The Annual Investment Allowance (AIA) is a valuable tax relief for businesses in the UK, allowing them to claim a deduction for certain capital expenditures. This allowance enables companies to write off the full cost of qualifying assets in the year of purchase, providing a significant boost to cash flow and reducing the overall tax burden. Understanding how the AIA works is essential for business owners and investors, as it can help optimize financial planning and decision-making. This paragraph will delve into the specifics of the AIA, its benefits, and how it can be effectively utilized to maximize tax efficiency.

What You'll Learn

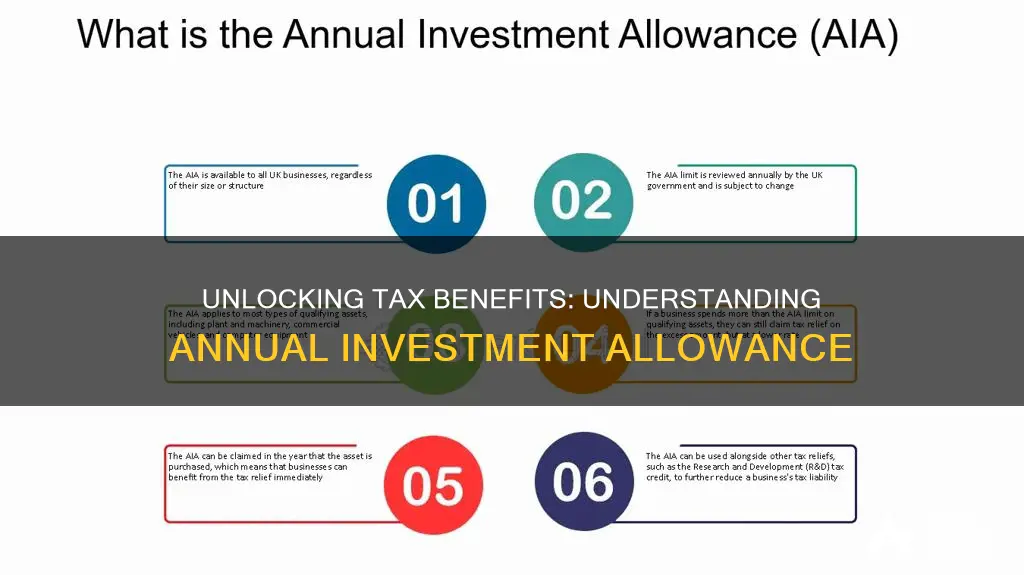

- Annual Investment Allowance: A tax relief for new plant, machinery, and vehicles

- Claiming Allowance: Businesses can claim up to 100% of investment costs

- Annual Limit: The allowance has a £1 million annual limit

- Carry-Forward: Unused allowance can be carried forward for up to 5 years

- Tax Benefits: It reduces taxable profits and provides cash flow benefits

![]()

Annual Investment Allowance: A tax relief for new plant, machinery, and vehicles

The Annual Investment Allowance (AIA) is a valuable tax relief mechanism designed to encourage businesses to invest in new plant, machinery, and vehicles. It provides a significant benefit to companies by allowing them to claim a higher deduction for their capital expenditures, effectively reducing their taxable profits. This allowance is particularly beneficial for businesses looking to expand their operations, upgrade equipment, or acquire new assets.

Under the AIA, companies can claim an allowance on the full value of most new plant and machinery purchases made during the tax year. This means that when a business invests in new assets, it can immediately deduct the entire cost from its profits, resulting in a substantial tax saving. The allowance is set at a specific percentage or amount, which varies over time, and it applies to a wide range of qualifying assets. For instance, in recent years, the AIA has been set at 100% of the investment, allowing businesses to claim the full value of their purchases as a deduction.

To be eligible for the AIA, the plant and machinery must be new and acquired for use in the business. This includes a variety of assets such as computers, office furniture, vehicles, and specialized equipment. It's important to note that second-hand or used assets do not qualify, and the allowance is only available for the year of acquisition. Once the asset is acquired and put into use, the business can claim the AIA for that specific year.

The AIA provides a powerful incentive for businesses to invest in their future. By allowing immediate tax relief on capital expenditures, companies can free up cash flow and potentially reinvest those savings into further growth. This mechanism encourages businesses to make strategic investments, driving economic growth and development. It also promotes a cycle of continuous improvement, as businesses are motivated to regularly update their equipment and infrastructure to remain competitive.

Understanding the Annual Investment Allowance is crucial for business owners and financial planners. It enables them to make informed decisions about capital investments and optimize their tax strategies. By taking advantage of this allowance, businesses can enhance their financial performance and contribute to the overall economic health of the country.

ExxonMobil's Infrastructure Overhaul: A $10 Billion Makeover

You may want to see also

![]()

Claiming Allowance: Businesses can claim up to 100% of investment costs

The Annual Investment Allowance (AIA) is a valuable tax relief mechanism designed to encourage businesses to invest in tangible assets and equipment. It allows companies to claim a deduction for a significant portion of their investment costs, providing a substantial financial boost. Under the AIA, businesses can claim up to 100% of their investment costs as an expense, which directly reduces their taxable profits. This means that the entire investment amount can be written off in the year it is incurred, offering a powerful incentive for companies to make capital expenditures.

To claim the AIA, businesses must ensure they meet certain criteria. Firstly, the investment must be made in tangible assets, such as machinery, plant, and equipment, which are used in the production or supply of goods or services. This includes items like computers, vehicles, and manufacturing machinery. Secondly, the investment must be made in the UK and must be new or unused when the allowance is claimed. It's important to note that the AIA applies to both small and large businesses, providing a level playing field for all companies regardless of size.

When claiming the allowance, businesses need to keep detailed records of their investments. This includes evidence of the purchase, such as invoices and delivery notes, as well as any associated costs, such as installation or setup fees. The AIA can be claimed in the year the investment is made, and it is calculated as a percentage of the total investment cost. For the current tax year, the AIA rate is 100%, meaning that up to 100% of the investment can be claimed as an expense.

It is worth mentioning that there are some limitations and changes to the AIA that businesses should be aware of. The allowance is typically limited to a maximum investment amount, which is indexed to inflation. For the current tax year, this limit is set at £1,000,000. However, there have been recent changes to the AIA, including a temporary increase during the pandemic, which allowed for a higher allowance. Businesses should stay updated with the latest legislation to ensure they claim the correct amount.

In summary, the Annual Investment Allowance provides a significant opportunity for businesses to maximize their tax efficiency by claiming a substantial portion of their investment costs. By understanding the criteria and keeping proper records, companies can take full advantage of this allowance, which can lead to improved cash flow and overall financial health. Staying informed about any changes to the AIA is essential to ensure compliance and optimize tax planning strategies.

Investment Firms: Your Retirement's Best Friend

You may want to see also

![]()

Annual Limit: The allowance has a £1 million annual limit

The Annual Investment Allowance (AIA) is a valuable tax relief for businesses in the UK, designed to encourage investment in plant and machinery. One of the key aspects of the AIA is the annual limit, which is set at £1 million. This limit is crucial as it determines the maximum amount of investment that can be claimed as a deduction against profits in a given tax year.

When it comes to the £1 million annual limit, it's important to understand that this is a fixed amount that applies to all businesses, regardless of their size or industry. This means that if a business invests more than £1 million in plant and machinery in a single tax year, they can only claim the full £1 million as a deduction. Any excess investment above this limit will not be eligible for the AIA and will need to be carried forward to future years.

To maximize the benefit of the AIA, businesses should carefully plan their investment strategy around this annual limit. This involves making strategic decisions about when and how much to invest in order to ensure that the £1 million limit is utilized effectively. For example, a business might choose to invest a significant amount in the first quarter of the tax year to take full advantage of the AIA in that year.

It's worth noting that the £1 million limit is a generous provision, allowing businesses to deduct a substantial portion of their investment costs. This can result in a significant reduction in taxable profits, leading to lower tax liabilities and increased cash flow. However, businesses should also be mindful of the potential impact of the limit on their cash flow, especially if they are planning large investments that exceed the annual threshold.

In summary, the £1 million annual limit of the AIA is a critical consideration for businesses when planning their investment strategy. Understanding this limit and how it applies to their specific circumstances can help businesses make informed decisions to optimize their tax position and financial performance.

The Debt-Investment Dilemma: Navigating the Path to Financial Freedom

You may want to see also

![]()

Carry-Forward: Unused allowance can be carried forward for up to 5 years

The Annual Investment Allowance (AIA) is a valuable tax relief for businesses, allowing them to claim a deduction for certain capital expenditures. One of its key features is the ability to carry forward unused allowance, providing a significant benefit for businesses that may not have enough qualifying investments in a given year.

When a business makes qualifying capital expenditures, it can claim the AIA against its profits, reducing its taxable income. If the AIA claim exceeds the business's profits, the excess can be carried forward. This carry-forward mechanism allows businesses to utilize the allowance in subsequent years, providing a valuable tool for long-term financial planning.

The carry-forward period for unused AIA is typically limited to five years. This means that any unused allowance from a particular year can be carried forward and utilized in the following five years. For example, if a business has an unused AIA of £100,000 in 2022, it can claim this amount in 2023, 2024, 2025, 2026, or 2027, depending on the business's investment patterns and financial situation.

This carry-forward provision is particularly useful for businesses with cyclical investment patterns or those experiencing fluctuations in profits. It allows them to smooth out their tax liabilities over time, ensuring that they can take advantage of the AIA when it is most beneficial. By carrying forward the unused allowance, businesses can better manage their cash flow and financial planning, especially during periods of lower investment or profitability.

Understanding the carry-forward mechanism is essential for businesses to maximize the benefits of the Annual Investment Allowance. It enables them to strategically plan their investments and tax affairs, ensuring that they make the most of this valuable tax relief.

Unraveling the Mystery: How Investing Works in HUD

You may want to see also

![]()

Tax Benefits: It reduces taxable profits and provides cash flow benefits

The Annual Investment Allowance (AIA) is a valuable tax relief mechanism designed to encourage businesses to invest in tangible assets and plant. One of its primary benefits is the significant reduction in taxable profits, which can lead to substantial tax savings for businesses. When a business claims the AIA, it directly reduces the taxable profit for the year, resulting in a lower tax liability. This is particularly advantageous for small and medium-sized enterprises (SMEs) that often have limited profits, as the AIA can effectively increase their profit margins. By reducing taxable profits, businesses can retain more of their earnings, which can then be reinvested into the business or distributed to shareholders as dividends.

The AIA's impact on cash flow is another critical aspect. By allowing businesses to claim a higher deduction for investment spending, it provides an immediate cash flow boost. This is especially beneficial for companies looking to expand their operations, purchase new equipment, or invest in property. The cash flow benefit is twofold; firstly, it enables businesses to make these investments without a significant immediate impact on their cash reserves, and secondly, it allows for better financial planning and management, as the reduced tax liability provides more financial flexibility.

To illustrate, consider a small manufacturing business that decides to invest in new machinery. If the total cost of the machinery is £100,000, and the business qualifies for the AIA, they can claim a deduction of up to £100,000 for that year. This means their taxable profit is reduced by £100,000, resulting in a lower tax bill. Additionally, the business now has the full £100,000 available for other operational expenses or future investments, improving their overall cash flow.

It's important to note that the AIA's impact on taxable profits and cash flow can vary depending on the business's specific circumstances and the level of investment made. Businesses should carefully plan their investments and ensure they meet the AIA's eligibility criteria to maximize these tax benefits. Proper utilization of the AIA can lead to improved financial performance and long-term sustainability for businesses.

Investors: Money Masters or Risk-Takers?

You may want to see also

Frequently asked questions

The Annual Investment Allowance is a tax relief mechanism in the UK that allows businesses to claim a deduction for certain capital expenditures made during the tax year. It provides a significant benefit for companies investing in plant, machinery, and other qualifying assets.

The AIA enables businesses to claim 100% tax relief on investments up to a specified limit, which is currently set at £1 million for the 2023/24 tax year. This means that if a business invests in eligible assets, they can reduce their taxable profits by the full amount of the investment in the same year, providing an immediate tax saving.

Yes, there are certain conditions and limitations. Firstly, the AIA is only available to businesses in the UK. Secondly, the allowance is limited to investments in tangible assets like buildings, plant, and machinery, and it does not cover intangible assets or second-hand purchases. Additionally, the AIA is a temporary measure, and its value and eligibility criteria may change over time, so it's essential to stay updated with the latest tax regulations.