Mortgage securitization is a complex process that involves turning a group of income-producing assets into a single security tradable on financial markets. It is beneficial to investors, lenders, and the economy, as it increases access to credit. In the case of mortgage-backed securities (MBS), investors buy a share in a pool of mortgages and receive regular cash flows from the underlying mortgages as homeowners make their monthly payments. This process has advantages for borrowers as it makes loans more available and stimulates the market. However, it is not without its downsides, including the risk of prepayment, where borrowers may refinance or pay off their mortgages earlier than expected, altering the cash flow for investors.

| Characteristics | Values |

|---|---|

| Increased liquidity | Commercial real estate borrowers benefit from increased liquidity |

| More available loans | Securitization stimulates the market and makes loans more available |

| Reduced risk | Ginnie Mae, for example, guarantees the timely payment of mortgages' principal and interest, thereby reducing the risks for MBS investors |

| Regular cash flow | Investors benefit from regular cash flows from the underlying mortgages |

| Capital appreciation | If interest rates fall, investors benefit from the potential for capital appreciation |

| Prepayment risk | Investors face the risk that homeowners may refinance or pay off their mortgages earlier than expected |

| Default risk | The risk that homeowners will default on the mortgages that back the MBS |

What You'll Learn

![]()

Increased liquidity

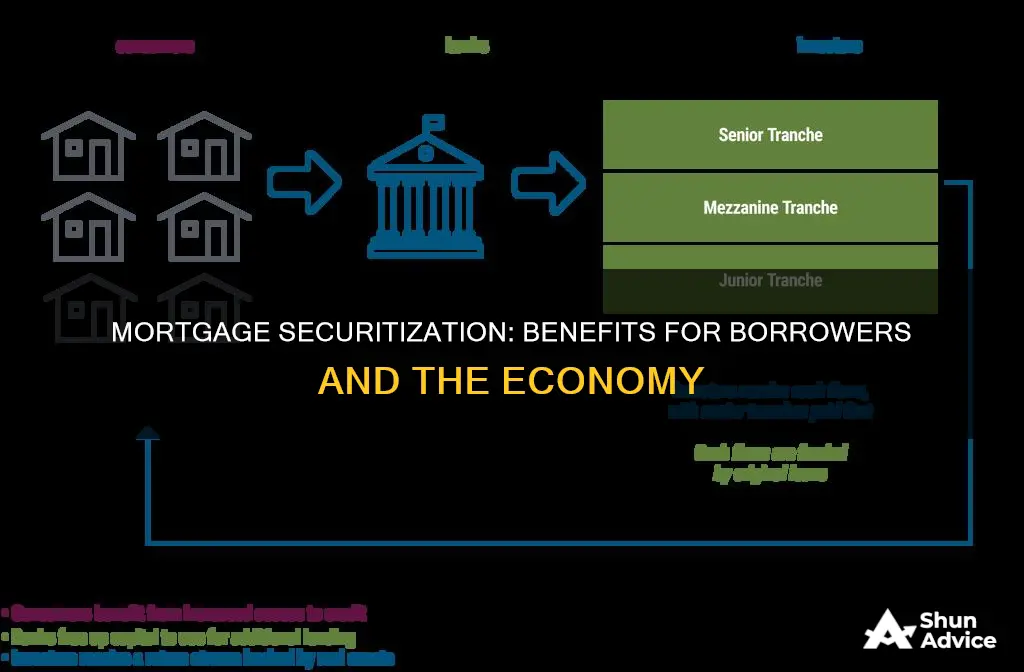

Securitization is a complex process that involves turning a group of income-producing assets into a single security that can be traded on financial markets. This process increases liquidity in the market by making loans more available to borrowers.

Mortgage debt is the most commonly securitized asset, with mortgage-backed securities (MBS) being a common securitized product. In the securitization process, a company that owns debt, such as a commercial or multifamily real estate lender, will place the debt into a special purpose entity (SPE) or special purpose vehicle (SPV). The SPV is a separate legal entity designed to be bankruptcy-remote, meaning that its assets will not be affected if the lender goes bankrupt. The SPV then issues securities, known as pass-through certificates, which represent an interest in the pool of assets.

By securitizing mortgages, the originator can remove these assets from its balance sheets and free up capital for additional loans. This increased liquidity benefits borrowers by making more funds available for lending and stimulating the market. Securitization also reduces the risk for lenders, as they are no longer solely responsible for the loans they originate. Instead, the risk is distributed to investors who purchase the securities.

Additionally, securitization can lead to greater access to credit for borrowers. With more funds available, lenders may be more willing to offer loans to a wider range of borrowers, including those who may not have qualified for a traditional mortgage. Securitization also allows lenders to offer more competitive interest rates, as they can offset costs by selling the securities to investors.

Mortgages: Empowering Buyers to Achieve Homeownership Dreams

You may want to see also

![]()

More available loans

Securitization is a complex process that involves multiple steps. It begins with a lender, such as an investment bank, issuing loans to borrowers. These loans can be mortgages, auto loans, credit card receivables, or other types of credit. The lender then selects a pool of loans with similar characteristics, such as loan type, maturity, and credit quality. This pool of loans serves as collateral for issuing securities.

Mortgage debt is the most commonly securitized asset. By securitizing mortgages, lenders can make loans more available to borrowers. This is because securitization allows lenders to remove assets from their balance sheets, freeing up capital for additional loans. This process stimulates the market and increases liquidity for borrowers.

For example, a bank might securitize a group of mortgages by selling them to a special purpose vehicle (SPV), which is a separate legal entity designed to be bankruptcy-remote. The SPV then creates tradable securities backed by the mortgages and sells them to investors. The investors now effectively own a share of the mortgage pool and receive regular cash flows from the borrowers' monthly payments.

Through securitization, lenders can free up capital and provide more loans to borrowers. This process can help to stimulate the market and increase the availability of loans for borrowers seeking to purchase real estate or other assets. However, it is important to note that securitization also has potential downsides, such as the risk of early loan repayment by borrowers, which can impact the expected cash flows for investors.

Jared Vennett's Guide to Modern Mortgages Explained

You may want to see also

![]()

Reduced risk

Securitization is the financial practice of pooling various types of contractual debt, such as residential mortgages, and selling their related cash flows to investors as securities. This process can benefit borrowers by reducing risk in several ways. Firstly, it isolates credit risk from the parent entity, meaning that the securitized assets are separate from the assets of the originating entity. This isolation can lead to a higher credit rating for the securitization than the "parent" company, as the underlying risks are different. For example, a small bank may be considered riskier than the mortgage loans it provides to its customers. Securitization also reduces the liability on the originator's balance sheet, allowing them to underwrite further loans and provide greater access to credit for borrowers.

Another way in which securitization reduces risk is by creating a self-funded asset book for banks and finance companies. Securitization allows these institutions to lower their capital requirements by removing assets from their balance sheets while maintaining the "earning power" of the assets. This can result in reduced funding costs, as a company with a lower credit rating can borrow at a higher rating through securitization.

The pooling of debt in securitization also helps to mitigate credit risk. By grouping together various types of debt, the overall risk is spread across a larger base, reducing the impact of individual borrower defaults. This diversification of risk is beneficial to both lenders and investors.

Additionally, securitization can reduce the risk of profit uncertainty. Once a block of business has been securitized, the level of profits is locked in, and the risk of profits not materializing is transferred away from the company. Securitization also provides more flexibility in allocating principal and interest to different classes of issued securities, allowing for the tailoring of maturity, risk, and return profiles to meet investor needs.

Finally, securitization can reduce the risk of technical defaults, which occur when a borrower violates the terms of their loan, such as by signing a lease with a tenant not approved by the loan servicer. While securitized loans can still lead to technical defaults, the risk has been mitigated through tighter underwriting standards and new regulations, such as risk retention rules.

Gifts, Mortgages, and Parental Money: Impact and Insights

You may want to see also

![]()

Regular cash flows

Mortgage securitization is the process of pooling together various types of contractual debt, such as residential mortgages, and selling the cash flows from these debts to investors as securities. These securities are known as mortgage-backed securities (MBS). As borrowers make payments on their mortgages, the cash flows are collected by a servicer and distributed to the MBS investors according to the terms of the securities.

The regular cash flows benefit investors in MBS as they receive a consistent income stream from the underlying mortgages. This income stream is generated by the monthly mortgage payments made by homeowners, which include both principal and interest payments. The cash flows are distributed to the MBS investors on a pro-rata basis, meaning that each investor receives a portion of the total cash flow collected.

The pooling of mortgages into MBS also helps to reduce the risk of default for investors. When a loan defaults within a portfolio of loan claims, the loss is first absorbed by the subordinated tranches, with the upper-level tranches remaining unaffected until the losses exceed the entire amount of the subordinated tranches. This structure helps to protect the senior tranches of investors from bearing the full brunt of any losses.

Additionally, mortgage securitization can help to reduce funding costs for borrowers. Through securitization, a company with a lower credit rating but a strong cash flow may be able to borrow at higher credit ratings rates. This is because the securities issued are backed by the underlying pool of assets, which provides a level of security and lowers the risk for investors.

Overall, the regular cash flows and reduced risk associated with mortgage securitization can make it an attractive investment opportunity, providing consistent returns for investors while also helping to reduce funding costs for borrowers.

Mortgage-Backed Securities: Boosting Economy Through Homeownership

You may want to see also

![]()

Potential for capital appreciation

Securitization is a complex process that involves several steps. It begins with a lender, such as an investment bank, issuing loans to borrowers. These loans can be in the form of mortgages, business lines of credit, auto loans, credit card receivables, or other types of credit.

The lender then selects a pool of loans with similar characteristics, such as loan type, maturity, and credit quality. This pool of loans serves as collateral for issuing securities. The next step is to create a separate legal entity called a Special Purpose Vehicle (SPV) or a special purpose entity. The SPV is designed to be bankruptcy-remote, meaning that if the lender goes bankrupt, the assets held by the SPV will not be affected.

The lender then sells the pool of loans to the SPV, removing them from its balance sheet. The SPV issues securities, known as pass-through or flow-through certificates, which represent an undivided interest in the pool of assets. As borrowers make payments on their loans, the cash flows are collected and distributed to investors pro-rata.

Mortgage-backed securities (MBS) are a common form of securitized product, backed by home loans issued to consumers. When an investor purchases MBS, they are buying a share in a pool of mortgages. As homeowners make their monthly mortgage payments, the cash is collected and distributed to MBS investors pro-rata.

Investors in MBS benefit from regular cash flows from the underlying mortgages, as well as the potential for capital appreciation. If interest rates fall, the value of fixed-income securities tends to rise. This means that investors can profit from both the principal and interest payments made on the underlying loans by the borrowers.

However, investing in MBS also comes with risks. One such risk is prepayment risk, where homeowners may refinance or pay off their mortgages earlier than expected, altering the cash flow profile of the MBS. By investing in MBS, investors are exposed to the risks and returns associated with the underlying mortgages.

Understanding Mortgage Escrow: Accounts, Payments, and Zero Balance

You may want to see also

Frequently asked questions

Mortgage securitization involves taking a group of income-producing assets and turning them into a single security that can be traded on financial markets. Mortgage debt is the most commonly securitized asset.

Securitization can make loans more available for borrowers, stimulating the market. It can also result in regular cash flows and potential capital appreciation.

There is a risk that CMBS loans are serviced by a separate company, known as a master servicer, which holds a fiduciary duty to the investors, not the borrower. This can lead to challenges if the loan goes into default. There is also a higher risk of technical defaults due to the strict rules arising from the securitization process.

Ginnie Mae facilitates the securitization of home mortgages backed by federally insured or guaranteed loans. Ginnie Mae guarantees the timely payment of mortgages' principal and interest, reducing the risk for MBS investors.

One potential downside is that borrowers may have to deal with a separate company, known as a master servicer, if their loan goes into default. Additionally, there may be a higher risk of technical defaults due to the strict rules that come with the securitization process.