Getting a mortgage preapproval is an important step in the home-buying process. It is a more thorough evaluation of your finances than pre-qualification and involves a hard credit check. A preapproval letter from a lender indicates that they are tentatively willing to lend money to you, up to a certain amount. This letter is valid for a certain period, typically 30 to 90 days, and helps you shop for a home within your budget. It also lets the seller know that you are a serious buyer who is likely to be able to secure financing. While a preapproval does not guarantee final approval of your mortgage, it gets a large chunk of the approval process out of the way, making it easier to make quick offers on homes.

| Characteristics | Values |

|---|---|

| Purpose | To determine how much money you can borrow to buy a home |

| Benefits | Provides a clear idea of how much home you can afford; shows sellers that you are a serious buyer; gives you a competitive edge over other buyers |

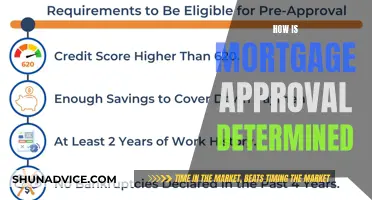

| Requirements | Filling out a mortgage application; providing proof of income, employment, assets, and credit score; demonstrating good credit through a hard credit pull |

| Process | Lenders look at your financial information, including income, assets, debts, and credit record; lenders may also require tax returns and other paperwork |

| Timeframe | Preapproval letters are typically valid for 30 to 90 days, but can also be valid for 60 days or as little as 30 days |

| Impact on Credit Score | May lower your credit score in the short term due to the hard credit inquiry |

| Differences from Pre-qualification | Preapproval is a more thorough evaluation of your finances and involves a more rigorous process than pre-qualification |

What You'll Learn

![]()

Pre-approval vs pre-qualification

Prequalification and preapproval are both types of mortgage approvals that refer to steps that lenders take to verify that a client can afford a mortgage. However, they have distinct meanings and purposes.

Prequalification

Prequalification is an early step in the homebuying journey. It is a preliminary evaluation of how much money you can borrow to buy a home. It is based on data you submit, such as your income, assets, and expected down payment. Lenders will use this information to provide a preliminary estimate of the mortgage size you could qualify for. Prequalification can be completed quickly, often online, and you may get results within an hour. It is a less involved step, with fewer verification steps. It is useful for first-time homebuyers who are establishing their homebuying budget and want an idea of how much they might be able to borrow. It is also helpful for narrowing down lenders.

Preapproval

Preapproval is a more thorough evaluation of your finances and creditworthiness. It is a more specific estimate of how much you could borrow from a lender. It requires more documentation, such as pay stubs, W-2 statements, and signed tax documents from previous years. Lenders will use this information to determine what loans you could be approved for, how much you can borrow, and what your interest rate might be. The preapproval process typically takes longer than prequalification and can take up to 10 business days to complete. A preapproval letter indicates that the lender has taken the time to look into your financial profile and considers you a serious buyer. It can give you a competitive edge in a competitive market and increase your chances of having your offer selected.

While the terms pre-qualification and pre-approval are sometimes used interchangeably, they are not the same thing. Preapproval provides a more accurate estimate of how much you can borrow and requires more financial information and verification. It also carries more weight with sellers and can increase your chances of having your offer accepted. On the other hand, prequalification is a quicker and easier process that provides a rough estimate of how much you can borrow. It requires less financial information and may be useful for homebuyers who are still in the early stages of the homebuying process and want to get an idea of their budget.

Mortgage Borrowing: When Is It Too Much?

You may want to see also

![]()

The role of credit score

A good credit score is essential to securing a mortgage preapproval. Lenders will conduct a hard credit inquiry to evaluate your creditworthiness. This involves requesting a copy of your credit report from one of the three major credit bureaus, and it can result in a small, temporary drop in your credit score.

The credit inquiry, or hard pull, is a significant factor in the preapproval process, as it provides lenders with a detailed view of your financial profile. They will examine your credit history, including your debt-to-income (DTI) ratio, which is calculated by dividing your total monthly debt payments by your monthly pretax income. Lenders typically prefer a DTI ratio of no more than 43%, but some programs may allow a higher ratio with a strong credit score or additional mortgage reserves.

Your credit score plays a pivotal role in determining the terms of your mortgage. A higher credit score can lead to more favourable conditions, including a higher loan amount and a lower interest rate. Conversely, a lower credit score may require additional measures, such as purchasing private mortgage insurance (PMI) or providing a larger down payment.

While a preapproval is not a guarantee of a mortgage, it provides a strong indication of your creditworthiness to sellers. This can be advantageous in competitive markets, as sellers often prefer buyers with preapproval letters. It demonstrates that you are a serious buyer who is likely to secure financing. Therefore, a good credit score, as evidenced by a preapproval letter, can enhance your credibility and increase your chances of securing the home you desire.

It is worth noting that the impact of a credit inquiry on your credit score is usually minor and temporary. Additionally, FICO® mentions that your score will generally remain unaffected if all credit inquiries are made within 30 days. Therefore, while credit score plays a significant role in the preapproval process, the potential impact on your score should not deter you from seeking preapproval when considering a home purchase.

Paying Off My Mortgage: Strategies for Faster Freedom

You may want to see also

![]()

How it helps buyers stand out

A mortgage preapproval is an important step in the home-buying process. It is a more thorough evaluation of your finances than pre-qualification and involves a hard credit check. This process determines how much money you can borrow to buy a home. It is beneficial to get preapproved before you start your house hunt as it gives you a clear idea of how much home you can afford.

A preapproval letter from a lender indicates that they are willing to lend money to you, up to a certain loan amount. This letter is an essential factor in the homebuying process and shows that you are a serious buyer. It is a competitive advantage over other buyers as sellers prefer buyers with a preapproval letter. It shows that you can secure a mortgage and are seriously looking for a home.

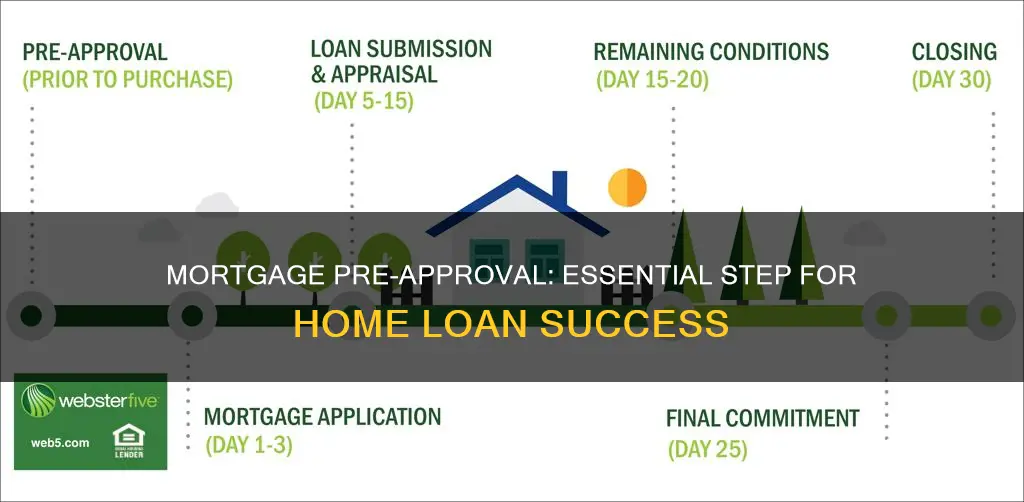

The preapproval process involves a lender looking at your income, assets, debts, and credit record. They will ask for pay stubs, W-2 statements, and signed tax documents from previous years. This process can take a week or longer, depending on the lender. The preapproval letter is typically valid for 30 to 90 days.

While a mortgage preapproval may lower your credit score in the short term, it is a valuable step to take when you are ready to make an offer on a home. It is a great way to spot potential issues and correct them before making an offer. It also gets a large chunk of the mortgage approval process out of the way, so when you find a house you love, you can make a quick offer that the seller is likely to take seriously.

In summary, a mortgage preapproval is essential for buyers as it shows their commitment and financial ability to purchase a home. It helps buyers stand out in a competitive market and increases their chances of securing their dream home.

The High Cost of Mansion Mortgages: Average or Exception?

You may want to see also

![]()

The pre-approval process

To get pre-approved, you will need to complete a mortgage application and provide extensive documentation, including proof of income, employment, assets, and expenses. This can include pay stubs, W-2 statements, tax returns, and bank statements. Lenders will also perform a hard credit check, which can cause a small, temporary drop in your credit score.

Pre-approval letters are typically valid for 30 to 90 days and are not a guarantee of a mortgage. They are based on the assumption that your financial situation will remain stable. Any significant changes to your finances, such as a decrease in credit score, accrued debt, or change in employment, may result in your mortgage being denied after pre-approval.

While pre-approval is not mandatory, it is a valuable step that can give you a competitive edge in the home-buying process. It provides you with a clear understanding of your budget and demonstrates to sellers that you are creditworthy and likely to secure financing.

Beating Foreclosure: My Second Mortgage Nightmare

You may want to see also

![]()

Pre-approval letters

A pre-approval letter is a document from a lender offering conditional approval of a mortgage. It is a statement from a lender that they are tentatively willing to lend money to you, up to a certain loan amount. It is not a guaranteed loan offer, but it lets the seller know that you are likely to be able to get financing. The pre-approval letter may include everything from your maximum loan amount to your estimated interest rate. It will also have an expiration date, typically 30 to 90 days, during which time you can shop for a home and formally apply for a mortgage.

The pre-approval process is a more thorough evaluation of your finances than pre-qualification. Lenders will likely conduct a hard credit inquiry and look at documentation such as proof of employment, income tax returns, and assets. They will also verify your creditworthiness and perform a credit check. They may ask for pay stubs, W-2 statements, and signed tax documents from previous years. This process can take a week or longer, depending on the lender.

A pre-approval letter is important because it shows sellers that you are a serious buyer, and in a competitive market, it can help you stand out among other potential buyers. It is also beneficial to get pre-approved early in the process, as it can be a good way to spot potential issues and correct them in time.

While a pre-approval letter is an important step in the homebuying process, it is not a guarantee that you will get a mortgage. If there are changes to your financial profile after receiving the letter, you may not get a loan. It is also important to note that the pre-approval process may lower your credit score in the short term.

Mortgage Reserves: Critical for Home Loan Approval and Peace

You may want to see also

Frequently asked questions

Pre-qualification is an optional step that can help you fine-tune your budget, while pre-approval is an essential part of your journey to getting mortgage financing. Pre-qualification is a rough estimate of how much you'll be able to borrow, based on self-reported financial data. Pre-approval, on the other hand, is a more thorough evaluation of your finances, including a hard credit check and verification of your income, assets, and employment.

Pre-approval is important because it helps you shop for a home and lets the seller know that you are likely to be able to get financing. It also gets a large chunk of the mortgage approval process out of the way, so when you find a house you love, you can make a quick offer that the seller is likely to take seriously.

To get pre-approved for a mortgage, you'll need to complete a mortgage application and provide documentation, such as proof of income, employment, and assets, as well as undergo a hard credit check. The lender will then review your application and determine if you are eligible for pre-approval.