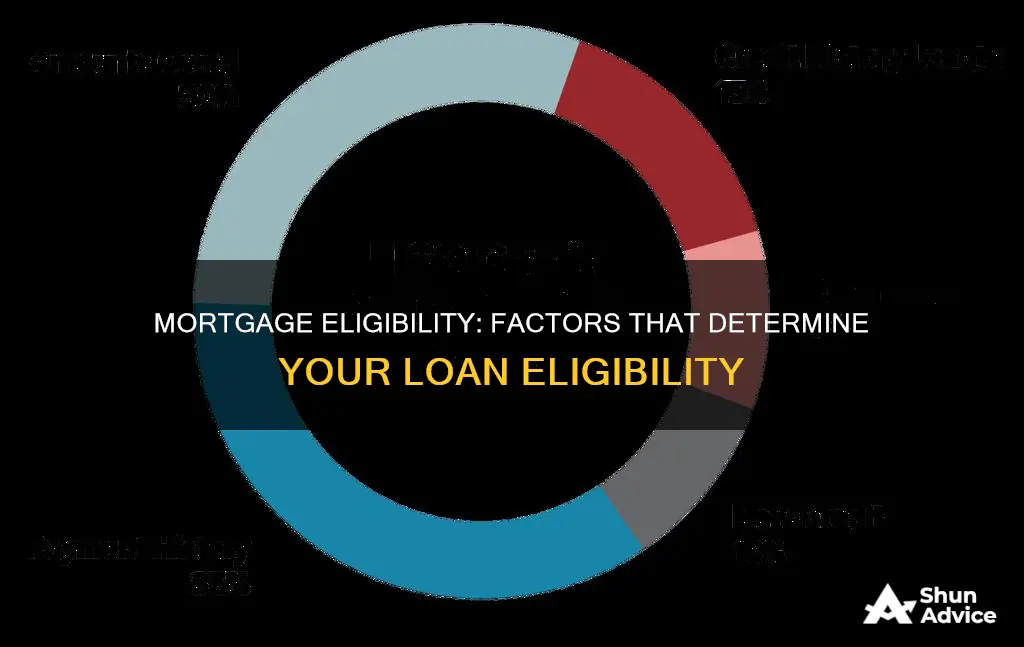

There are a number of factors that determine mortgage eligibility. Lenders will assess your income and employment history to ensure you have a stable source of funds to repay the mortgage. Your credit score is also an important factor, as it indicates your likelihood of repaying the loan. Lenders will also consider your debt-to-income ratio (DTI), which includes monthly expenses such as credit card payments, rent or mortgage, and other personal loans. Additionally, the type of property you want to buy and your age can impact your eligibility. Mortgage eligibility can be confusing, and it's important to remember that it changes from lender to lender.

| Characteristics | Values |

|---|---|

| Credit score | A higher credit score improves eligibility and provides better interest rates. |

| Income | Lenders assess income and employment history to ensure a stable source of funds for repayment. |

| Debt | Monthly debt, including credit card payments, loans, and rent, is considered. A lower debt-to-income (DTI) ratio is more favourable. |

| Employment | A secure job history strengthens eligibility. Self-employed individuals may need to provide additional proof of income. |

| Age | Older applicants may face challenges, as lenders specify the maximum age of the borrower when the loan should finish. |

| Property type | The type of property affects eligibility. Primary residences are typically easier to secure loans for. |

What You'll Learn

![]()

Credit score

FICO scores put a lot of emphasis on payment history and credit utilisation, with other factors also playing a role. Payment history makes up 35% of your FICO score and tracks how well you make your payments. Credit utilisation accounts for 30% of your score and considers your credit card balances, with lower balances preferred by lenders as they indicate a lower risk of default.

Your credit score is also influenced by the length of your credit history and the types of credit you have, such as credit cards, installment loans, mortgages, student loans, and finance company accounts. Recent credit activity, including opening new accounts, can affect your score, as can the amount of available credit you have. While having more available credit may not significantly impact your score, lenders may view it as a sign that you take out any credit available to you, even if you don't need it.

When determining your eligibility for a mortgage, lenders will consider your credit score in conjunction with other factors, such as your income, employment history, debt, assets, and property type. They will assess your income and employment history to ensure you have a stable source of funds to repay the mortgage. Lenders will also consider your debt-to-income (DTI) ratio, which is calculated by dividing your total monthly expenses by your total pre-tax household income. A lower DTI ratio indicates that you are a more attractive borrower.

Additionally, your credit score can impact the interest rate and loan eligibility. A higher credit score can lead to a better interest rate, resulting in lower monthly mortgage payments. It is recommended to check your credit score and review your credit report before applying for a mortgage to ensure everything is correct and identify areas for improvement.

Islamic Mortgages: Unique Features and Differences Explained

You may want to see also

![]()

Income and employment history

Lenders will assess your income and employment history to ensure you have a stable source of funds to repay the mortgage. A consistent income and a secure job history can strengthen your eligibility. It will also help determine how much a lender is willing to lend to you, which is a big part of your mortgage affordability. Typically, you can borrow between 4 to 4.5 times your household income for a mortgage. Some people, such as nurses, doctors, teachers, or higher earners, can qualify for 5.5 or even 6.5 times their income.

Lenders will require documentation to verify your income and employment stability, such as a job offer letter, employment contract, or pay stubs. They will also want to see that you have a history of receiving variable income and that your overall income is enough to make the payments on the loan. If you are self-employed, it is important to show that you have a steady income, and lenders will likely ask for 2-3 years' worth of accounts or your most recent profit figure. Lenders will also want to see that your income is projected to continue for at least the next two years.

If you have been with the same job for less than two years, lenders will collect information on previous employers and your line of work to address income trends. They will require documentation and/or a written explanation in cases where you have a new job but a previous two-year employment history. For example, if you were in school previously or took time off to be a homemaker. A two-year employment history is standard, but shorter employment histories may be permitted for applicants with stable jobs and incomes or other positive factors.

Lenders are less concerned with where you work or your job title and more focused on the stability of your income and your prospects for continued employment. Military service and formal education, such as college or vocational school, are usually considered employment when you apply for a mortgage. Similarly, borrowers who have changed employers but continue to advance in their career field and earn a steady or improving income are better positioned to qualify for a mortgage.

Understanding Mortgage Payment Strategies and Management

You may want to see also

![]()

Debt-to-income ratio

Your debt-to-income ratio (DTI) is a key factor in mortgage approval. Lenders use your DTI ratio to determine if you can comfortably afford to make monthly mortgage payments. It is calculated by dividing your total monthly debt payments by your total pre-tax monthly income. The formula involves dividing your total recurring monthly debt by your gross monthly income (income before taxes or other deductions).

Monthly debt payments can include monthly credit card payments, car payments, student loans, alimony and child support payments, any house payments (rent or mortgage) other than the new mortgage you’re seeking, rental property maintenance, and other personal loans with periodic payments. Do not include everyday expenses like groceries or utilities, entertainment expenses and health insurance premiums.

Lenders may also use your new mortgage payment in these calculations to make sure you meet their approval guidelines. Ideally, your front-end HTI calculation should not exceed 28% when applying for a new loan, such as a mortgage. You should strive to keep your back-end DTI ratio at or below 36%. Staying within these ranges demonstrates to the lender that you are well equipped to meet your ongoing financial obligations while still leaving room in your budget for living expenses and unexpected events.

While standards vary, most lenders prefer a DTI ratio below 35%-36%. Some mortgage lenders may allow up to 43%-45%, with loans insured by the Federal Housing Administration (FHA) allowing up to 50%. As a general rule, you'll need a DTI ratio of 50% or less to qualify for most loans. The lower your DTI ratio, the more attractive you are as a borrower. A low DTI ratio reflects a good balance between income and debt, making you a more attractive candidate for loans.

Factors That Influence Mortgage Rates and Payments

You may want to see also

![]()

Age of the applicant

While age is not the sole factor in determining mortgage eligibility, older applicants may find it harder to secure a mortgage loan. This is because mortgage lenders will usually specify the maximum age of the borrower at the end of the mortgage loan term, which is typically 70 years old.

Lenders view older people as high-risk borrowers, especially if they are retired or approaching retirement. This is because they are likely to have a lower income, which could affect their ability to keep up with mortgage repayments. Older applicants will need to prove that their pension will cover the mortgage repayments and other outgoings.

In the US, the Equal Opportunity Credit Act and the Equal Credit Opportunity Act make it illegal for lenders to refuse to loan money to applicants because of their age, as long as they are 18 or older. However, applicants still need to prove that they can afford the monthly mortgage payments and that they are not a high risk to fall into foreclosure.

Lenders will also consider an applicant's income and employment history to ensure they have a stable source of funds to repay the mortgage. A consistent income and secure job history can strengthen eligibility. Lenders will also look at an applicant's credit score when determining whether they are a high risk. A high credit score, coupled with a history of paying bills on time and a low level of credit card debt, will make a lender more willing to grant a mortgage, regardless of age.

To increase the chances of getting approved for a mortgage loan, applicants can ensure their total monthly debts, including the new estimated mortgage payment, equal no more than 36% of their gross monthly income. They should also ensure their total monthly housing payment, including taxes, insurance, and interest, consumes no more than 28% of their gross monthly income.

Understanding Mortgage Interest Calculation: What You Need to Know

You may want to see also

![]()

Property type

Firstly, the property's usage, whether residential, commercial, or investment, is a key consideration. Investment properties, for example, often have stricter deposit requirements and generally require larger deposits than primary residences.

Secondly, the property's condition and construction type are important. Most lenders consider traditional houses made from bricks and mortar, but anything outside of this is usually classed as a "non-standard" property, which may include higher-risk materials or construction types. For instance, high-rise condominiums or manufactured homes may incur additional risk-based surcharges from lenders.

Thirdly, the specific type of residence, such as a detached house, semi-detached house, terraced house, flat, or studio, can impact eligibility. For example, most flats are bought on a leasehold basis and are generally eligible for mortgages, but lenders' criteria may vary depending on the flat's size and features. Studios, in particular, may be subject to minimum size requirements by lenders, often needing to be at least 27 sqm to be eligible for a mortgage.

Lastly, the property's location and features can influence eligibility. The age of the property, its maintenance and renovation history, and the presence of special features like a pool can all impact its eligibility. The location's proximity to emergency services and the neighbourhood's crime rate can also affect the property's value and, consequently, the eligibility for a mortgage. Additionally, the actions of neighbours in shared or adjacent properties can impact the property's value.

It is important to note that mortgage eligibility is a complex interplay of various factors, and lenders have different requirements. Thus, consulting an independent mortgage broker or using a mortgage calculator can help determine eligibility for specific property types.

Debt Collection and Mortgage: What's the Connection?

You may want to see also

Frequently asked questions

Lenders consider two main factors when reviewing mortgage applications: the likelihood of repaying the loan (usually determined by a credit score) and the ability to do so (usually determined by proof of income). Other factors that influence mortgage eligibility include age, employment history, debt, assets, and property type.

Lenders assess your income and employment history to ensure you have a stable source of funds to repay the mortgage. A consistent income and a secure job history can strengthen your eligibility. Lenders will also consider other reliable and regular income sources, such as investment accounts, contract work, or government benefits.

Lenders will consider your debt-to-income (DTI) ratio, which is calculated by dividing your total monthly expenses by your total pre-tax household income. A lower DTI ratio makes you more attractive as a borrower. As a general rule, a DTI ratio of 50% or less is needed to qualify for most loans, with lenders typically preferring a ratio lower than 36%.