taxed as ordinary income. However, some dividend-paying stocks qualify for qualified dividend treatment, which is taxed at a lower rate.

- Tax-Loss Harvesting: This strategy involves selling investments that have declined in value to offset capital gains. By realizing losses, you can use them to reduce taxable income in the current year.

Asset Location:

- Tax-Sensitive Investments in Tax-Advantaged Accounts: Place investments with higher tax consequences (like bonds or dividend-paying stocks) in tax-advantaged accounts like 401(k)s or IRAs. This maximizes the tax benefits of these accounts.

- Tax-Efficient Investments in Taxable Accounts: If you have a taxable investment account, consider holding investments with lower tax implications (like index funds or ETFs) to minimize potential taxes.

Regular Review and Rebalancing:

- Tax-Loss Carryforwards: Monitor your portfolio for losses that can be used to offset future capital gains. These losses can be carried forward indefinitely, providing tax relief in future years.

- Rebalancing: Periodically review and rebalance your portfolio to maintain your desired asset allocation. This can help ensure that your investments are aligned with your risk tolerance and tax goals.

Remember: Tax laws are complex and constantly evolving. Consult a qualified financial advisor or tax professional to tailor a tax-efficient strategy that aligns with your individual circumstances and investment goals.

Investing: A New National Pastime?

You may want to see also

Frequently asked questions

An investment portfolio is a collection of financial assets, such as stocks, bonds, cash, and other securities, that an individual or institution owns. It is a way to diversify one's investments and manage risk by holding a variety of assets.

Diversification is a key strategy to reduce risk. By investing in different asset classes, sectors, and geographic regions, you can minimize the impact of any single investment's performance on your overall portfolio. This way, if one investment underperforms, others may compensate, leading to a more stable and potentially higher return over time.

Asset allocation refers to the process of dividing your portfolio among various asset classes. This could include stocks, bonds, real estate, commodities, and cash equivalents. The goal is to determine the appropriate mix based on your investment goals, risk tolerance, and time horizon. A well-allocated portfolio can help balance risk and return, ensuring your investments align with your financial objectives.

Regular portfolio reviews are essential to ensure it stays on track. It is recommended to review your portfolio at least annually or whenever there are significant changes in your financial situation or investment goals. Rebalancing involves buying or selling assets to return the portfolio to its original target allocation. This process helps maintain the desired risk level and investment strategy.

A financial advisor can provide valuable expertise and guidance in managing your investment portfolio. They can help assess your financial goals, risk tolerance, and time horizon to create a customized investment plan. Advisors can also offer research, market insights, and regular portfolio reviews, ensuring your investments are well-diversified and aligned with your objectives. Additionally, they can provide tax-efficient strategies and help navigate complex financial decisions.